Angus Nicholson for Chris Weston, Chief Market Strategist at IG Markets

Fed Chair Janet Yellen’s comments overnight confirmed the significantly dovish turn seen in the last Fed statement. And while there are positive developments in the US economy, the Atlanta Fed’s GDPNow estimate for 1Q has collapsed to 0.6% from 1.4% last week. Given this, Yellen’s dovishness seems warranted. Nonetheless, it’s clear from her and a number of Fed speakers that they also have a heightened awareness of the global implications of tighter US monetary policy. This is something that Indian central bank governor Raghuram Rajan has been calling for repeatedly.

Yellen’s speech helped see the DXY dollar index drop 0.8%, and September is now the only date the markets are pricing with a better than 50% probability of a rate hike. Materials, and particularly gold miners, are rallying heavily off this development. But it also has broader implications.

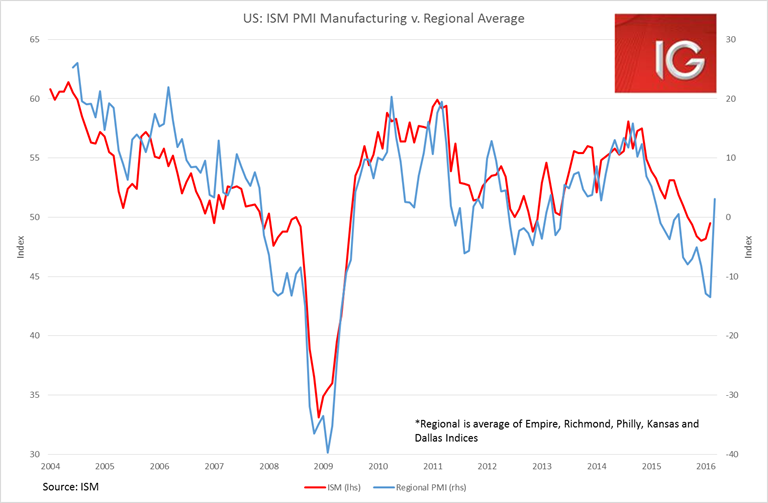

A weaker US dollar has really been driving the recovery in US manufacturing. All major US regional manufacturing indicators are pointing to a major recovery in Friday’s ISM manufacturing number. It is likely to move above 50 for the first time since September last year. This in turn is likely to see further benefits in US job growth going forward.

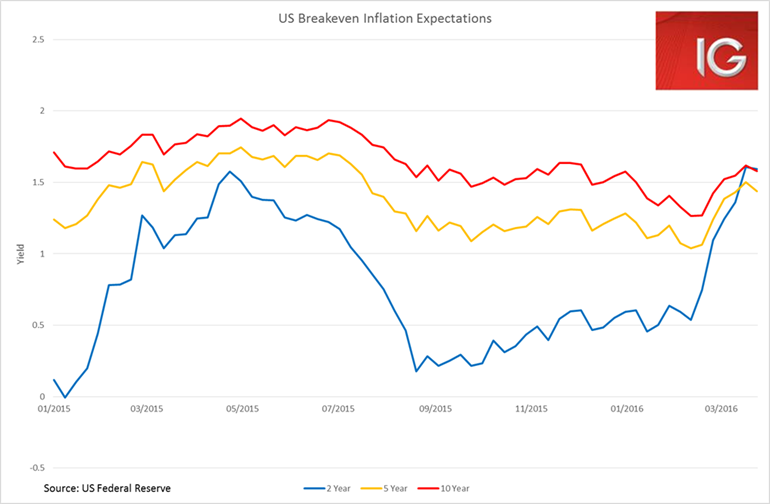

Stronger US job growth as the manufacturing sector recovers could see a significant tightening in the US job markets. In economic theory, the Phillips Curve is meant to measure the amount of spare labour capacity and its respective effects on inflation. And if we do see a noticeable pickup in employment this pressure may (finally) start showing up in the inflation numbers. Even though Monday’s PCE Core inflation release underwhelmed, markets are becoming increasingly aware of the potential for a rise in inflation. This is very clear when one looks at the momentum in breakeven inflation expectations.

The weaker US dollar has coincided with what looks increasingly like the cyclical bounce in a range of commodity prices. And the prospect of resurgent US manufacturing job growth and commodity prices raises the prospect of rising inflation in 2H 2016. Chart (Source: Bloomberg Finance L.P.) white: WTI Oil, green: Copper, purple: Iron ore.

