Chris Weston, Chief Market Strategist at IG Markets

There is an air of fatigue from the bulls in a number of developed equity markets, but they continue to grind higher.

We have not yet reached the point where the market internals are highly suggestive of contrarian short positions. But the market is in need of some injection of new news to provide an injection of inspiration and cause a new leg higher. It seems unlikely this inspiration comes from today’s US payrolls. After yesterday’s employment sub-component of the ISM services PMI (the lowest levels since 2014), one suspects the market goes into this release fearing a number closer to 150,000.

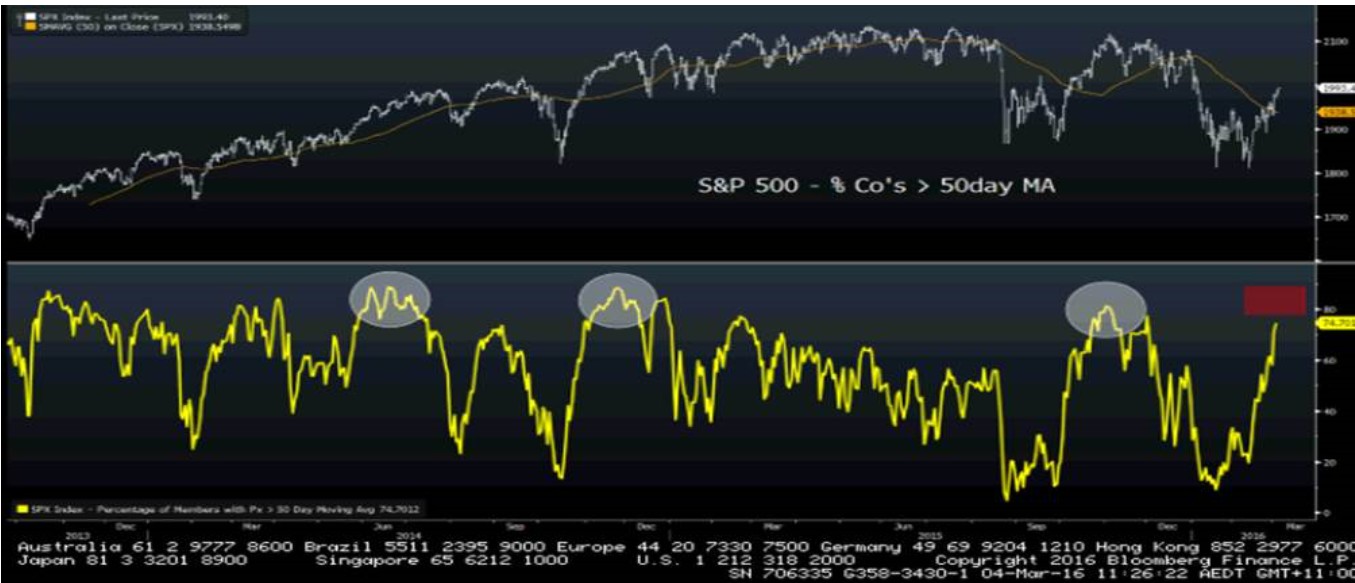

The purest reaction to the payrolls will be seen in 2- and 5-year US treasuries and fed fund futures and from there we should get a read into credit, the USD and then subsequently equities and commodities. Focusing on the S&P 500 (see chart below), the index looks set to close the week above the neckline of the January and February double bottom at 1947 and the technical target here would be 2080. Naturally 2080 is not going to be seen overnight, although it is only a further 4.3% away.

Looking at the market internals, the index is not yet at a stage where I would have any strong conviction in taking a contrarian view, despite a sizeable 93% of companies trading above the 20-day moving average. Taking a slightly longer-term stance, 74% of companies are trading above the 50-day moving average and it has been a more reliable indicator to fade the index when 85% to 90% of companies are above this average. A modest 5% of companies are trading two-standard deviations from the 20-day average and again my preference is to wait for this level closer to be closer to 20% before feeling things have become stretched.

The point is: the trend is higher and the technicals alone suggest a move into 2080, but the internals are starting to suggest lightening up on longs, although we are not yet at the point of conviction. There are conflicting forces at work.

