Angus Nicholson for Chris Weston, Chief Market Strategist at IG Markets

Asian markets moved cautiously higher today in the wake of solid US data on Friday and the oil price selloff after Saudi Arabia refused to commit to supply cuts or freezes without Iran. That equity markets are so far ignoring the pullback in oil prices should be seen as a positive, given they have been so tightly correlated over the past few months. Oil looks likely to head below US$35, but there does not look to be enough negativity in the market to push it below US$30. This pullback is very important because if we see oil prices bounce upwards again after returning to the US$30-35 region then that largely locks in the mid-February double bottom around US$26 as the cyclical low for the oil price. Meaning the only way from there is up. But price moves are set to be fairly volatile as rumours and press releases leak out as we head into the producers meeting in mid-April. But when oil prices turn up again the high-yield debt complex and emerging markets are all likely to rally strongly.

US

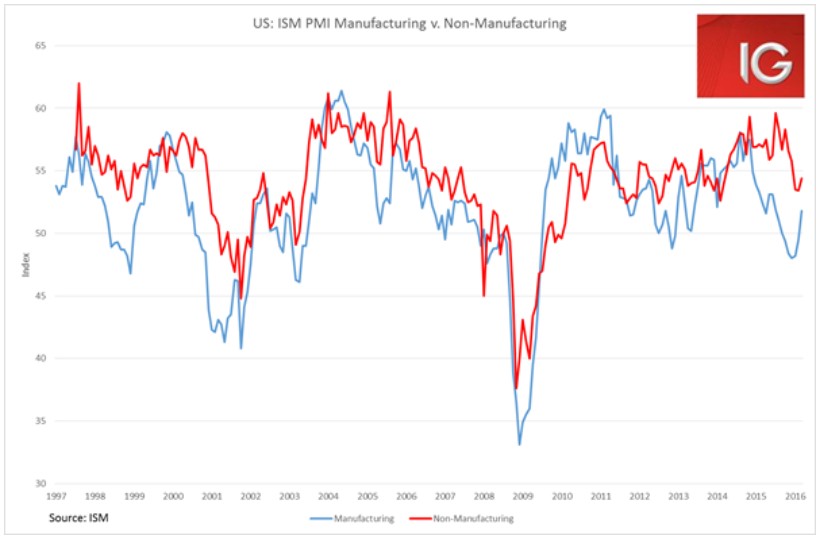

US data on Friday was solid across the board, except for a miss on auto sales. The weakness in the US dollar is clearly flowing through to the US economy. Non-Farm Payrolls added another above 200,000 number and hourly earnings returned to positive month-on-month growth. But it was really the ISM Manufacturing that stole the night. The regional activity indicators were pointing to a strong number, but 51.8 from a prior 49.5 really puts to bed concerns about an imminent manufacturing recession in the US. The ISM Non-Manufacturing also bounced back to 54.4. As I’ve argued before, the weak US data seems to have largely been a reflection of the US dollar strength, and with a weaker US dollar, recession concerns look to be ebbing away dramatically. When one looks at the manufacturing and non-manufacturing indices on a chart, it is striking the similarities between the past year and 1998 when the US dollar surged on the back of safe-haven buying in the wake of the Asian Financial Crisis.

The weaker US dollar is also helping the Chinese economy (alongside significant Chinese government stimulus) by removing the pressure for them to devalue the CNY. Near-term strength in the US and China is a positive for the world (despite coming at the cost of Japan and the Eurozone), and given this alone, one can see a good case for the Fed to leave rates on hold throughout 2Q. The WIRP bond market pricing currently has November as the earliest date with an above 50% chance of a rate hike. I think there is a solid case for a September hike, but we are likely to continue to see USD weakness throughout 2Q.

Australia

The Aussie dollar continues at what are likely unsustainable levels, although much of this is driven by US dollar weakness. The RBA will leave rates on hold tomorrow, but today’s series of Aussie data releases certainly highlight the risks of a rate cut in 2H (I’m looking at 4Q in particular given the election/Glenn Stevens retirement dynamic).

