Angus Nicholson for Chris Weston, Chief Market Strategist at IG Markets

RRR cuts

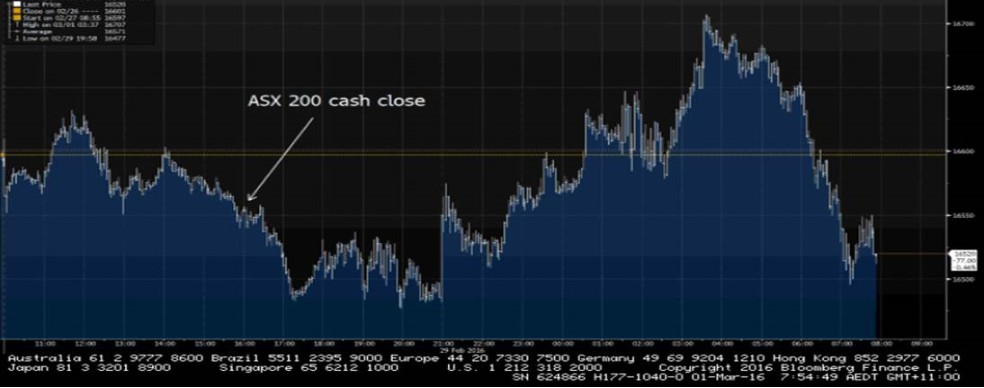

China’s surprise 50 basis point reserve requirement ratio (RRR) cut overnight has not created much excitement in the equity space. The timing seemed significant coming hot on the heels of the G20 finance ministers meeting and ahead of today’s poor batch of PMIs and the weekend’s Party Congress. Materials and energy equities have reacted strongly to the announcement in Australia, but commodities spot prices were less convinced.

The Shanghai Composite was only just holding onto positive territory today. The ASX saw strong buying in the energy and materials space. And it is worth noting that the debt markets have really been rallying strongly behind BHP and RIO after cost cutting and dividend cuts, and the equities look to be following their moves today. The compelling yields on offer in Aussie banks look to have finally brought buyers back to the markets, and ANZ was gaining the most on their compelling historically low valuation.

One reason for the lacklustre response to the RRR cuts globally is that China had already injected roughly RMB 600-700 billion of liquidity into China’s banking system ahead of the Lunar New Year holiday through open market operations (OMOs). As these OMOs rollover, this liquidity is coming back out of the market, and the 50 basis point cut to the RRR will inject roughly about RMB 600-700 billion, keeping net liquidity stable rather than adding a significant new amount.

As I’ve previously mentioned, with China set to suffer persistent capital outflows over the next couple of years, the RRR will probably need to come down to at least 10% simply to calm interbank liquidity pressures. The bigger question is how this impacts the CNY. There is a fraught debate playing out over the adequacy of China’s FX reserves with CNY short-seller Kyle Bass taking one side and PKU Professor Michael Pettis taking the other. While an interesting discussion, PBOC advisors such as Li Daokui have indicated that FX reserves of USD 3 trillion is a level the government does not want to see breached, and PBOC advisors were recommending a 10-15% devaluation in January. So downplaying the likelihood of a CNY devaluation looks a little imprudent at this point, irrespective of M2 money supply accounting methodologies.