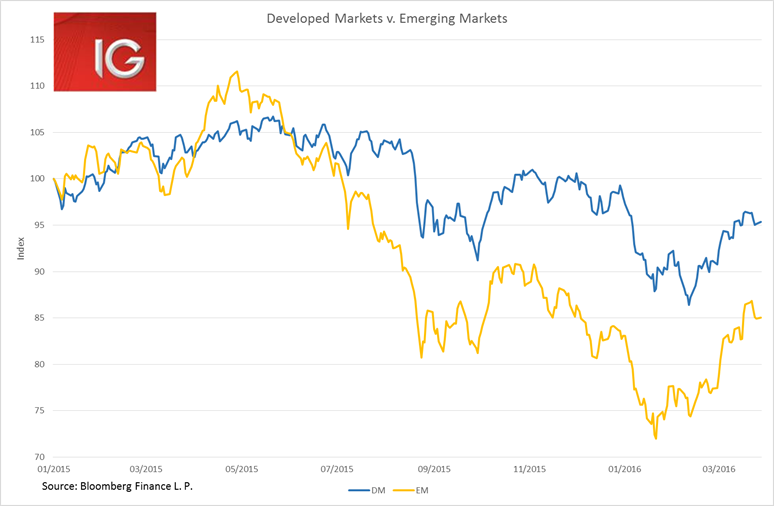

A weaker US dollar not only benefits the dollar-denominated price of many commodities, which are a key export for most emerging markets. But it also lowers the burden of US dollar-denominated debt in a range of emerging markets. Emerging market equities look set to significantly outpace developed markets in 2016 (EEM and EMCI are likely your best ETF picks to benefit from the emerging markets rally).

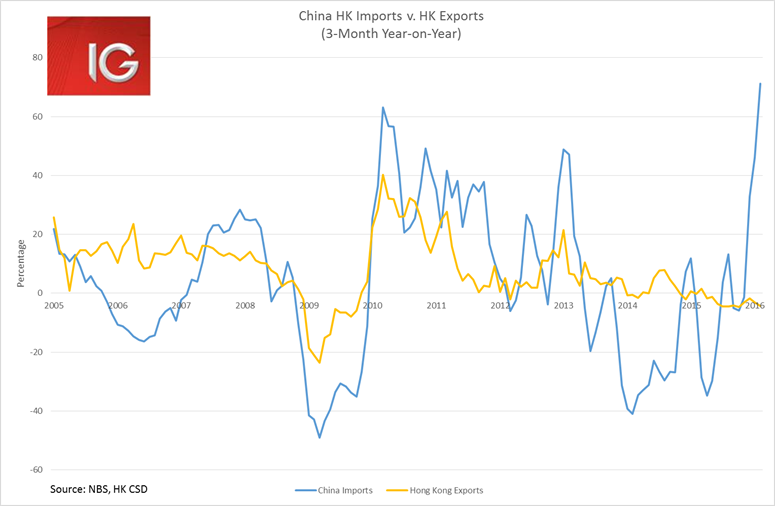

Weakness in the US dollar, and subsequent strength in the JPY and EUR, puts a lot less pressure on China to devalue their currency. This easing of CNY pressure has also been well-timed with a pickup in property and fixed-asset investment as China turns on its fiscal taps again. Nonetheless, the threat of a potential devaluation will continue to linger. Yesterday’s release of Hong Kong’s trade statistics for February confirm the dramatic difference in China’s reported imports from Hong Kong versus Hong Kong’s reported exports to China. Clearly, the balance of payments net errors and omissions capital flows are still making their way out through the trade account.