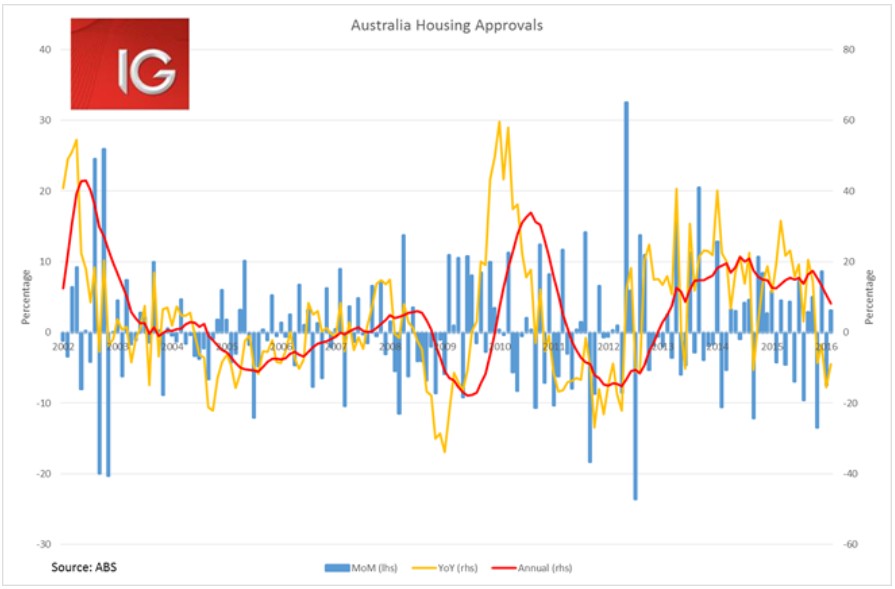

The general trend in retail sales and housing approvals releases today is fairly concerning for GDP growth in 2H. Housing approval growth has declined for the fourth straight month in a row in YoY terms. Given home building was such a big contributor to 4Q GDP, the continued slide in approvals is likely to see home construction weigh on 1Q GDP. This data does certainly argue somewhat for the bear case on the Aussie banks that a minor increase in housing delinquencies could see them reduce dividend payments. Nonetheless, how this trend plays out over the coming months will be key in deciding the fate of the Big Four banks.

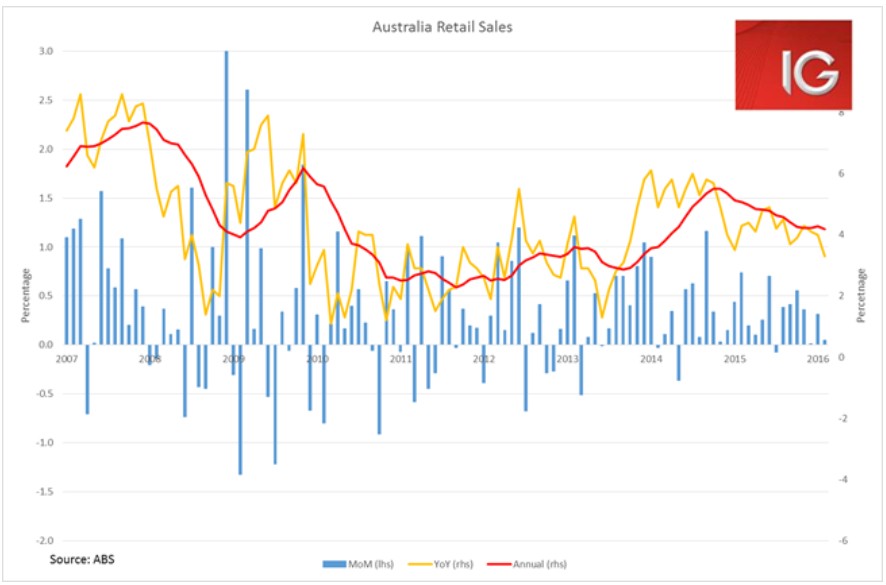

Retail sales were flat month-on-month and showed the weakest YoY growth since September 2013. If the current trend continues, Aussie retail sales could be returning to their 2010-2013 era of 2-3% YoY growth. One would expect that 2Q may see a bit of a bounce in retail sales as Aussie consumers make the most of the likely temporary strength in the AUD, but this AUD bounce is likely to dissipate by 2H.

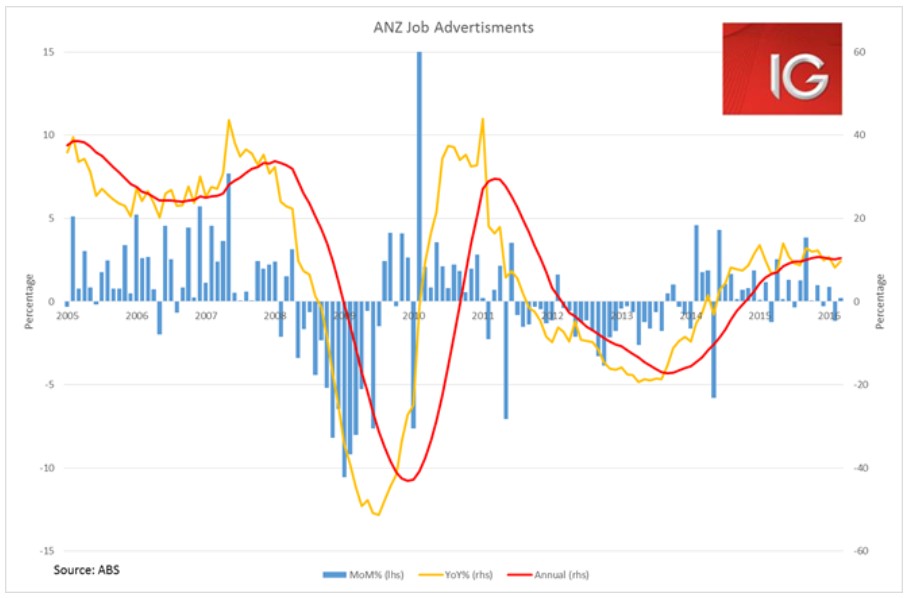

ANZ job ads increasingly look like they peaked in mid-2015, but continue to hold up for the moment. However, a rate cut by the RBA in the second half of the year after these trends play themselves out and after Glenn Stevens vacates his position seems increasingly likely.