Angus Nicholson for Chris Weston, Chief Market Strategist at IG Markets

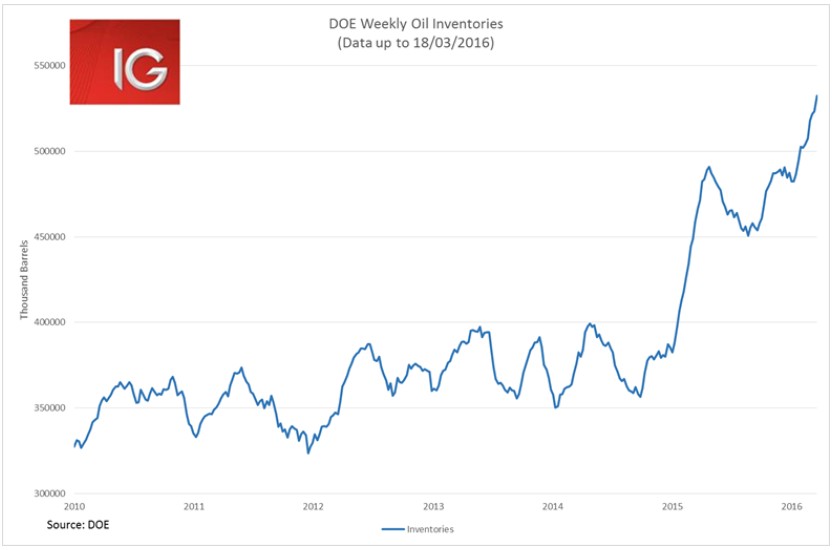

The oil price and equity markets are teetering on the verge of a much larger pullback as hawkish Fed officials have lifted the US dollar this week. Markets in Asia look to be rolling over as the whole region suffered steady losses throughout the session. Chinese Premier Li Keqiang’s upbeat speech at the Bo’ao Forum did little to soothe investor concerns as the Shanghai Composite had its worst day in two weeks. Overnight, the US weekly Department of Energy numbers saw a significant addition to already heavily oversupplied oil inventories. 9.4 million barrels were added to crude inventories, the biggest weekly addition since February, making another concerning data point for oil after last week’s Baker Hughes crude oil drill rig count increased for the first time in three months.

The oil price did look like it was getting ahead of itself above the US$40 level. While US oil production has begun to slow, there was a large amount of oil imports that added to the DOE inventory numbers showing that global production is still way above rebalancing levels. The technicals and the fundamentals are lining up for a pullback in the spot price to at least US$35, if all the way back down to US$30 again. There is the possibility that the price surges higher on some deal from the oil producers meeting in Doha in mid-April. Although the prospects for a steadily higher US dollar and ongoing inventory builds provides greater downside risks to the current price level.

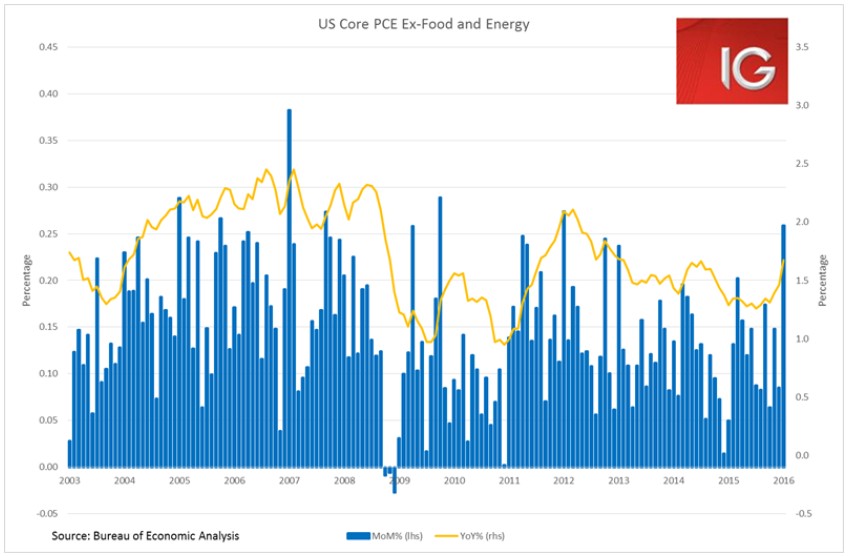

Commodities as a whole are not coping well with the bounce in the US dollar this week. The iron ore price lost 0.8% overnight, and the Comex Copper price fell 2.4%. And Dalian iron ore futures have fallen a further 4.5% in trade today. If much of the selloff is being driven by the four-day rally in the US dollar, then commodities are in for an unpleasant time next week. The final figures for US 4Q GDP are released on Friday (while most markets are closed) and then next week will see Core PCE and Non-Farm Payrolls data released.

Core PCE inflation, in my view, is almost the key data series for global macro at the moment. If strong and consistent growth is borne out in the Core PCE release next week, two rate hikes by the Fed this year will be the bare minimum. Continued strong figures over the coming months potentially opens up an even more hawkish path for the Fed Funds rate than the “dot plots” indicated at the last meeting. And Bullard’s comments overnight were thoroughly consistent with such a view, as he stated he has been tempted to “unilaterally” pull out of the dot plots because he thinks they mislead the market.

ASX

The ASX has noticeably reversed its trading pattern of the past few weeks, not only because it is selling off, but also which stocks are being sold off. Short-covering in the banks, materials and energy stocks coincided with US dollar weakness and rising commodity prices and helped drive the rally of the past couple of weeks. In such a scenario, growth stocks, in particular healthcare stocks, notably missed out on the rally in part due to US dollar weakness hurting their previously beneficial offshore earnings.

Today healthcare stocks are up over 1% as the ASX as a whole loses more than 1%. Concerns about an ongoing slide in equities is also evident in the strong buying being seen in utilities stocks as well.

But the banks have been the biggest drag on the index today after ANZ announced a $100 million increase in bad debts related to the commodities sector. ANZ lost almost a full 6% on the day, with WBC close behind losing 4.5%. The renewed slide in commodities and the belief that the rally in bank stocks has been overdone all contributed to today’s sharp reversal in the sector.