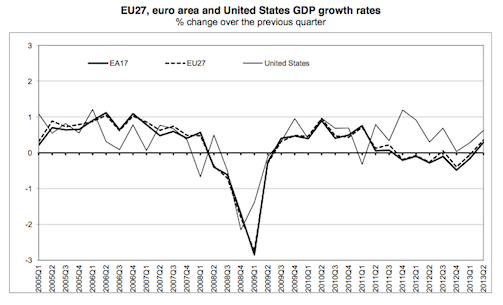

Overnight Eurostat released its second estimate for Q2 GDP for the Eurozone which restated that the region finally showed some growth in Q2:

GDP rose by 0.3% in the euro area1 (EA17) and by 0.4% in the EU271 during the second quarter of 2013, compared with the previous quarter, according to second estimates2 published by Eurostat, the statistical office of the European Union. In the first quarter of 2013, growth rates were -0.2% and -0.1% respectively.

Compared with the same quarter of the previous year, seasonally adjusted GDP fell by 0.5% in the euro area and remained stable in the EU27 in the second quarter of 2013, after -1.0% and -0.7% respectively in the previous quarter.

During the second quarter of 2013, GDP in the United States grew by 0.6% compared with the previous quarter (after +0.3% in the first quarter of 2013). Compared with the same quarter of the previous year, GDP rose by 1.6% (after +1.3% in the previous quarter).

….

Among Member States for which data are available for the second quarter of 2013, Portugal (+1.1%) recorded the highest growth compared with the previous quarter, followed by Germany, Lithuania, Finland and the United Kingdom (all +0.7%). Cyprus (-1.4%), Slovenia (-0.3%), Italy and the Netherlands (both -0.2%) registered the largest decreases.

As noted by Reuters the two major components for the uplift were exports along with government sector spending:

Stronger-than-expected growth from Germany to Portugal helped the bloc’s economy expand 0.3 percent in the April-to-June period, the European Union’s statistics office Eurostat said on Wednesday in its first breakdown of the data.

Exports to the rest of the world rose sharply in the quarter after six months of falling sales, while government spending made its first positive contribution to the economy since late 2009 when Greece plunged the euro zone into its debt crisis.

…

Behind Germany’s strong growth of 0.7 percent in the second quarter, Eurostat’s breakdown highlighted the softening of the austerity policies that many economists blame for worsening the euro zone’s 1-1/2 year-long recession. That was accompanied by the first quarterly rise in household spending since late 2011.

Portugal’s economy grew 1.1 percent, while Spain’s contraction was just 0.1 percent, offering hope that southern Europe will be able to end a social crisis highlighted by popular unrest and record youth joblessness.

Advertisement

However, there is still some caution in reading these numbers, especially from Portugal, whose own government said the export figures may not be as good as they appear:

But sales of refined petroleum products—which are volatile because of fluctuating oil prices—accounted for half the rise in exports. And because the Easter slowdown came early this year, at the end of March, exports in the second quarter got a seasonal boost, the agency said.

Portugal’s government and the European Union urged caution in interpreting the surprisingly robust quarter-on-quarter GDP growth, the fastest of any EU country that reported Wednesday.

What is also of note, outside the export figures, is the uplift in government sector spending. This follows on from the obvious change in policy position that I have noted over the course of this year. For nations, such as Portugal, this began in Q1:

Advertisement

Portugal’s lenders eased its budget goals on Friday and gave it more time to make unpopular spending cuts, acknowledging the country’s compliance with its bailout program will not prevent its economy from slumping further.

European Union finance ministers Friday confirmed that Ireland and Portugal will be given more time to repay some of their bailout loans.

Finance ministers from all 27 EU governments said at a meeting in Luxembourg they will allow a seven-year extension on the average maturities of loans made to the two countries from a bailout fund that was backed by the EU budget.

The move, which was already agreed in April at an summit in Dublin, is part of an effort to help the two countries wean themselves off bailout money and regain full access to capital markets.

Advertisement

Besides France and Spain, the Commission is also granting the Netherlands, Poland, Portugal and Slovenia more time to bring their deficits below the EU ceiling of 3 percent of annual economic output. That means they will be allowed to stretch out spending cuts over a longer time as they try to fight record unemployment and recession.

The Netherlands and Portugal are now granted one additional year, whereas France, Spain, Poland and Slovenia are granted two additional years each.

This is, however, is only half of the policy change story. What we have also seen is a slow, yet somewhat domestically concealed, change in German policy on wage inflation which I suspect is also contributing to the upside data:

Advertisement

And this is something that continued, at pace , into 2013:

German wages rose at their fastest pace in almost four years at the start of 2013 and euro zone exports jumped in April, giving the bloc a basis for a recovery from its long recession.

Nominal hourly labor costs rose 3.9 percent in Germany in the first quarter, the EU’s statistics office Eurostat said on Monday, faster than the overall euro zone rate of 1.6 percent. It was Germany’s biggest jump since the first three months of 2009.

Higher wages in Europe’s largest economy should mean German shoppers have more cash to splash out on Spanish holidays, Italian cars and Portuguese wine, potentially helping depressed southern Europe out of its downturn.

So, once again, the big question for me is what happens post-German election. Will be see a continuation of the relaxing of policy and therefore a continuation of growth, or a return to the pre-2013 hard-line position, and a renewed slump. We’ll know in 3 weeks.