US bond yields finally found buyers in US trade, although this can largely be attributed to a flight to quality. The perversity of the situation is that the move higher in developed market yields of late has been a key reason for the massive re-allocation of funds into developed markets from emerging markets (EM) funds and now. A viscous circle in some ways.

Still, for those who have been following the EM story closely, the issues at hand are not new and many know that India and Indonesia need external capital to fund their current account deficits. The new issue that is dividing traders though is whether liquidations start to impact nations such as Singapore and Korea, countries that don’t have the same excessive levels of private sector credit and therefore don’t display the same credit bubble properties that other more leveraged nations exude. This is a story yet to play out; however it is one that is firmly in the markets’ crosshairs now and could even be the biggest event risk for traders into Q3, Q4 and into 2014, especially with more and more comparisons between what we are seeing now and the 1997 Asian crisis.

In Asian trade today USD/MYR (Malaysian ringgit) has pushed slightly higher, while USD/IDR (Indonesian rupiah) has stolen the show briefly pushing above 11,000 and rallying a lazy 2.5%. Reports Indonesia’s biggest pension fund is increasing its purchases of Indonesian stocks has probably stopped the Jakarta Composite falling further into bear market territory, with the index flat on the day. India is seeing better days with the Sensex up 1%, after news that the Indian Central Bank is buying long-dated bonds, with yields falling 58 basis points on the day. Yesterday’s high of 9.47% on the Indian ten-year was around thirty basis points lower than Greece’s ten-year bond, despite having around 5% growth; although this has more than halved from 2010.

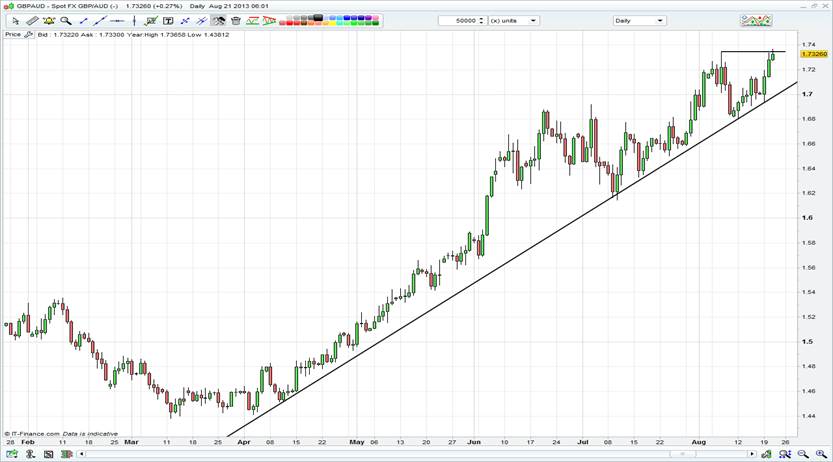

In terms of the AUD, the flows we’ve been seeing over the last couple of days have been very much two-way, however the Aussie seems to have become the market’s favourite G10 short again, for those looking to express concern on emerging market risk. Yesterday’s falls were testament to that, and price action now in GBP/AUD and EUR/AUD is once again quite one-sided and looking to resume its recent uptrend. This therefore gives AUD even more leverage to Fed policy, because more hawkish language than the market is positioned from the Fed will see further stress on EM and therefore on the AUD. News that Japan has raised the severity of the latest Fukushima leak to level three has pushed AUD/USD down to a low of .9018.

On the subject of the Fukushima leak, a level three is considered a ‘serious’ incident by global standards, so this is very much a watch this space issue for markets now. USD/JPY hit a low of 97.11 on the back of this news, although this is more a correlation effect, with the Nikkei which fell 1.6% in a short space of time, after being up 0.5% in early trade. In theory you could make an argument that this incident will heighten the perception of increased US energy imports in the future and therefore a lower trade balance and over the longer term a stronger USD/JPY.

The ASX found good buying off the low, with the index hitting 5069 in early trade and pushing up through lunch to close at 5100 (+0.4%).22 corporates have reported today, so it’s been a busy day for equity traders, with plenty of single-name volatility. We’ve seen nearly 40% of the ASX 200 report earnings and 56% have beaten the street’s consensus on EPS, while 42% have beaten on top-line. From what we’ve seen so far earnings have fallen nearly 10% against the previous corresponding period, although we expect this figure to rise through the remaining earnings season. Buying in the banks has kept the market steady, with BHP taking out the points given its 8.4% weight on the market. We like to stay ‘neutral ‘on this name from a fundamental point of view given the big macro issues playing out and underwhelming earnings, although lower costs and 2014 capex guidance are supportive. The $2.6 billion committed to the Jansen Potash project is interesting, and while this is being seen as negative at the margin, the longer-term diversification this offers should be positive. This is a long-term project however, and this is a short-sighted market and investors want to be leveraged to what’s working here and now.

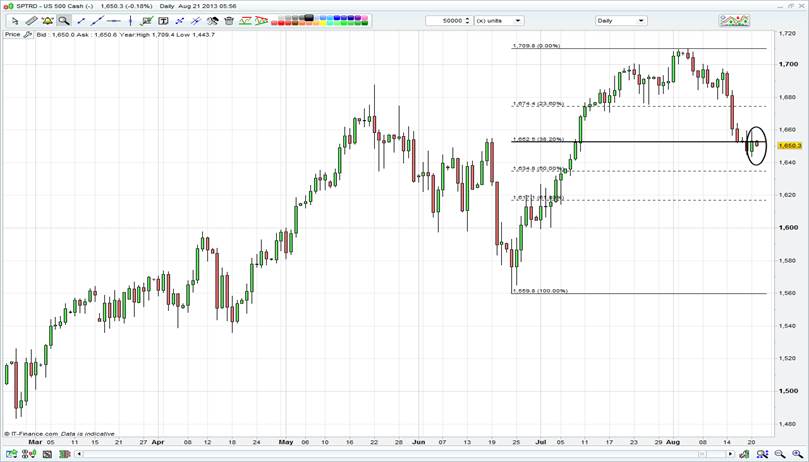

Europe looks to be getting off to a weaker start and could very well be in a holding pattern until we get into the FOMC minutes in the latter part of the session. The failure to close back above the 38.2% retracement of the 1560 to 1709 move at 1562.62 (see below) on the S&P 500 (the S&P 500 closed at 1652.35) is a bit of a concern for the bulls and shows momentum is starting to favour further downside, although we haven’t been given a strong sell signal yet. Today’s Fed minutes will be the key release then for today and will expand from the July FOMC statement, which was taken to be more dovish than expected at the time by the market. Whether we actually get any new information is what traders will be scouring the narrative for, and the areas of most interest involve heightened language around forward guidance and further concern around the risks around higher mortgage rates. We stick by our call that the September meeting will herald a clear sign of tapering, although given rhetoric from recent Fed officials this event could be fully announced in the October meeting (which could have an additional press conference) and likely lowered by a token amount to both US treasuries and mortgage-backed securities. This in turn could be tempered by a change in the current forward guidance instigated by Charles Evans.