Chris Weston, Chief Market Strategist at IG Markets

Big day today with CBA, CSL, NWS, CPU, OZL, PRY, CRZ, AGL reporting. On the data side we get Aussie Q2 wages (2.3% exp), Japan industrial Prod, China high frequency data at 15:30 (IP, retail sales, FIA)

11:15 is key though. This will be the ‘new’ fixing mechanism from the PBoC. Recall they are looking at a much more market orientated driven fix and given spot USD/CNY closed at 6.3250, a further 1.5% from yesterday’s 2% devaluation, if the Chinese market makers move the fix in-line with the spot close some would see USD/CNY as a more freely floating currency – i.e. the market will have a greater say in where it goes.

Given on most valuation metrics the CNY is around 10% overvalued the market would naturally push USD/CNY higher…I feel long USD/CNH (offshore RMB and tradeable with IG) is a good, low vol long term play here.

Anything leveraged to the Chinese consumer was hit fairly hard overnight and the perception of a weakening RMB will do that (think purchasing power).

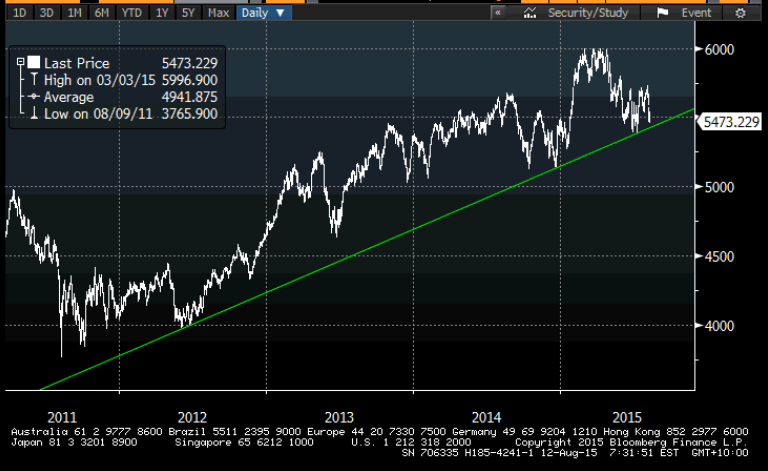

Still, it is the must watch of the Asian session (along with CBA earnings). I think the 2012 uptrend (currently 5440) on the ASX 200 will be taken out on open, with our call 5430, so a close around here will clearly be negative.

China is deporting its deflation to the world again. This is partially down to poor export data but a belief that the Fed will raise this year and the USD is only going one way. They are prepared to accept capital outflows and a burden on the corporate landscape given the level of USD denom debt most corps hold ($856b in March – SAFE).

For what it’s worth the implied probability of the Fed moving in September has dropped to 44% from 54% a day or two ago, with the 2-yr US treasury reflecting that -5bp on the day.