Angus Nicholson for Chris Weston, Chief Market Strategist at IG Markets

The RBA decision today played out almost exactly as expected. Rates were left unchanged and a slightly stronger easing bias was evident in the wake of the sharp selloff seen in January. China gained a new mention in the first paragraph, and risks around its economic slowdown, wildly volatile equity markets and the devaluation of its currency are very much a concern for the RBA. However, the rapid slowdown of the housing market did not warrant the same concern, with the RBA still relatively upbeat about the domestic economy.

But bets for a rate cut by June have been greatly strengthened by the introduction of the final line: “Continued low inflation may provide scope for easier policy, should that be appropriate to lend support to demand.” Inflation and China look to be the primary drivers of interest rate policy.

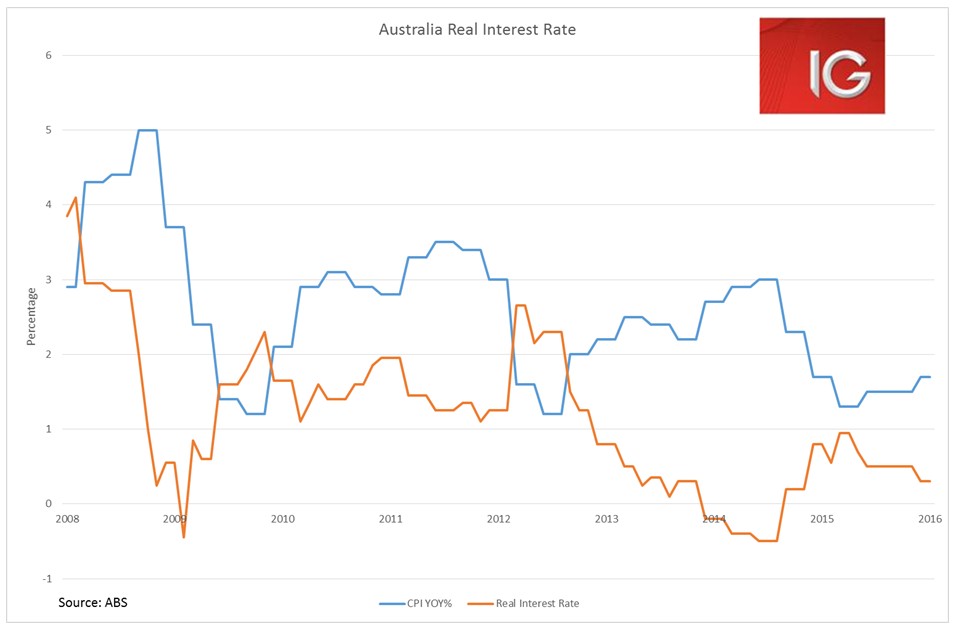

The Aussie dollar dipped soon after the statement, with the prospect for further rate cuts driving it down. Despite the prospect of further rate cuts providing greater stimulus for equities, the ASX began to sell off sharply after the decision. If we had two more rate cuts by the RBA and inflation held at 1.7%, Australia would have negative interest rates. This provides no incentive to put one’s money in bank deposits, and provides a strong incentive to seek out low-volatility, high-yielding stocks. This largely boils down to increased demand for the Big Four banks, Telstra and utilities (particularly AGL).

The race to zero in the Antipodes

Markets are heavily positioned to see rate cuts from both the RBA and RBNZ this year, but the question is: who will cut first and who will cut the most by the end of the year? The RBNZ’s January meeting already laid a pretty clear case for a series of rate cuts this year. And a range of economic indicators are increasingly showing a rapid deterioration in economic activity in New Zealand. At the current juncture, the RBNZ is looking like it will have to cut rates harder and faster this year, while the RBA is likely to cut slower and later. This scenario not only indicates a roughly 8-10% downside for the AUD and NZD against the US dollar this year, but also in the near term the AUD/NZD has 4% upside potential as it re-tests its highs of NZ$ 1.13.

