Chris Weston, Chief Market Strategist at IG Markets

To any conspiracy theorists it’s all become quite clear. There is a global coordinated central bank effort to weaken the USD in play, which in turn has led to a massive de-risking in equity and credit markets. A weaker USD has been a key reason why we have seen a 54% rally in US crude and 40% rally in Brent. And, perhaps, these moves will see some upside in headline inflation globally. The fact that we have seen one of the biggest two-day sell-offs in the USD in the last seven years is the focal point for markets, and, importantly, this has allowed the PBoC to ‘fix’ the CNY by a monster 333 pips stronger today, which, in percentage terms (-0.5%), is actually the third strongest fixing ever! Some have posited that USD weakness was meant to help reflate other economies, but perhaps the real issue was to avoid a sizeable CNY devaluation. Given the PBoC have strengthened the currency by 544 pips over the last two days suggests this could be the case.

Perhaps, we should have listened to the barrage of comments from PBoC Governor Zhou Xiaochuan, who noted recently that there was ‘no basis for CNY deprecation’. He doesn’t talk much, so, perhaps, when he does we should pay greater attention!

Since the G20 meeting in Shanghai there have been many red flags. Whether it’s the PBoC easing the Reserve Ratio Requirements (RRR) by 50 basis points, the RBNZ cutting its cash rate by 25 basis points (very much out of consensus), or the ECB moving to a focus on credit markets and going significantly above and beyond expectations. Of course, then we also have the Fed, who missed the economists’ modestly hawkish playbook by about as wide a margin as we will likely see. What the Fed has done is bring back the element of surprise to its meeting, similar in a way to the ECB.

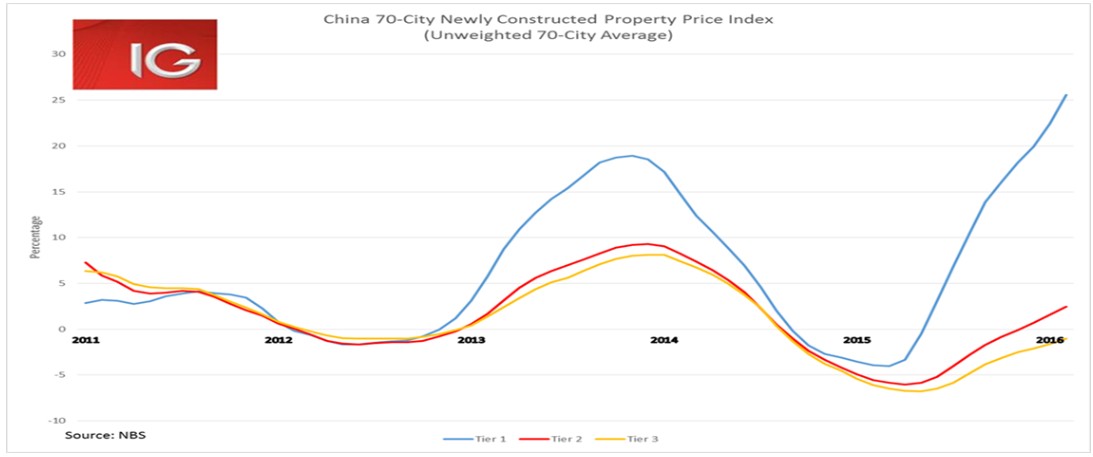

We can look at measures from the Chinese to spur on the property market, which has led to property sales (February) gaining 43.6% and new loans for house purchases rising to the highest ever (RMB471 billion). Authorities have opened up channels to allow Chinese investors to do what they do best – buy property. Eastern Jiangsu Province has even had to conduct a lottery just to give individuals the right to buy a property. In turn, we have seen the level of outstanding margin debt falling to the lowest levels since November 2014, down 63% from last June. Out of stocks, and into property.

Then we can focus on house price data out today – China Tier 1 cities: Shenzhen +56.9% YoY, Shanghai 20.6% YoY, Beijing 12.9% YoY, Guangzhou +11.8% YoY

If an agreement was forged, then it is a bitter pill for the likes of Glenn Stevens, Mario Draghi and Haruhiko Kuroda to swallow. If true, then it shows just how concerned these central bankers are about a sizeable CNY devaluation.

Interestingly, the positive correlation between the ASX 200 and AUD/USD is actually the fifth highest in five years, so unlike in European or Japanese equities, traders are not concerned about exchange rate moves. Traders are happy to buy as there is a positive impact from rising terms of trade and low volatility herds individuals into yield plays, something Australia is well known to offer. AUD/USD still feels like it can go higher here and I have absolutely no conviction to short even at these levels. The path of least resistance (in this current backdrop) is for a higher AUD and I look for $0.7800 to $0.7900 as possible place to short with greater conviction.

Saying that, the trend has been to fade risk into the afternoon session. The Nikkei has been pulling down sentiment and with the USD/JPY hitting a low of ¥110.81 before further rumours that the BoJ were checking rates caused a spike higher. A weaker open in Europe can be expected and the prospect of traders booking a few short-term profits after some stellar gains in the month of March. Comments today from key Fed members Bullard and Dudley could be worth listening too, especially as Bill Dudley seems to be the key architect behind recent Fed dovish stance.