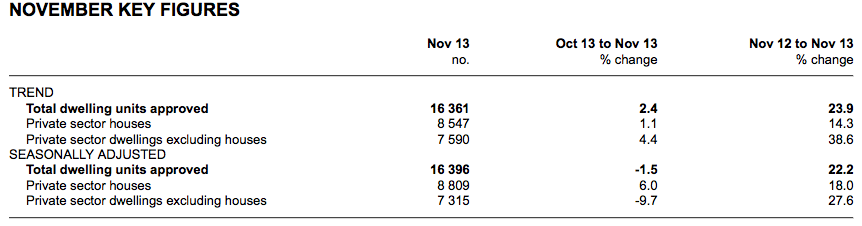

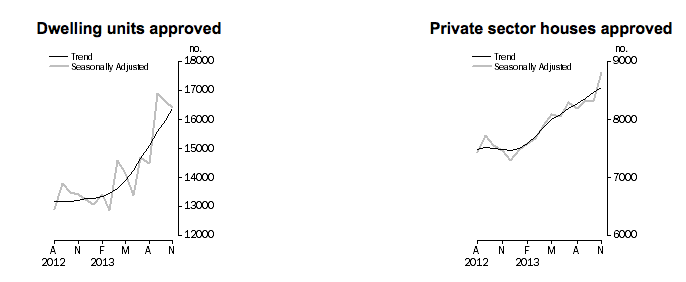

TOTAL DWELLING UNITS

- The trend estimate for total dwellings approved rose 2.4% in November and has risen for 13 months.

- The seasonally adjusted estimate for total dwellings approved fell 1.5% in November and has fallen for two months.

PRIVATE SECTOR HOUSES

- The trend estimate for private sector houses approved rose 1.1% in November and has risen for 11 months.

- The seasonally adjusted estimate for private sector houses rose 6.0% in November following a fall of 0.2% in the previous month.

PRIVATE SECTOR DWELLINGS EXCLUDING HOUSES

- The trend estimate for private sector dwellings excluding houses rose 4.4% in November and has risen for eight months.

- The seasonally adjusted estimate for private sector dwellings excluding houses fell 9.7% in November and has fallen for two months.

VALUE OF BUILDING APPROVED

- The trend estimate of the value of total building approved rose 2.3% in November and has risen for 22 months. The value of residential building rose 2.6% and has risen for nine months. The value of non-residential building rose 1.9% and has risen for three months.

- The seasonally adjusted estimate of the value of total building approved fell 3.2% in November after rising for four months. The value of residential building fell 1.9% after rising for five months. The value of non-residential building fell 5.3% following a rise of 20.1% in the previous month.

Westpac take on the data

The number of dwelling approvals in November were broadly in line with the market consensus, falling 1.5% following a 1.6% fall in October. We had been expecting a more material pullback in the month, circa –4.0%. Our forecast was built upon an expectation of a partial reversal of the mid-2013 strength in multiples. In the event, we did see a 9.7% decline in the number of multiples approvals in November, but an unexpected (and relatively unusual) 6.0% rise in the number of house approvals largely offset this weakness. The strength in private sector house approvals in November was relatively broadbased, with monthly gains of almost 15% seen in SA and NSW and a circa 8% rise in Vic. Taking a longer term perspective, the mid-2013 surge in multiples approvals and modest subsequent pullback has left the level of multiples approvals 27.6% higher than a year ago. Private sector house approvals are now also up a robust 18.0%yr. Growth in alterations and additions remains much more muted, with the value of approvals up 6.1%yr following a 6.7% gain in November.

Advertisement

Advertisement