Angus Nicholson for Chris Weston, Chief Market Strategist at IG Markets

G20 in Shanghai: Morning Zhou

After a few months out of the media, People’s Bank of China (PBoC) Zhou Xiaochuan made his second appearance in a week. His was keen to emphasise that while PBoC monetary policy will be “prudent”, there was “a slight easing bias”. Taken alongside Ministry of Finance proposals that China can afford a fiscal deficit of 4% of GDP, further stimulatory support does look forthcoming in 2016.

However, Zhou Xiaochuan is unlikely to be able to abide by all his statements today, at least if we take them at face value. He stated that monetary policy had “a slight easing bias”, that FX reserves will be kept at adequate levels, and that there is “no basis for sustained yuan depreciation”. While all of these statements are reassuring to the market, only two out of three of those statements can be true in the long term. If there is further monetary policy easing, the pressure for further CNY depreciation will sap FX reserves if the currency isn’t allowed to weaken. While China has the means to pause the exchange rate at current levels for a few months, once FX reserves drop below US$3 trillion, it is only a matter of time before a major one-off devaluation becomes the best course of action. China’s domestic liquidity situation in the face of growing NPLs needs an ongoing easing of monetary policy and the CNY will have to weaken alongside it.

USD influence on the Aussie and the Kiwi

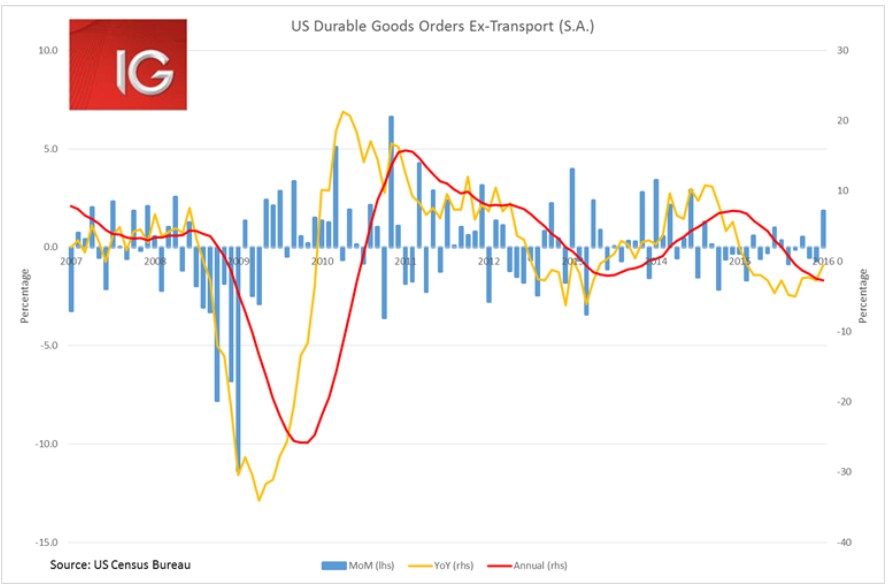

Markets overnight did look a bit undecided as to whether they should give greater weight to the improving capital and durable goods numbers or the 10,000 jump in weekly jobless claims. The stability that is starting to come through in the durable and capital goods numbers is a clear positive for the US economy and shows the impacts of the strong USD are starting to wane. Durable Goods Ex-Transport orders and Capital Goods Non-Defense Ex-Aircraft both saw their biggest month-on-month increase since June 2014.

Despite this, the buoyancy of the oil price has lowered volatility and increased demand for risk assets. The Aussie and Kiwi dollars have been clear beneficiaries of this. But the US data flow will be key in dictating their future directions. The early-March release of Markit and ISM PMIs for the US look set to be major market movers. The flash Markit services PMI yesterday dropped into contractionary territory below 50, if that number holds and the ISM non-manufacturing sees a similar drop, the USD is set for a further big fall. But if the Markit flash estimate proves to be overly negative and we start seeing some stability in the manufacturing PMIs, the Aussie and the Kiwi could be set to drop, particularly given market pricing for rate cuts by both central banks in Q2.