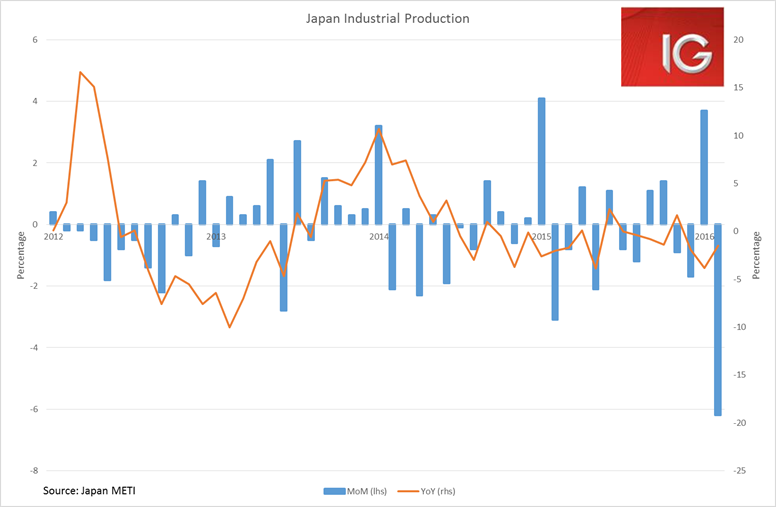

But this newfound weakness in the USD comes at the cost of JPY and EUR strength. And given these economies are still struggling it is uncertain how much longer they will be able to cope without the benefits of a weaker currency. And as if to underline this point today, Japanese industrial production in February promptly collapsed by 6.2% in month-on-month terms.

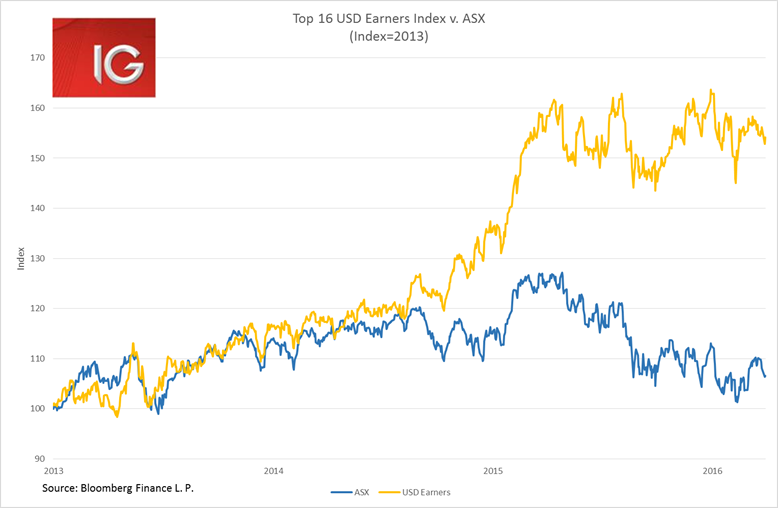

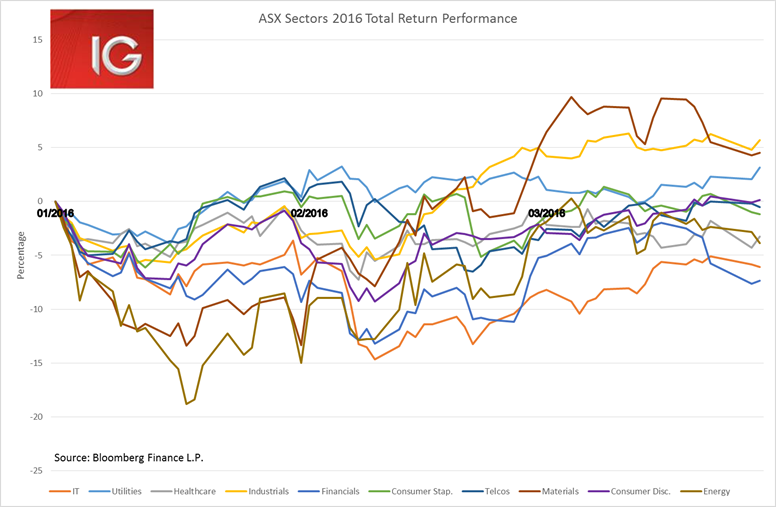

These macro factors are having a clear influence on the trajectory of the ASX. I’ve created a chart here that show the total returns of the ASX by sector because dividend yield is such an important driver for the ASX. In total return terms, the materials sector (particularly BHP and RIO) makes a compelling buy case with resurgent commodity prices and still hefty (if slightly lessened) dividend payouts (materials year-to-date total return +4.5%). One of the surprising losers from such a scenario is healthcare (YTD TR -3.3%), because of the government’s focus on medical expenses and the lack of benefit from foreign currency earnings with the stronger Aussie dollar.

And the greater impact of this story is the definitive end of the outperformance of USD earning stocks. With the RBA likely on hold all year, and negative rates in Europe and Japan, the Aussie dollar increasingly looks likely to continue above the US$0.70 level for the rest of the year. A stronger AUD will make it a tough year for healthcare stocks.