Angus Nicholson for Chris Weston, IG

China fears have again dominated Asian markets today, and then later in the day a large North Korean nuclear bomb test added a touch of Armageddon fears to the markets as well. Asian markets were down slightly in early trade, but the unexpectedly weaker CNY fix appears to have pushed all Asian markets down a leg more. After a “triple-threat attack” yesterday of direct equity market intervention, direct FX market intervention and the injection of CNY 130 billion of reverse repos into the interbank market hopes were for China concerns to dim today. Yet despite the onshore CNY strengthening 0.3% yesterday, likely on FX “National Team” buying, the CNY mid-point fix today was 0.2% weaker.

FX and equity markets did not take the CNY surprise well, despite what looks to be further intervention in the Mainland markets. The spread between the onshore and offshore CNY has now reached some of the highest levels in the pair’s history – a clear indication of both volatility and intervention.

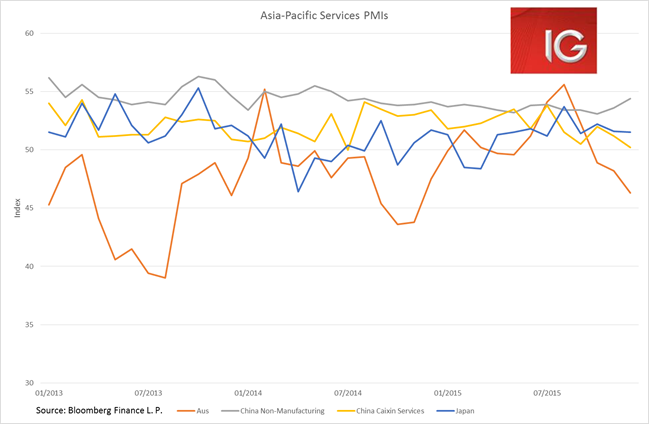

There was little joy to be had in the Caixin Services PMI release today either. With hopes for the Chinese economy increasingly tied to its services sector, greater importance has been given to the monthly services PMIs. So to see the Caixin Services PMI fall to its lowest level since July 2014 is quite concerning, particularly given the fall also seen in the Caixin Manufacturing PMI on Monday.

And yet, FAI, industrial production and the NBS PMIs all clearly displayed improving Chinese activity in November and December, but how could this be? They made up the statistics goes the call. Well, maybe, but a closer look at the NBS PMI sub-sector components does actually explain the divergence. The performance of the small and medium enterprises in the NBS manufacturing PMI is very consistent with the weakness seen in the Caixin PMI, with small enterprises recording readings of 44.9 and 44.8 in the past two months – deep in contractionary territory. The Caixin PMI is far more weighted towards private sector small and medium enterprises (SMEs). What looks to be happening is the Chinese government’s fiscal and monetary stimulus has not been reaching the SMEs, while larger state-owned corporates are readily finding access to capital.

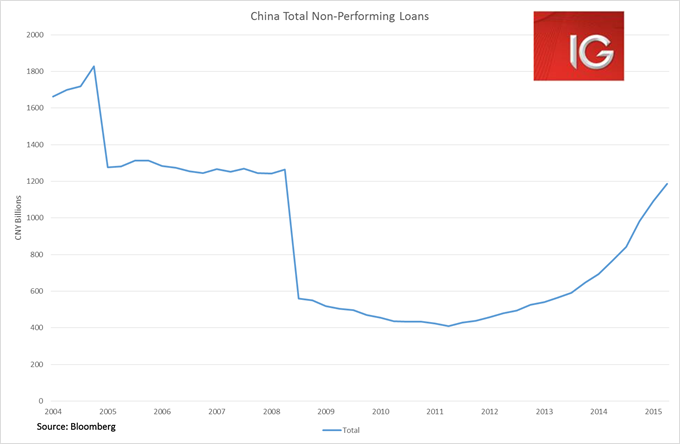

Unfortunately, this is not a new story. China’s form of top-down centrally-controlled Leninist governance has always been very good at directing resources into fixed assets dominated by the secondary sector. Yet, growing the private sector is more about removing barriers to entry rather than central directives to spend. Provincial governors have also always had far more of a penchant for tangible physical investments rather than less obvious storm water systems or grand IT infrastructure overhauls. Access to credit for SMEs has been a constant problem, but overhauling the state banking system with private sector competitors who may have more inclination to lend to SMEs has never been high on the government’s list. Growing non-performing loans in Chinese banks are clearly impacting access to capital for SMEs, and much of the stimulus we are seeing from the government looks to simply be rolling over loans for large SOEs.

ASX

The ASX was rocked by another day of indiscriminate broad-based selling more driven by perceived market risk rather than any specific company factors. The market was looking like it would see a 2% loss today, but managed to pull back above the 5100 level. Unfortunately, if trade over recent months is anything to go by the selloff in the ASX still has more to run.

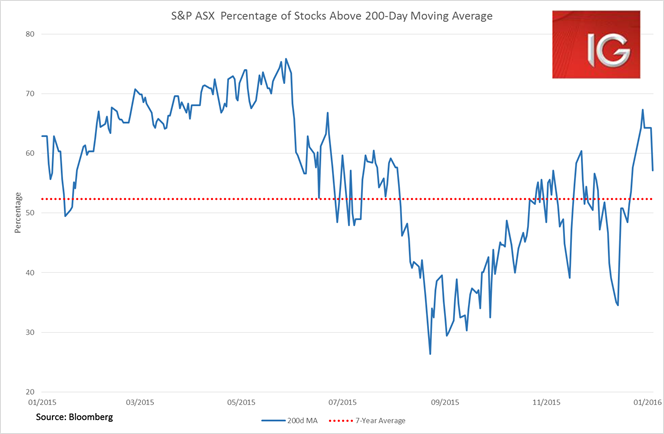

The selloffs in the ASX that began at the end of October and the beginning of December continued until they dropped below the 5000 level. The market internals do not give much faith either, in previous selloffs the market did not turn around until the number of companies trading below their 200-day moving average fell below 40%. Currently, 56% of companies are still trading above their 200-day moving average, which could mean the market has quite a way down to go yet.

The selling on the ASX has been most concentrated in the materials and IT sector today. China concerns have been hitting commodities, and overnight the iron ore price broke its longest winning streak in four years. Fortescue’s stock did not react well to the price drop, losing over 5% today.

But the banks were very much a driving force in the selloff today, with financials losing 1.3%. It will be very difficult to see the ASX turning around until the banks start finding buyers due to their large market cap on the index.

Ahead of the European open we are calling the FTSE 6095 -42, DAX 10212 -98, CAC 4511 -27, IBEX 9279 -56