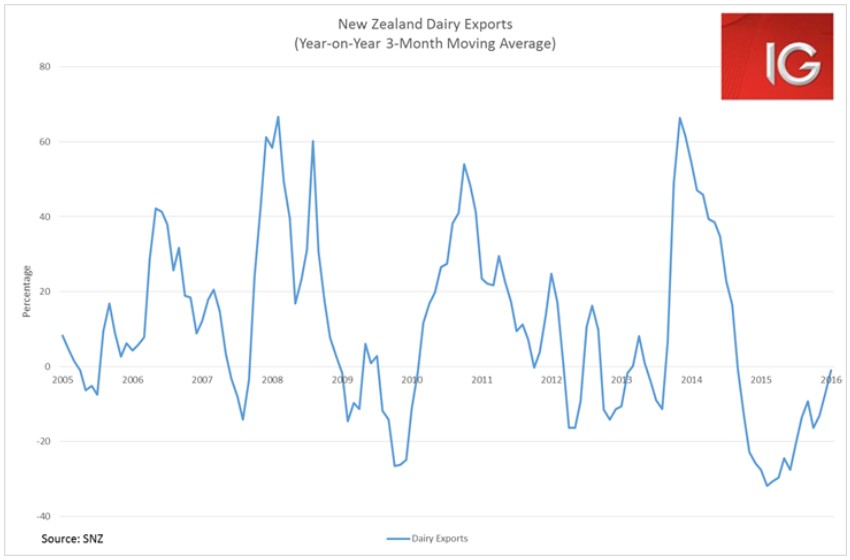

The Kiwi is surging against the USD of late. Today’s Kiwi trade data also provided further upside with much better-than-expected exports and imports. Most notable is dairy exports which seem to be picking up at a rapid rate, partly benefitting from the collapse in prices in the second half of 2015.

The yen and prospects for further Bank of Japan (BoJ) easing

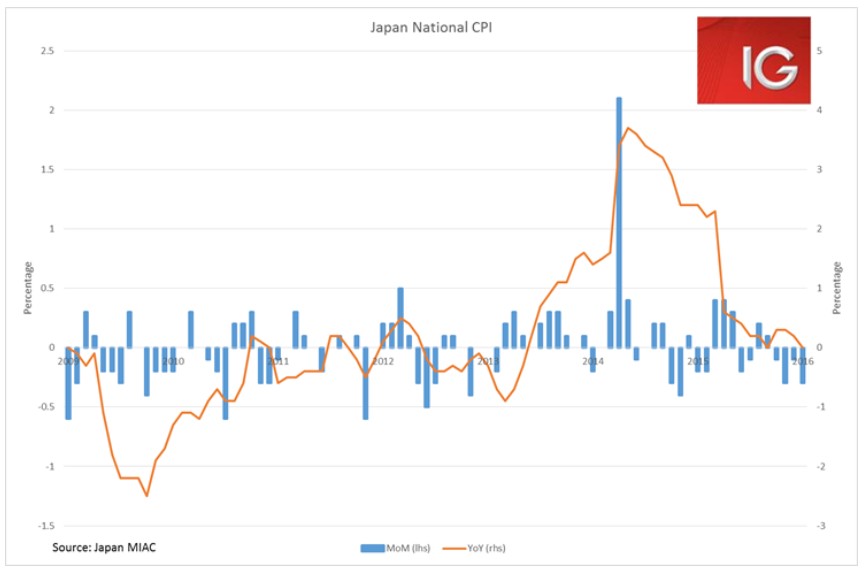

The positive moves in the oil price and the drop in volatility has reduced safe-haven demand for yen and boosted the Japanese equity markets. Today’s Japanese CPI release underscores the need for further action by the BoJ if they are determined about the 2% inflation target.

Japanese headline CPI fell back to 0% year-on-year where it was in September last year. The ex-food and energy CPI also weakened to 0.7% year-on-year from 0.8% the previous month. No doubt energy prices were primarily responsible for the weak headline number, but clearly there is a lack of inflationary pressure in other aspects of the Japanese economy. The strength in the yen will not have helped inflation either as it reduces tradables inflation.

The case for further action by the BoJ at their 15 March meeting is pretty clear. However, the introduction of negative rates at the previous meeting was responsible for the massive selloff in Japanese banks and associated selloff across Japanese equities. The introduction of negative rates in Europe did not see quite the same savaging of the banking sector, and this may be partly because they always announced an increase of asset purchases alongside them.

An increase in the BoJ’s asset purchases program seems to be what the market is demanding. But the BoJ’s QQE policy is at such extreme levels that they are beginning to run out of government bonds to buy. An extension to the asset purchasing program at the next BoJ meeting may provoke the desired JPY weakness, but there is a growing risk that the market believes the risks of further moves by the BoJ are beginning outweigh the benefits. Yet if investors really start to grow concerned about the financial instability risks from the BoJ’s program, you would think that the JPY would start to lose its safe-haven status. Lots of JPY volatility to come this year.