I don’t know how best to say it, so here it goes – the current mainstream theory of the firm is dodgy. Real dodgy. Put simply, the theory of the firm that we all know and love tolerate, is a neat mathematical construction contrived to support an already established, but flawed, theory of markets.

If we want to make real progress in economics we need a new theory of the firm upon which we can build a theory of markets; fully informed by empirically observation and able to generate realistic predictions about production, trade and prices.

Is that too much to ask?

I stumbled into this challenge. In first year economics, when the supply curve was shown as upward sloping, the annoying undergraduate in me asked: why? When we get on to exactly why the supply curve is upward sloping, lo and behold, it is simply a representative firm’s marginal cost curve. Amazing!

But wait. If that’s true then firms operate at a point where there are diseconomies of scale. Yet didn’t most goods come down in price as output increased? What happened to the whole idea of economies of scale?

Oh what’s that? You’re getting confused between the short, medium and long run young grasshopper, of course there’s economies of scale, but we don’t lose anything from the analysis by assuming they exist only in the long run.

Tell me more Obi-Wan.

It was far too ad hoc for my liking. The contrived concept of short, medium and long run, is to all accounts quite inconsistent, since all periods of time must be part of all ‘runs’. But as a good economist-in-training I shoved my doubts back into the suppressed deviant skeptic part of my mind and accepted that marginal costs probably slope up. Surely the chaps with all those PhDs must have some empirical insight about this ‘fact’.

Except they didn’t. And they don’t. Alan Blinder made that clear after surveying firm managers about their cost structures and operations. He said

The overwhelmingly bad news here (for economic theory) is that, apparently, only 11 percent of GDP is produced under conditions of rising marginal cost. … firms typically report fixed costs that are quite high relative to variable costs. And they rarely report the upward-sloping marginal cost curves that are ubiquitous in economic theory. Indeed, downward-sloping marginal cost curves are more common…

If these answers are to be believed … then [a good deal of microeconomic theory] is called into question…

There are numerous other studies showing this to be the case – that flat or rising marginal costs are the exception rather than the rule.

So do I trust the contrived theory of the firm? Or do I trusted the empirical record? Personally, I prefer to start from observation, so I’m siding with the empirical record.

Which altogether leads to another conundrum – the heart of economic theory, that equilibrium is found where marginal cost equals marginal revenue, can no longer be accepted. Some other mechanism must be at play in the determination of prices generally.

My own experience in business, and the repeated challenges to the theory of the firm, finally revealed to me what was missing from the theory.

Returns.

It’s strange to think how in economic commentary the rate of return and profit are terms used almost interchangeable. Even Milton Friedman did this from time to time, saying that ‘firms behave as if they were seeking to maximise their expected returns’. He did a poor job of clarifying what he meant by returns, only that he uses the term profits as the realised ex post version of the ex ante expected profits, which he labels returns. Strange but true.

The foundation of economic theory is actually centred on profit-maximisation, being the maximisation of revenue minus costs. Returns, by every definition apart from Milton Friedman’s, are profits divided by costs. Colloquially, profits are ‘bang’, and returns are ‘bang for your buck’ – and I’ve never heard of anyone trying to get the best bang without trying to economise on the buck.

Just think of Milton Friedman assessing a production plan before a company board:

MF: This project will earn a return of $10m!

Board member: Great! But a return of $10m on what?

All the more strange is that Avinash Dixit and Robert Pindyck made the astute observation twenty years ago that in the real world of uncertainty, and where investments in new businesses and expansions are risky and costly (meaning firms have a real option to delay incurring costs to increase production levels), that maximising the firm’s overall rate of return maximises its value.

So if maximising the rate of return is ubiquitous in financial analysis, and has strong foundations in economic analysis under realistic market conditions, why hasn’t our theory of firm production been updated to address this? Well, today it has.

We – myself and co-author Brendan Markey-Towler – have released a working paper outlining a new theory of return-seeking firms. And to our surprise, what seems a rather minor change in the firm’s objective function leads to a variety of results consistent with the empirical record, and with many alternative theories of firm production and pricing (such as mark-up pricing).

What did we do?

First, we relaxed the assumptions about market conditions. Rather than the unrealistic free entry and exit and perfect knowledge of the future which define most models, in our world firms face uncertainty, have irreversible costs, and can delay investment to future time periods. As per real options theory, these conditions give rise to our firm objective of return maximisation.

Next, we allow competition to enter the model via the shape of the firm-specific demand curve. The firm specific demand curve can be specified to include the supply of other firms producing substitute goods, and the parameters of the curve can be varied to reflect differing intensity of competitive pressures.

We do this because the usual model condenses similar products into a single market, yet there are almost no examples of markets where the goods produced by different firms are perfectly interchangeable. Hence, competition is a process of return-seeking between firms competing in close substitute goods.

