Angus Nicholson for Chris Weston, Chief Market Strategist at IG Markets

The weekly Energy Information Administration (EIA) inventories release gave an unexpected boost to oil prices overnight, which raised expectations for today’s Asian session. The market looked through the 3.5 million barrel increase in inventories to the first decrease in 15 weeks in gasoline inventories, which indicates growing consumer gasoline demand from cheap prices. Even with the inevitable drop after some “real talk” from Saudi and Iranian oil ministers yesterday, WTI oil still held comfortably above the US$30 handle. Oil has made a very solid double bottom off the US$26 handle over the past month, and it is looking increasingly unlikely that it will go sub-$20 this cycle (pending CNY devaluation allowing).My preferred way to play the growing evidence of the oil price bottoming is to look at high yield ETFs (which correlate very highly with oil) where you are being paid over 9% yield while you wait for prices to pick up.

Expectations in Asia are high for there to be an announcement from the G20 meeting in Shanghai tomorrow. Chinese officials have reportedly put the kibosh on any discussion of a major CNY devaluation, and have also dismissed the idea of some sort of Plaza Accords II deal being announced. People’s Bank of China governor Zhou Xiaochuan is set to hold a press conference at 12.30pm AEDT (9.30am in China), which could well be a market mover. Given the more than 4% sell off in the Shanghai Composite at pixel time, Mainland investors might be ready for a bounce on some good news tomorrow.

Japanese markets were enjoying a bit of an oil-induced recovery alongside some weakening of the yen. However, the continuing sell off in Chinese equities has started to pull back these gains. The yen has not responded well to the introduction of negative rates, and the implicit message is markets want to see asset purchases from the Bank of Japan not further negative rates.

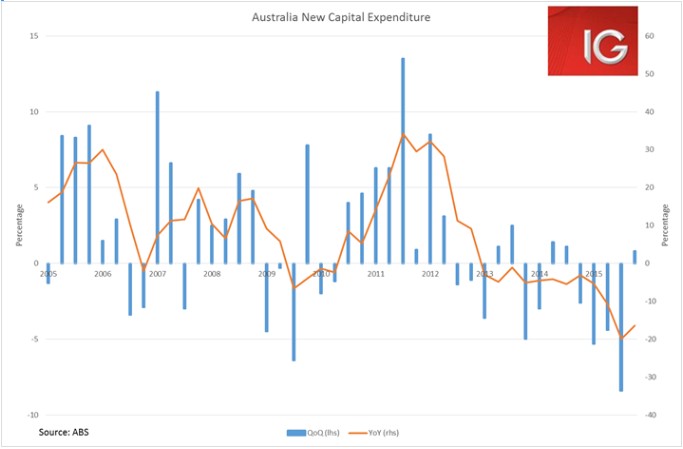

Aussie Capex and the Aussie Dollar

The Aussie dollar was among the many beneficiaries of the horrific US flash Markit Services PMI, which dropped like a stone from a prior 53.2 to 49.8. Were a similar result to be mirrored in the ISM Non-Manufacturing PMI we would be staring at a US recession this year (every time the ISM manufacturing and non-manufacturing PMIs have both dropped below 50 they have reliably indicated a recession). The Aussie surged over 1% in overnight trade, putting it in a delicate position ahead of the mood-killing quarterly Capex release.

True to form, the Aussie began to weaken ahead of the Capex release and then promptly dropped another 0.3% as the forecast Capex numbers for 2016-2017 came in well below forecasts (AUD $82.6 billion against estimates of AUD $92.8 billion).

In the short-term, the Aussie dollar’s performance looks like a battle between poor US data and poor Australian data. I think forecasts for a US recession look unlikely at the current juncture, and China concerns should be USD positive. We are still looking for a Reserve Bank of Australia cut in Q2, and another in 2H, with the Aussie dollar below US$0.65 by mid-year. The possibility of a major one-off devaluation by China’s central bank would open the possibility of the Aussie dollar at US$0.60 or lower.

ASX

The ASX has struggled to overcome the poor performance of the banks and miners today. Moody’s rating downgrade of RIO to Baa1 from A3 even after their elimination of their progressive dividend policy seems to have continued clouding expectations for the miners.

Nonetheless, smaller market cap areas of the market had a pretty decent day. IT stocks had a great day as Iress, Seek and MYOB all released strong results, helping push the sector up for a 1% gain.