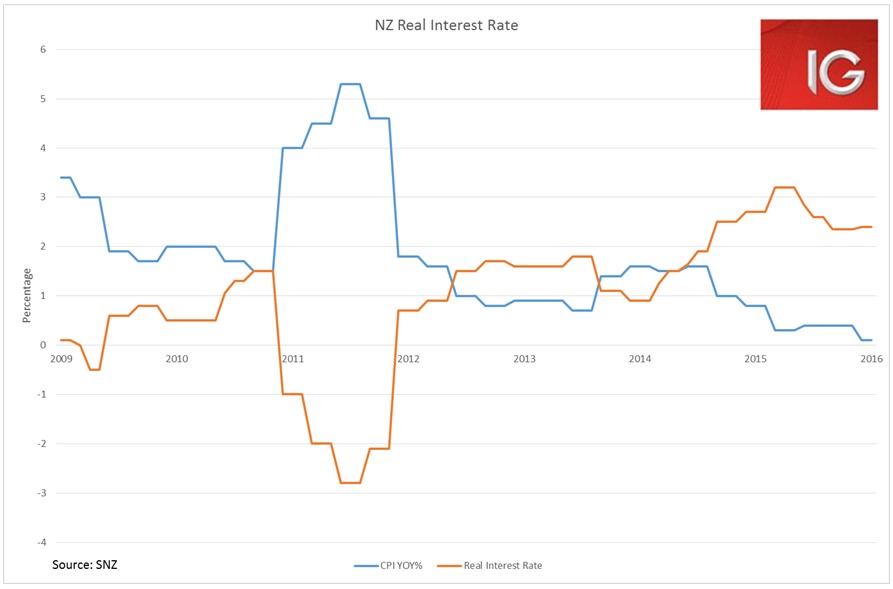

The most pressing concern for the RBNZ is the risk of deflation. Headline CPI for Q4 was 0.1% YoY, which means that despite four interest rate cuts in 2015, real interest rates are still sitting at 2.4%. New Zealand employment growth saw the first quarterly decline since 2012 in Q3, and dairy prices, its key export, have been falling away at a rapid rate in 2016.

The main issue that has seen a pause in more drastic cuts by the RBNZ has been financial instability concerns over the rapid growth of the housing market. But growth in house prices and house sales has been falling rapidly since peaking in August and September 2015. With momentum falling out of the housing market, and FX controls on Chinese citizens minimising foreign demand, housing financial instability is set to be less of a concern in 2016.

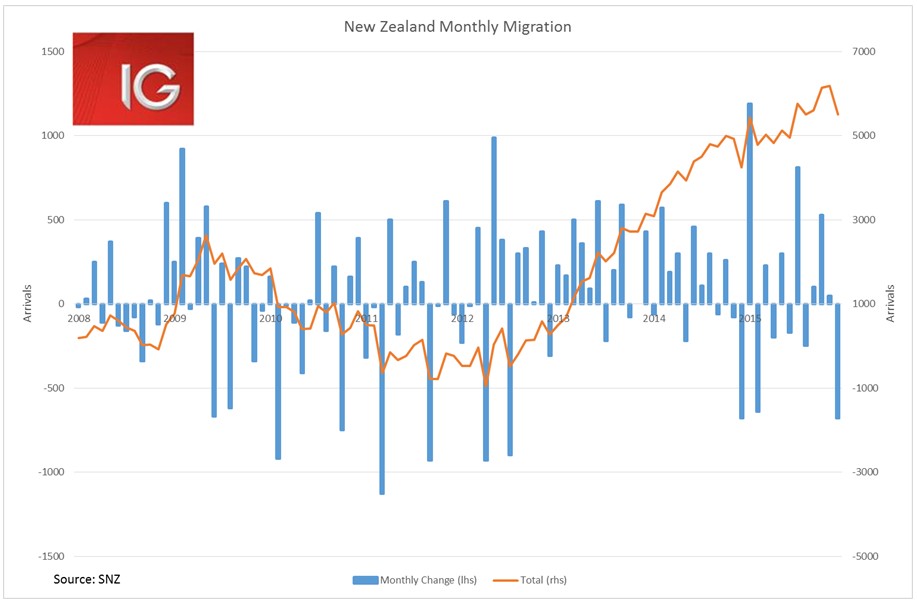

But the most stalwart indicator of the AUD/NZD is the migration data for New Zealand, with growing migration an indication of NZD strength. However, December may well have been the turning point in rapid migration to New Zealand. December saw the biggest monthly decline in net migration to New Zealand since July 2012 (apart from December 2014, which declined by the same amount). Obviously, seasonal factors around people returning home for Christmas are at play as well, but the correlation with the decline in employment growth does indicate a more notable turning point. And possibly a strong indication to be long AUD/NZD.