Angus Nicholson for Chris Weston, Chief Market Strategist at IG Markets

The two dominant macro influences on markets of late, China and oil, have diverged over the past 24 hours of trade. The good news for investors is most markets (bar the ASX and Shanghai Composite today) seem keen to follow oil higher. The fact US and European markets were able to ignore the more-than-6% selloff in Chinese equities could mean markets have reached a saturation point for negative moves in Chinese equities.

While this is a positive for markets, the ephemeral moves in oil off the back of rumours of a deeply complicated deal for production cuts by Russia and Saudi Arabia do not necessarily bode well for continued equity gains.

A blowout in the EIA inventories number this evening (consensus: 4.37 million barrels, data out 02.30 AEDT) could be the proximate cause for another trip back into the $20 handle for oil. Certainly, current futures predictions for US and European markets are pointing to a tougher session than yesterday.

- Chinese markets look like they will continue to sell off until their last day of trading before Chinese New Year on 5 Feb. There is a good chance that Chinese equities may find their cyclical bottom in the next week and half if the current pace of selloff continues. I’ve previously pointed to the Shanghai Composite bottoming around the 2500 level (although that seems to be a crowded prediction in the analyst community of late). Given this level has been so widely emphasised in the press and among Chinese traders, I think there is a good chance of the market overshooting it and touching levels in the 2300-2400 region. One theory I strongly disagree with is the idea the state will intervene strongly at the 2500 level. The state is not going to waste valuable resources bailing out the stock market (again!) at 2500 when it is approaching a natural rebalancing level. Today’s further decline in industrial profits will not have helped market sentiment in China either.

- The major macro-economic risk this year is a large one-off devaluation by the Chinese government. Particularly, as China’s FX reserves approach the stipulated “red-line” of USD 3 trillion for reserves, as mentioned by PBOC advisor David Li Daokui, a major decision about the currency is likely to be thrust upon the Chinese government. Capital outflows through the difficult-to-control trade channel are growing as the government closes down the easier-to-use channels. This is most evident in China’s trade statistics with HK, with the jump in Chinese-reported imports from Hong Kong discreetly hiding FX flows. There was also a huge 62.4% month-on-month jump in gold re-exports to China from Hong Kong in December, another well-known FX flow proxy. A big move downward in the Chinese yuan this year does look increasingly likely. As one trader says, “It’s a popular trade. I can’t imagine a single western hedge fund has got short dollar-(yuan).”

- China’s economic slowdown and increasingly tight FX controls are certainly adding to the slowdown in the Australian housing market. A sharper-than-expected slowdown in the housing market and the potential for a devaluation in the Chinese yuan are the major reasons we are looking towards two potential cuts this year by the RBA. The argument is that housing and weak activity data could prompt the cut in Q2, and a China devaluation might prompt another cut by year-end. I would also argue that this two-legged call would see the AUD move US$0.65 for housing/activity reasons, and US$0.60, were a major CNY devaluation to occur.

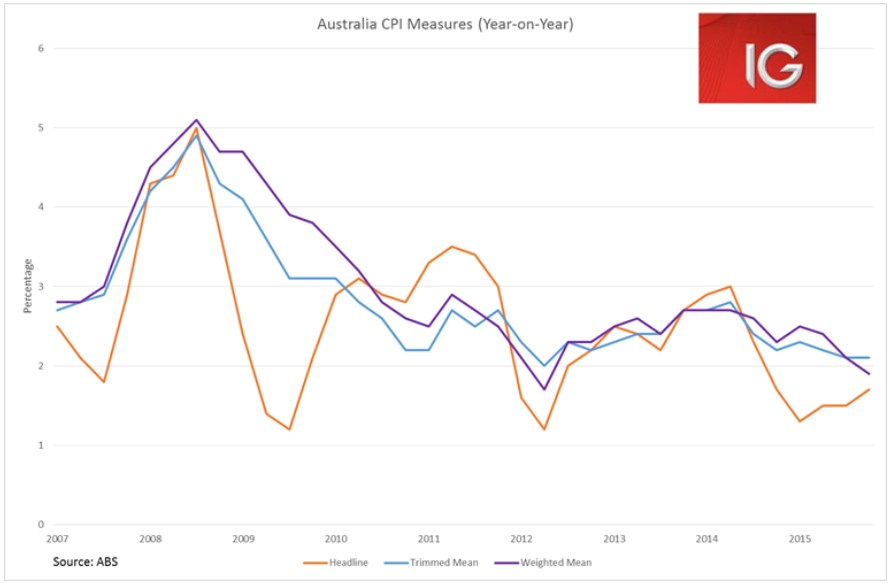

- However, the better-than-expected Q4 CPI release today did provide a little upside to the Aussie dollar and saw bond market pricing for an interest rate cut fall back. We had Q4 CPI pencilled in as 1.7-1.8% YoY, so the 1.7% increase was not a huge surprise. The lower Aussie dollar is not only seeing a boost to tradables inflation, but also spurring increased demand for other goods and services. There are green shoots in the Aussie economy that the RBA are unlikely to want to see dissipate, and even inflation growing at 1.7% YoY is unlikely to be a concern for the RBA if they decide to cut rates when their target is 2-3% YoY.

- ASX: The ASX hasn’t had a great session trying to catch up with global markets after its Australia Day closure yesterday. The selloff in Asia yesterday and the solid US session overnight left it opening relatively unchanged from its Monday open. However, the falls in the oil price seen in the Asian session and ongoing declines in Chinese equities seemed to be major reasons behind the slide in the ASX.

- The banks and energy stocks were hit the hardest on the market today. Energy stocks were hit by the pullback in the WTI spot price in the Asian session as the market positioned itself for a blowout in the EIA inventories number tonight.

- The general concern about the market and the economy seemed to weigh particularly hard on the banks today. However, news that NAB had successfully voted to demerge its Clydesdale assets in the UK did seem to be causing some investor upset in the market seeing it underperform the sector as a whole.