This conception of competition also predicts non-price competition which aims to reduce the price sensitivity of customers, such as loyalty schemes and other incentives, and of course, product differentiation. Because of the way market competition is conceived in our new model, there is no need for the arbitrary conceptual leap between a downward-sloping market demand curve, and a horizontal curve faced by a firm in a competitive market. All firms operate in their own markets, whose demand schedule is influenced by the offerings in substitute markets.

One thing that is consistent with the traditional model of markets is that the more competitive a market the firm faces, in terms of having a flatter demand curve (more price sensitive customers who have more substitutes available), the greater their output with a specific level of capital.

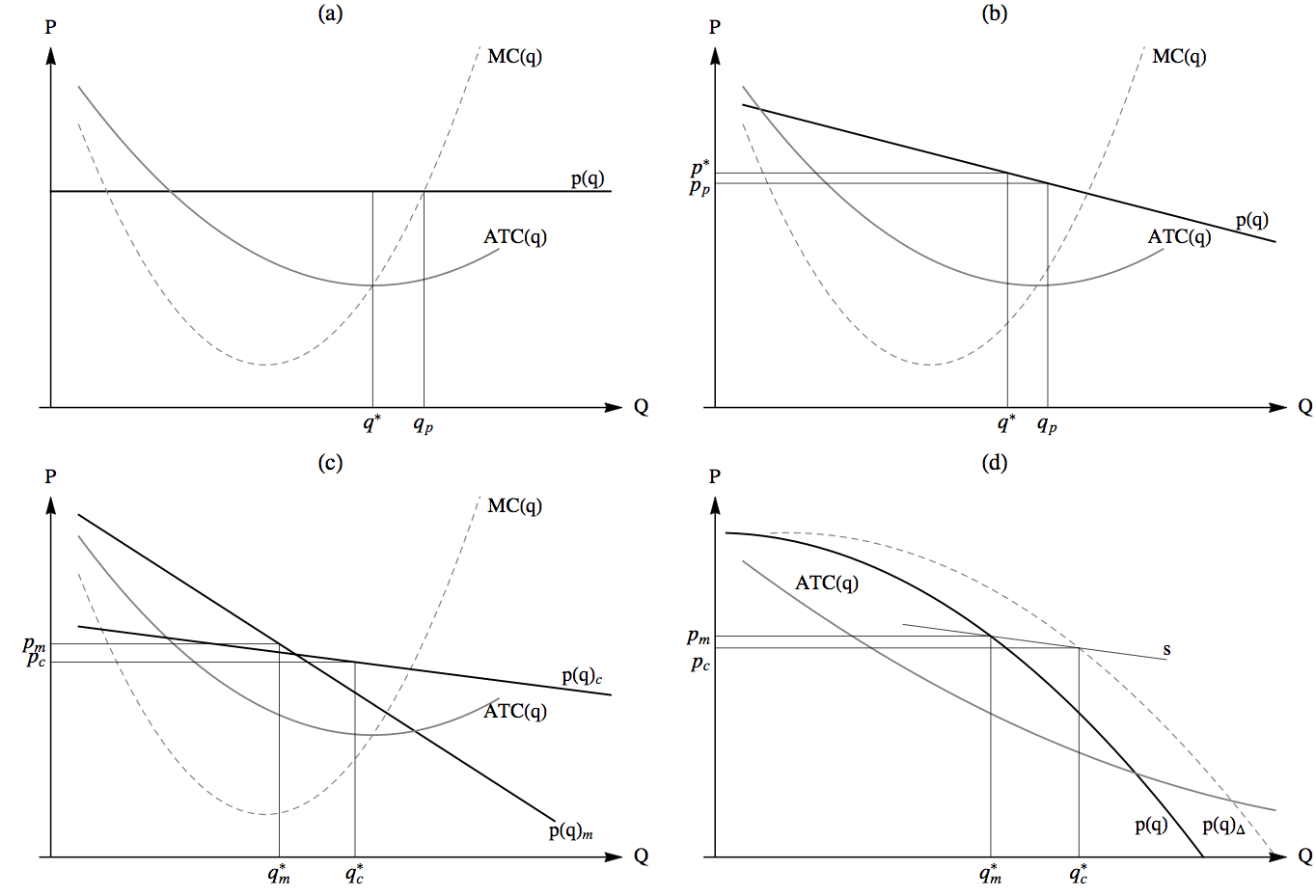

I show this in panel (c) of the figure below, where competitive (q*c) and monopolistic (q*m) outputs are chosen when the same firm faces a competitive demand curve, p(q)c, or a monopolistic-type demand, p(q)m using the same capital inputs.  Third, firms choose their inputs and output level to maximise their rate of return. This means that the price is above the marginal cost (and above average cost) such that mark-ups over cost are a feature of firm accounting structures. It also means that there must exist some economies of scale for firms to produce at all.

