Angus Nicholson for Chris Weston, Chief Market Strategist at IG Markets

The risk-on rally has continued in Asia (ex-Japan) after processing the announcements from China’s National Party Congress and the release of US Non-Farm Payrolls (NFP) over the weekend. The face value market interpretation seems to be that strong headline growth in the NFP but weak hourly earnings growth keeps Fed rate hikes on hold, while China’s batch of 2016 targets are not only feasible but will entail greater fiscal spending and help the current pickup in commodity prices.

I would question both those interpretations of the weekend’s developments, and perhaps the realisation of their flaws will be major factors in the pullback of the current rally. That is not to say the pullback will inevitably take global markets lower than where we bottomed in February, but a pullback is certainly coming. In particular, rallies in the materials space and in industrial metals’ spot prices look like they are getting way ahead of where the supply/demand rebalancing is. Iron ore prices, for one, look like they are fundamentally misinterpreting a rebuild in Chinese inventories as a genuine pickup in demand.

US

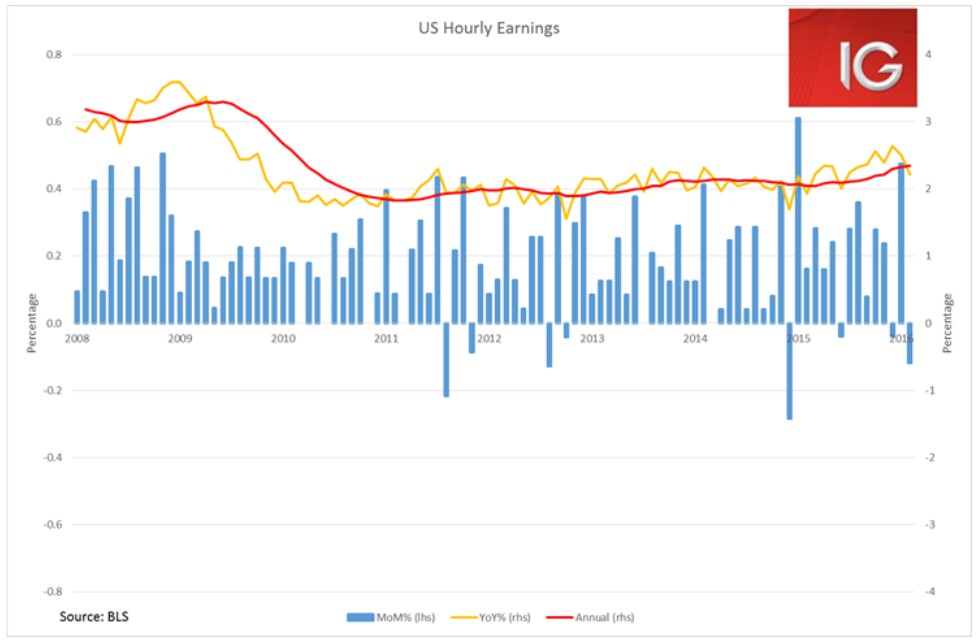

The dollar index lost 0.3% on Friday, despite the NFP adding 242,000 new jobs. This headline figure was tempered by the biggest MoM decline in hourly wages since December 2014, and this seemed to be the key focus for the market. Given the clear pick up in US data across a range of indicators, and most importantly a nascent recovery in manufacturing PMIs, it seems disingenuous the discredit the impressive headline NFP number. The hourly wages index does have quite a bit of variance month-to-month, and if one looks at annual growth (a much longer term trend) it is clear that hourly earnings have been steadily growing since February 2015. The current annual growth rate is 2.3% – the strongest growth since April 2010 – belying the MoM dip. Once the USD becomes more responsive to the improving US economic indicators, there is a real risk that it begins to tighten financial conditions again and put increasing pressure on the equities rally, not to mention weakening commodities prices.

China

China’s annual National Party Congress work report, released on Saturday, seems to have been interpreted as cautiously positive for markets today. But a careful read through of the targets for 2016 shows deep divisions within the leadership over the direction of reform and economic policy. It is a document ridden with internal contradictions, and some of the targets being proposed display an almost a wilful ignorance of the country’s current predicament.