(percentage of S&P companies trading above their 50-day MA)

(Source: Bloomberg)

As goes oil, so goes the S&P 500 and from here we get the leads for the ASX 200 and Asia. Price action on both the daily and weekly charts is becoming more compelling and the bulls will be gunning for a weekly close above $36.28 (April contract) – the 28 January high and double bottom neckline. If we see a break here, then traders could be targeting a move into $45.00, although the longer-term downtrend comes in around $40, and a break at this level will be tough going. A break of $36.28 has to be on the radar though, but until this break, price could go anywhere. Nonetheless, oil is certainly looking more constructive and that is underpinning the moves in other assets.

Locally, there has been a tendency to fade the AUD and this seems fair given the run we have seen. We have China’s National People’s Congress over the weekend, although the gapping risk on Monday is relatively low. A below consensus 30 basis point increase in January retail sales has taken some wind out of the ‘Aussies’ sails and, judging by the weekly chart, the failure comes at a key level. There is a confluence of resistance seen between $0.7380 and $0.7385 and we have seen a bias to sell into this level. Like oil, an upside break here would be very positive.

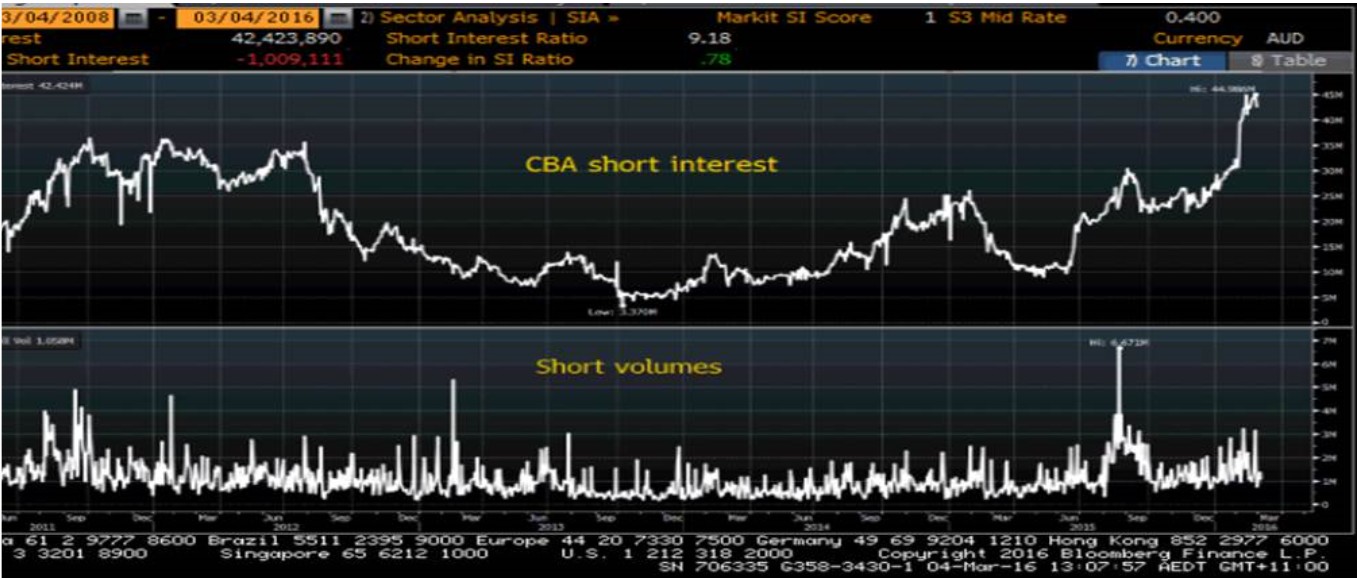

The ASX 200 is closing out the week holding the recent gains and looking at a very impressive 4.5% rally on the week. In USD terms the index has put on 7.7%, which is one of the strongest equity markets this week globally. This is what will happen when volatility subsides and investors throw a bid in for yield, where of course the ASX is the global benchmark. We can also look at the fact that at the start of the week CBA had a massive $44 million in short interest and $72 million in ANZ. Clearly parts of this short interest has been covered. On the week, the materials space has rallied just shy of 8%, energy 7.8% and financials 6.5%.

(Short interest in CBA)

(Source: Bloomberg)

(Short interest in ANZ)

(Source: Bloomberg)

The subdued leads today in Asia haven’t done a huge amount to benefit our European opening calls, but as things stand we expect markets to open on the front foot. EUR/USD looks interesting, especially with the ECB in focus next week. My preference is to look for shorts into $1.1030, with a stop at $1.1100.

Ahead of the open we are calling FTSE 6165 +31, DAX 9795 +44 and CAC 4437