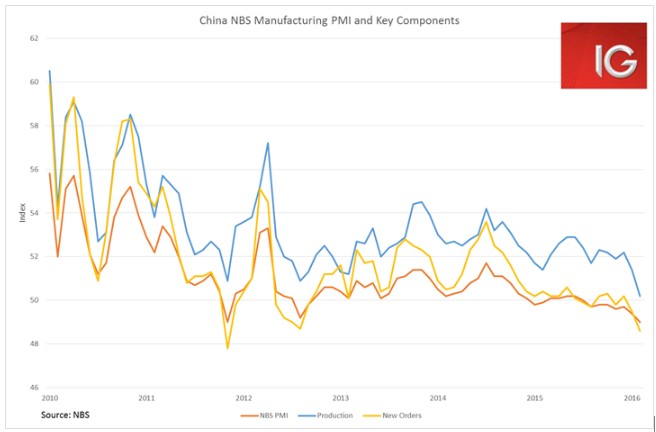

China PMIs

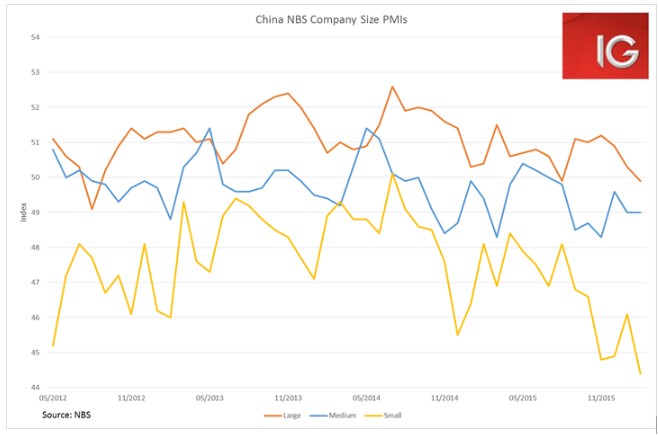

Chinese PMIs were predictably weak and while no doubt affected by the seasonal disruptions of Chinese Lunar New Year (LNY), the trend of late was pointing to further weakness in any case. In the NBS Manufacturing PMI, the key components of output and new orders both wilted dramatically. Probably of most concern was the renewed collapse in the small companies component, which contracted to 44.4. This emphasises the fact that despite the huge growth in credit in January, most of it is going to the large state-connected corporates while small and medium sized private enterprises continue to struggle. But we will really need to wait until April for the LNY distortions to start filtering out of the data before a good gauge on the manufacturing sector becomes apparent.

RBA

The RBA left rates on hold at their meeting today, making minimal changes to the statement. The board continue to be concerned about the low inflation environment and emphasis the scope for further easing. Given the notable weakness that is evident in a range of Australian data of late, the statement is relatively hawkish. The bond market is pricing in 45 basis point of cuts in the next twelve months, which means it has almost fully priced in two further rate cuts. We still think a rate cut in May is quite likely, and perhaps the change in the final sentence to “Continued low inflation would provide scope for easier policy” from “may provide” is a subtle indication of this.

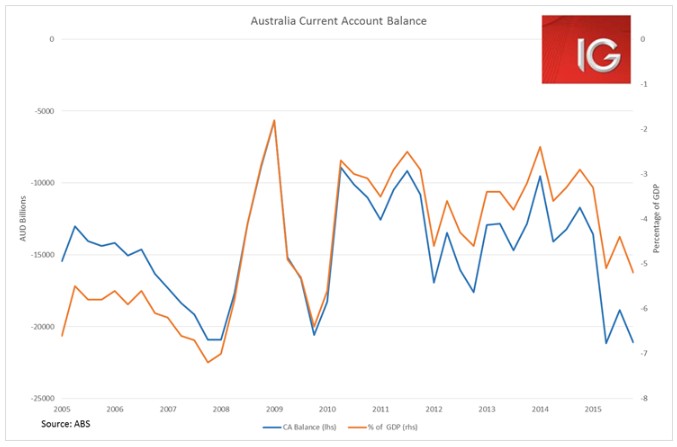

The balance of payments data today saw Australia’s current account deficit blow out to 5.2% of GDP, making the case that at least a further 10% fall in the AUD is needed to start turning this around. Net exports are set to contribute nothing to 4Q GDP, after contributing 1.5% in 3Q. The poor run of capex, inventories, construction work done and net exports have seen 4Q GDP expectations lowered.

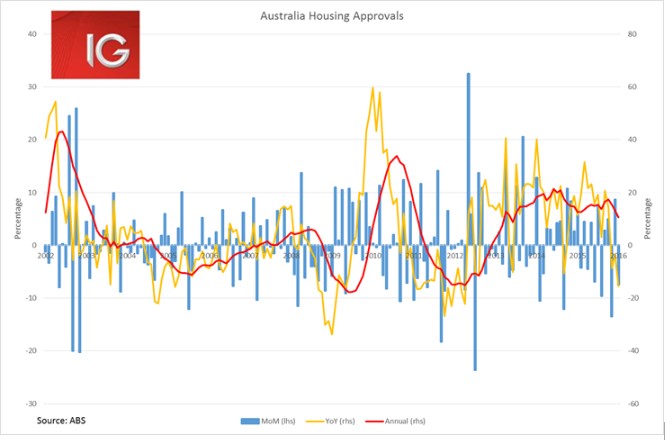

Mining capex continues to decline, exports are being impacted by the weak global environment and the housing market looks set to decline. Housing approvals saw their biggest YoY decline since April 2012 (-15.5%) in January. And yesterday’s credit data showed tightened property lending standards were slowing housing credit growth. Given all these ongoing factors and the fact that the Aussie dollar is still trading higher than it should to help rebalance the economy, further rate cuts by the RBA are needed.