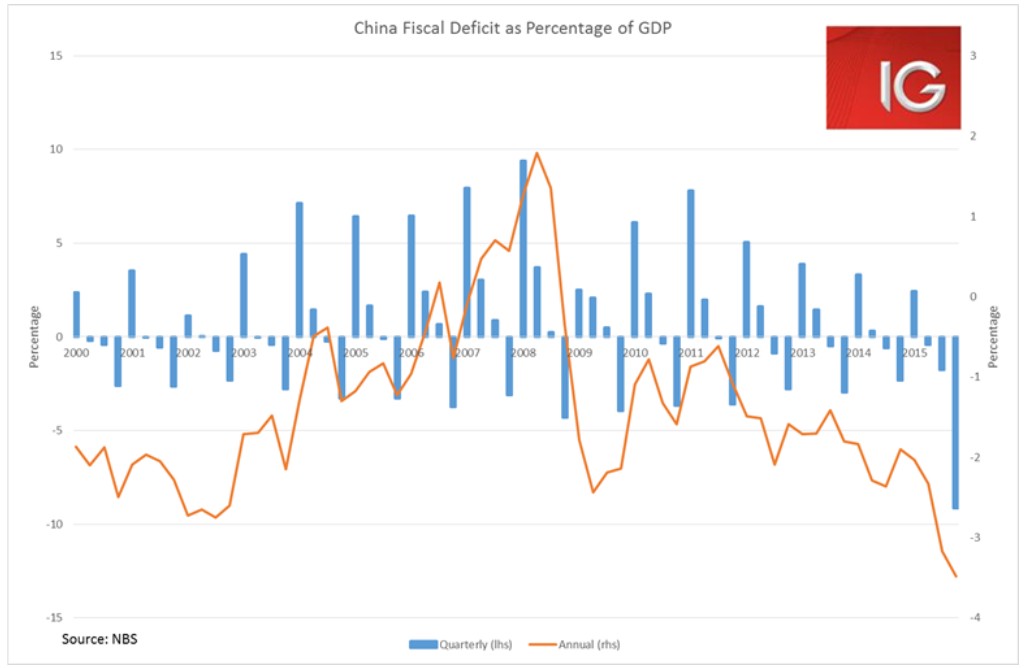

The 2016 GDP growth target of 6.5-7% alongside the fiscal deficit target of 3% of GDP is probably the most glaring internal contradiction. And it is clear they came from opposing factions, the GDP target from the “growth at any cost camp” (SOEs, provincial governments, those concerned about a financial crisis if growth slips too rapidly) and the fiscal deficit target from the “growth within China’s means” camp (those more concerned about the sustainability of China’s accelerating debt pile). It is simply not possible to achieve both of those targets in 2016. Especially when government figures show China’s fiscal deficit in 2015 was 3.5%, already higher than the 2016 target. Elements of the central financial leadership appear to be trying to restrict growth through the fiscal deficit target and the announcement that the local government bond swap quota for 2016 will be set at RMB 3.2 trillion lower than the RMB 3.8 trillion issued in 2015.

If that growth target is to be met, the fiscal deficit is going to blow over 4% and the bond swap quota will have to be raised to over RMB 4 trillion. These adjustments will probably be necessary just to keep China’s engines running in any case.

Australia

Aussie materials stocks and the Aussie dollar both look like they are getting ahead of themselves. Iron ore skyrocketed 5% on Friday, and the highly leveraged Fortescue Metals jumped 26.1% today! And yet much of the recent levity seen in the iron ore spot price seems to be driven by the rebuild in Chinese iron ore inventories. Chinese iron ore port inventories also look like they are peaking around the 95-96 million tonne level on the charts, and current inventory build looks increasingly like it is running out of steam.

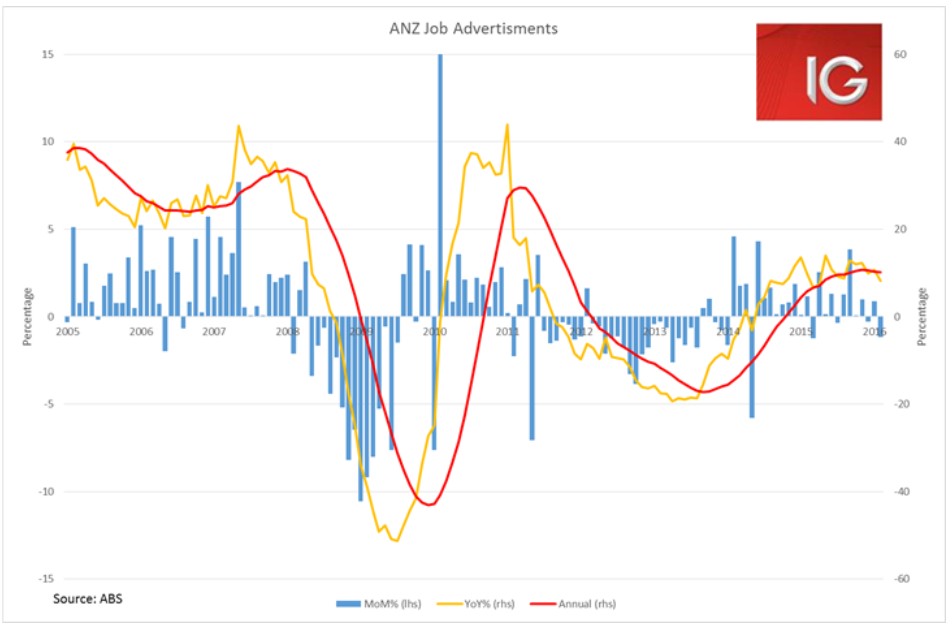

Australia’s huge 4Q GDP growth has seemed at odds with some of the other data evident in the Australian economy. Whether growth holds up in 2016 is a fierce debate in the analyst community, we still believe a faltering in the growth rate in 2016 the most likely scenario, but the Aussie dollar does not appear convinced at the moment. But the ANZ job ads today saw their weakest monthly performance in a year, and are also looking like they are past their peak. It’s early days yet, but the Aussie dollar above US$0.7400 seems likely to be an ephemeral achievement.