As I noted yesterday, the chatter about Europe changing course on ‘austerity’ is growing, although as I stated although this appears to be positive step forward, I really think we need to wait until after September to get a handle on exactly what that means. The outcome of the German election is very likely to have a large effect on the policy shifts from Berlin and Brussels and, although we are seeing signs that the hard-liners are loosening their grip on policy, we’ve seen significant back-flips in the past.

In the meantime, the current policy framework within the region continues to slow economic output and retrench private sector investment. Overnight the OECD warned that the Eurozone is once again slowing more “than expected”:

The OECD has again cut its growth forecasts for the eurozone and called on the European Central Bank to consider doing more to boost growth.

The organisation says the eurozone will shrink by 0.6% this year, widening the gap between it and faster-growing economies such as the US and Japan.

The UK forecast was revised down to 0.8% growth this year and 1.5% in 2014. Meanwhile, the European Commission has given France two more years to complete its austerity programme.

France fell back into recession in the first three months of the year. Spain, Poland, Portugal, the Netherlands and Slovenia have also been given more time to complete fiscal tightening.

The move suggests a shift away from a focus on austerity in Europe.

Of note the OECD cuts Italy’s 2013 forecast again to -1.8% from -1.5%, France to -0.3% from 0.3% and the EZ as a whole to -0.6% from -0.1%, which appears to have put to bed the idea, being pushed by Mario Draghi and other Eurocrats, that 2013 is the year of recovery.

Overnight we also had some data on deposits in periphery banking systems which wasn’t exactly good news:

Consumer and company withdrawal of deposits from Cypriot banks accelerated in April, where big account holders in the two largest lenders were forced to take a hit as part of an international bailout.

Private-sector deposits fell by 7.3 percent to 41.322 billion euros after a nearly 4 percent fall in March, European Central Bank data showed on Wednesday.

…Greece recorded a 1.6 percent decrease in private sector deposits, falling to 170.0 billion euros, and Spain saw similar development with a 1.5 percent fall. Deposits in Italian and Portuguese banks fell less than 1 percent each.

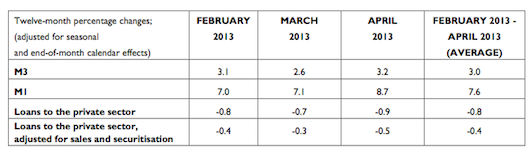

In line with that data, the ECB was also out with its monthly developments report and, as expected, private sector credit growth remains in the negatives:

Turning to the main counterparts of M3 on the asset side of the consolidated balance sheet of Monetary

Financial Institutions (MFIs), the annual growth rate of total credit granted to euro area residents stood at -0.1% in April 2013, compared with 0.0% in the previous month. The annual growth rate of credit extended to general government stood at 3.5% in April, unchanged from the previous month, while the annual growth rate of credit extended to the private sector stood at -0.9% in April, unchanged from the previous month. Among the components of credit to the private sector, the annual growth rate of loans was more negative at -0.9% in April, from -0.7% in the previous month (adjusted for loan sales and securitisation,the rate was more negative at -0.5%, from -0.3% in the previous month).The annual growth rate of loans to households stood at 0.4% in April, unchanged from the previous month (adjusted for loan sales and securitisation, the rate stood at 0.3%, unchanged from the previous month).

The annual growth rate of lending for house purchase, the most important component of household loans, stood at 1.2% in April, compared with 1.3% in the previous month. The annual growth rate of loans to non-financial corporations was more negative at -3.0% in April, from -2.4% in the previous month (adjusted for loan sales and securitisation, the rate was more negative at -1.9% in April, from -1.3% in the previous month).

Finally, the annual growth rate of loans to non-monetary financial intermediaries (excluding insurance corporations and pension funds) stood at 0.6% in April, unchanged from the previous month.

So some hope for the future ? Maybe, but the current situation is still very dour. Full report from the ECB below.

ECB Monetary Developments April 2013