Let me explain.

To do this I first need to be clear about why rents are not a feature of current mainstream economic reasoning.

You may not realise it, but in the neoclassical market model capital inputs are all leased by firms, and compensated are their marginal contribution to production. This leads to a very circular analysis and an inability to properly understand the concept of rents.

For example, when we whittle our way through the production chain down to the landowner, who has one input, land, the neoclassical framing say that this owner rents their land inputs, which are compensated at their marginal contribution to production. Okay. So she rents off another person who owns the land, who we then model as renting from another person, and so on.

The buck never stops.

That’s what happens when you conflate land and capital into a single input. They nee to be treated differently because land is not an output of any production process, unlike capital.

When you allow the buck to stop at ownership of land and natural resources, you get a very different picture of the economy. One in which the taxation capacity of rents is not limited their current value. As Gaffney points out, when we “lower other taxes, the revenue base is not lost, but shifted to land rents and values, which can then yield more taxes”.

Henry George made this argument concisely a mere 130 years ago when writing in 1881 about the fund from which taxation is drawn

It may seem like a truism to assert that the only fund upon which taxation can draw is that made up by the produce of the community, and that to multiply the places at which it is tapped is not to increase its capacity to yield.

To be more clear I will use a very simple and abstract example to show how reducing taxes on wages increases the taxation capacity of land.

Imagine two households – household A owns all the land, and household B rents the land on which their home sits from household A. It’s a big abstraction, but I need to make this point clearly.

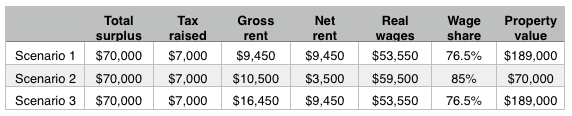

The renting household earns $70,000pa in wages, and pays 10% of that in taxes. The government raises $7,000 via taxes on incomes each year, meaning the net income of that household is $63,000.

Household B bids up to 15% of their take-home income on their preferred housing location, meaning they pay $9,450 in annual on rent for the land on which they reside. They pay all the costs of building and maintaining the structures on the land.

Household A, which owns all the land, does not work and receives as their income the $9,450 in rent paid by household B. If the market interest rate is 5%, that means the value of the land on which household B resides is $189,000.

The total surplus in the economy is the wages plus taxes plus rents, or $70,000 in this case. Remember, we don’t want to double count the $9,450 as wages, because in real terms, they are merely what is left over after paying taxes and rents. I summarise this setup as Scenario 1 in the table below.

Now consider what happens when the total tax burden is shifted to land.

This means that household B has more money to spend on rent because tax is not taken from their wages. If they continue to bid up to 15% of their income on housing location the rent is now $10,500 (shown as Scenario 2 in Table 1). The annual rent received by the land owner is 11% higher because taxes have been removed from wages, which increased the taxation capacity of their land.

To maintain a constant $7,000 tax revenue a land tax rate of 10% is required [1].

A third scenario drives home the idea that all taxes come from rents. In this case taxes are removed from wages and added to rents, but household B bids up the rent to a point where their real wage is identical. They now pay $16,450 in rent, which is the sum of the rent and taxes they paid in Scenario 1.

The land owner then pays the taxes and is left with an identical income. Thus, we can see that it is technically possible to switch all tax revenues to land without affecting the incomes of different actors in the economy.

The following table summarises this example economy under each taxation scenario. In reality, shifting to land taxes would involve something between Scenarios 2 and 3.

We also need to think carefully about this result in terms of debates about housing affordability and land taxes as a possible solution. While Scenario B has a much lower land value, both of these scenarios have land occupation costs of 15% of take-home wages.

What makes housing Scenario 2 more affordable is that the 85% of wages left over after land costs can buy more goods than in Scenario 1. 11% more in fact.

This exercise has demonstrated that indeed whatever current taxes are being raised can be raised through a single tax on land and natural resources. It provides a brief and very simplified look at the mechanisms whereby reducing taxes on labour increase the taxable capacity of land, and the distributional impacts of doing so.

Please share this article. Tips, suggestions, comments and requests to rumplestatskin@gmail.com + follow me on Twitter @rumplestatskin

fn[1]. Which we ascertain from solving the two equations:

value =(rent-tax_amount)/i

tax =value*tax_rate