Angus Nicholson for Chris Weston, Chief Market Strategist at IG Markets

After the terrible tragedy seen in Paris on Friday evening (and also the bombing in Beirut), markets have seen some of these fears play out in the financial world.

There was a slight but noticeable buying in gold and safe-haven currencies such as the US dollar and Japanese yen. Oil also saw a bit of an increase off its two-and-a-half month lows from concern about what the Western response may mean for Middle Eastern oil production.

Many markets opened down in Asia on the news, and futures were pointing down for European and American markets, although we did see this pull back somewhat as trade progressed throughout the day. All indications were that this negative move would only be temporary and are likely to dissipate over the coming days.

The bigger question is whether this will see an escalation of the conflict in Syria and Iraq. French President François Hollande has publicly called the attacks an “act of war” and we have already seen a retaliatory bombing of the ISIS stronghold of Raqqa on Sunday. The big question is whether France would decide to invoke Article 5 of the NATO treaty – the self-defense clause – which could see a significantly expanded presence of Western forces in Syria and Iraq. Oil price moves have been relatively muted so far, but as the probability of Western boots on the ground in Syria increases, this is likely to see a corresponding increase in the oil price.

The attacks in Paris and the ongoing humanitarian crisis from the vast amount refugees trying to enter Europe seem likely to prompt some major decisions on the Syria and Iraq conference at the G20 meeting in Turkey. The most likely scenario seems to be Western powers removing their objections to the continuation of the Assad regime, although this is unlikely to be very popular and would be seen as a major victory for Russia’s aggressive foreign policy.

Japan

Japan entered a technical recession in the third quarter as expected. Q3 GDP came in below expectations of -0.1% at -0.2% quarter-on-quarter (QoQ), although Q2 was revised upwards to -0.2% from a previous -0.3%. This will serve to reignite speculation that the Bank of Japan (BoJ) may need to step up its quantitative and qualitative easing (QQE) program. Although the BoJ would have been aware of this likely result at its meeting last month and still decided to leave its monetary stimulus program unchanged. This indicates that the BoJ is relatively nonplussed about inevitably missing its 2% inflation target for mid-2016 and that growth will have to see a more significant decline before they extend QQE. Nonetheless, despite the Nikkei opening down, the index rallied soon after the disappointing GDP result, likely driven by speculation that QQE may be extended.

The bright spot from the release was the bounce back in private consumption, which added 0.3% to GDP after contracting the previous quarter. Nominal GDP also grew 3.1% year-on-year, its strongest rate since Q3 2010. The major drags on GDP was a big drop in private inventories, which subtracted 0.5% from GDP, and a consecutive QoQ decline in private investment. The effects from inventories is expected to be temporary and GDP should return to positive territory in Q4. However, the ongoing decline in private business investment will be concerning to the Japanese government. Reforms focussed on getting Japanese businesses to start reinvesting again are very important. Prime Minister Shinzo Abe’s commitment to lowering the corporate tax rate is a good move in this direction, but should clearly be a key focus for the government with the BoJ looking increasingly tapped out in its ability to extend QQE.

Australia

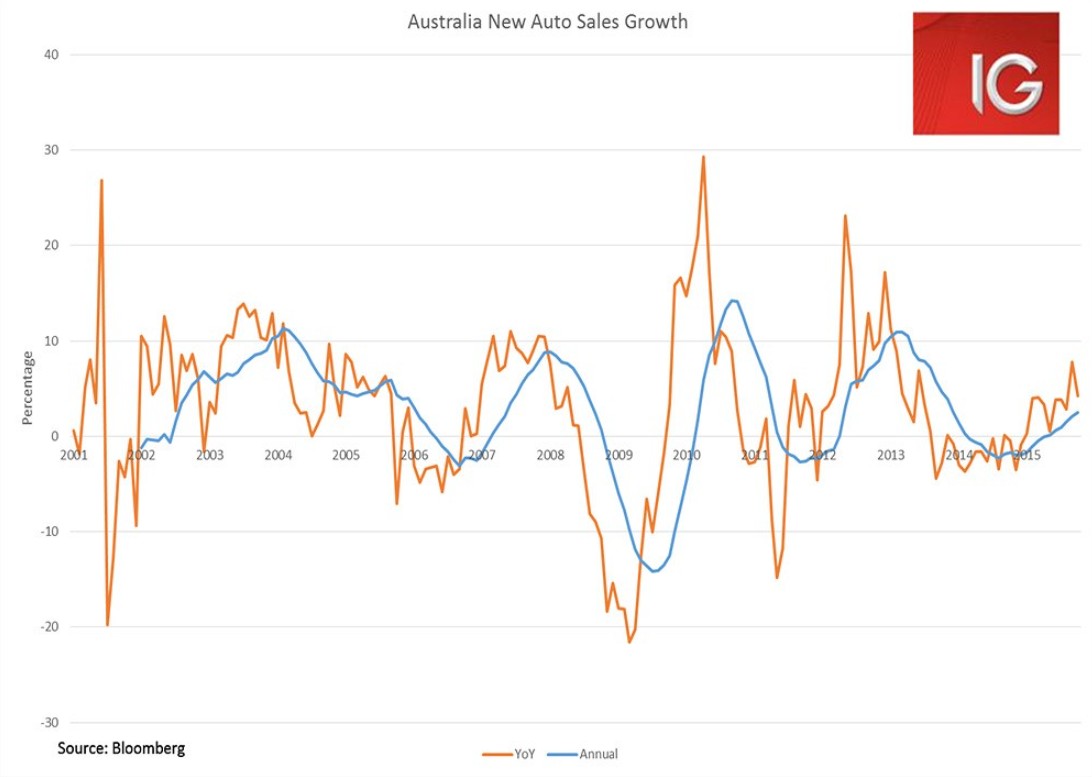

Australian auto sales eased somewhat in October from a very strong September. Auto sales grew 4.2% year-on-year (YoY) from an upwardly revised 7.8% in September. While not usually a market mover in Australia, it is another key statistic supporting the case for improved consumer demand heading into the Christmas sales period. Despite the easing in the YoY rate in October, the longer term trend seen in the annual growth rate reached 2.5%, its strongest level since December 2013. Improved consumer confidence, expanding employment and strengthening sales all continue to diminish the likelihood of rate cuts by the Reserve Bank of Australia in Q1 2016.

ASX

After plummeting 1.4% on the open as concerns over the Paris attacks saw all major futures markets selloff on Monday, the ASX looked to pare back much of these losses later on throughout the day. Fear buying around the Paris attacks saw a noticeable rise in the gold price.

This saw strong gains by the ASX-listed gold miners. Newcrest Mining, Evolution Mining, and Regis Resources were three of the top performers on the index today.

There were some gains in global oil prices over concerns about the potential for increased Western intervention in the Middle East. This wasn’t enough to bring the energy sector into positive territory, but the big names of Woodside and Santos were both in positive territory.

The banking sector did not perform well in this environment of heightened volatility. The Big Four and Macquarie all lost over 1% today, which was a major drag on the index.

The big surprise was Telstra holding up in positive territory amidst a sea of red from all the other smaller telecommunications companies. But their huge market cap weighting managed to push the sector as a whole into the green.