Third, firms choose their inputs and output level to maximise their rate of return. This means that the price is above the marginal cost (and above average cost) such that mark-ups over cost are a feature of firm accounting structures. It also means that there must exist some economies of scale for firms to produce at all.

In the special case reflecting a traditionally perfect market (firms face a horizontal demand curve), return-maximising firms do not respond to changes in demand. They produce at the point of minimum cost at all times, as long as prices are above costs (shown as point q* in panel (a) of the above figure). Hence there is no supply curve as such in this market.

Indeed, even under imperfect markets, where firm-specific demand curves are downward sloping, the path of a firm’s supply response to a change in demand depends both on the shape of their cost curve and the shape of their demand curve. Hence, there is no supply curve, merely a response to changing market conditions conditional upon a firm’s cost structure. This has implications for long run trends in the relative prices of different goods. For example, goods limited natural supply, such as land and mineral resources, will increase in price relative to manufactured goods where economies of scale dominate.

In panel (d) we show that the emergent supply response can lead to what some might call a downward sloping demand curve (following a rightward shift of the demand curve from p(q) to p(q)delta).

Fourth, we make the input and output space of the firm discrete, meaning firms can only produce goods in discrete quantities, or batches, and can only choose capital inputs in discrete amounts. This is highly relevant to the capital debates, which demonstrated the inadequacy of capital aggregation. In our model firms face discrete choices in their capital investment, allowing ‘lumpy’ capital units, and various production techniques to be exclusive choices for firms.

The discrete nature of firm choices also means that firms are almost never going to be at their optimal point – they will be seeking to get there but typically they will be unable to because the optimal point is between two discrete choices. Hence we call the model one of return-seeking, rather than maximising, firms.

Such a disequilibrium approach allows for interactions between investment paths of firms across the economy as each firm’s slightly imperfect decisions cascade into those of other firms, resulting in a business cycle driven by capital investment choices. For example, a large firm in a region undertakes a capital project, thereby increasing the income of the workers, who in turn increase the revenues of other businesses, who in turn undertake return-seeking capital investment choices based upon expectations of continued growth in revenue.

Fifth, in our model there is no need to invoke a ‘normal’ rate of return on costs, since all real returns are driven by investment and output decisions in markets. Rates of return emerge from the market, rather than being fed into the market and emerging from some deep group psychology.

Sixth, the existence of a firm relies on both economies of scale and uncertainty – both of which must feature in our model. This shouldn’t be a surprise, since some rather hard-hitting economists have also made this point. Here’s Ronald Coase – “It seems improbable that a firm would emerge without the existence of uncertainty.” And not forgetting Frank Knight – “Its [the firm’s] existence in the world is a direct result of the fact of uncertainty”. We simply add that economies of scale are also necessary, since output would be infinitesimally small for any firm if that wasn’t the case.

Lastly, we need not invoke any special notions of short, medium or long run to understand markets. At all points in time firms are investing in new capital – it is a continuous process in the macro economy, even if at a firm level these lumpy capital investments are undertaken intermittently.

Phew.

We never expected that the small changes we made to ‘what firms do’ in a model would capture so many features of reality that had so far been treated in an ad hoc manner.

One important question concerns the value in this new theory. What can it tell us that existing theory cannot? I’ve thought about this a lot, and the answer is ‘a great deal’. It may take a number of posts to cover the important ones, such as; regulation of private monopolists, analysis of competition and market structures, the dynamics of market power and innovation, the ability to define economic rent broadly, the impact of regulations on competitiveness, competition via market share, and more. But let me just give you an example that I think is extremely important.

Housing supply.

The usual approach is to suggest that rising home and land prices have some connection to town planning regulations that determine location and density limits for new housing. If prices are rising, then according to our mainstream theory there must be a regulatory or physical constraint on the ability to shift the supply curve.

But the theory of return-seeking firm suggests that for many land owners the optimal choice is to withhold their land from development. Because there is an ability to delay investment, deferring capital improvement maintains the option value to develop at a later date to a much higher density. It may currently seem optimal to develop a 3 storey apartment building, but if I delay investing, I might be able to develop a 10 storey building in five years time and increase my return on the land.

In fact land development is a core example in real options theory.

If a government wanted to intervene in this market to increase housing stock compared to the status quo under existing regulations, our theory of return-seeking firms suggests that any policy that reduces the rate of return of the land owner when they delay will be effective at bringing housing investment forward in time. One idea is to announce a future restriction on development density, or implement a land value tax, which will reduce the potential rate of return from delaying investment.

Again, the working paper is here for those who wish to review our approach. I appreciate all responses and criticisms. Please share this article. Tips, suggestions, comments and requests to rumplestatskin@gmail.com + follow me on Twitter @rumplestatskin