Another round of PMI data from the Eurozone overnight and once again, even though there are some minor improvements, the data is still poor.

PMI signals ongoing recession in second quarter, though downturn eases in May

- Flash Eurozone PMI Composite Output Index(1) at 47.7 (46.9 in April). Three-month high.

- Flash Eurozone Services PMI Activity Index(2) at 47.5 (47.0 in April). Three-month high.

- Flash Eurozone Manufacturing PMI(3) at 47.8 (46.7 in April). Three-month high.

- Flash Eurozone Manufacturing PMI Output Index(4) at 48.2 (46.5 in April). Four-month high

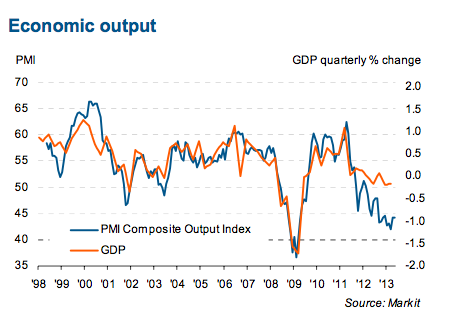

The Markit Eurozone PMI Composite Output Index rose to a three-month high in May, but remained deep in contraction territory. According to the flash estimate, based on approximately 85% of total replies, the Eurozone PMI rose from 46.9 in April to 47.7 in May, signalling an easing in the rate of contraction for the second consecutive month. However, the latest reading is merely in line with the average seen during the first quarter, a period when the region’s economy contracted 0.2%.

The ongoing downturn signalled by the PMI therefore suggests that the euro area’s recession will have dragged on into a seventh successive quarter in the second quarter of 2013. The downturn remained broad based, but both main sectors saw an easing in the rate of decline.

Manufacturing output fell at the slowest rate since January, while service sector activity declined at the weakest pace since February.

Although moderating, the downturn in business activity looks likely to persist into June, due to an ongoing decline in demand for goods and services across the region. New business fell sharply again, down for the twenty-second successive month with the rate of unchanged on that seen in April. Although manufacturers reported the smallest drop in new orders for three months, service sector companies saw the rate of decline accelerate again, having reported an easing in April.

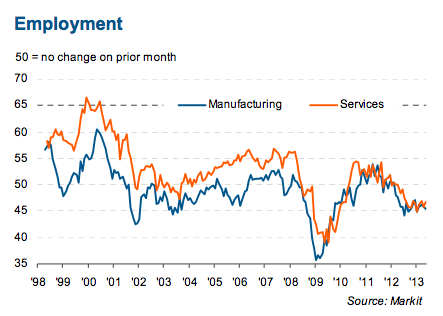

And on employment it’s much the same:

Employment fell for the seventeenth consecutive month, with the rate of job losses rising to the highest since February. Increasing numbers of firms sought to reduce capacity in line with deteriorating order books. Backlogs of work have now fallen continually for almost two years, dropping in May at a similar steep rate as seen throughout the year so far.

Employment fell in both manufacturing and services, with hiring even being scaled back in Germany, where headcounts fell for the first time since January. The rate of job cutting eased in France but nevertheless remained severe. The rate of job losses seen across the rest of the euro area eased to an 11-month low.

As Markit’s chief economist notes, the latest monetary policy action from the ECB has done little to nothing to help:

The eurozone’s second recession in five years looks set to drag on into a seventh successive quarter. Although the Eurozone PMI rose for a second successive month in May, the survey remains firmly in contraction territory and indicates that the economy is likely to contract in the second quarter at a similar rate to the 0.2% decline seen in the first three months of the year.

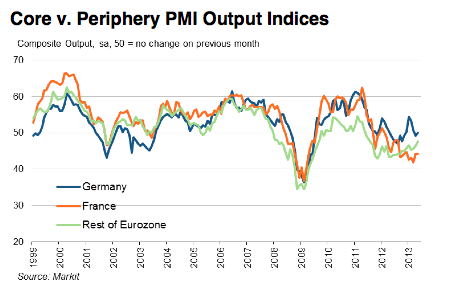

Weakness remains broad-based, with Germany stagnating, France contracting steeply and the rest of the region also clearly entrenched in an ongoing downturn of worrying severity, although some signs of the recession easing in the periphery were seen in May.

Signs of deflationary pressures were also evident, highlighting just how weak demand is at the moment. Both manufacturers and service providers cut their prices in the vain hope of stimulating sales.

The ECB’s quarter-point cut in interest rates seems to have done little to inspire confidence that the economy will start to pick up again. In fact, expectations about the year ahead deteriorated again in the service sector, suggesting recovery remains a long way off still and that policymakers need to do more to stem the downturn and revive growth.

That assessment is most definitely at odds with the latest musings from the Bundesbank who, like Mario Draghi and many other Eurocrats before them, have been forecasting a revival later this year:

Germany’s central bank expects the country’s economy to improve “markedly” in the second quarter – a development that could boost the wider euro zone as it struggles to get out of recession.

The Bundesbank said Tuesday that Europe’s largest economy should expand more robustly after a weak first three months of the year. Germany grew only 0.1 per cent in the first quarter in part because cold weather delayed the construction season.

In its monthly report, it said that construction activity will catch up. It also cited “reason to hope” that companies will start investing in machinery and equipment to meet increased demand for goods – a key stage in any recovery. Industrial orders unexpectedly rose in March by 2.2 per cent, instead of declining as analysts had expected.

So far, the report said, corporations continue to hold back on new investment, primarily because of weak demand for products – even though conditions for financing new investment are “exceptionally favourable.” The European Central Bank cut its key interest rate to a record low of 0.5 per cent on May 2 and bank lending rates remain low.

I’m personally struggling to see where this recovery is going to come from. Yesterday’s China PMI data suggests there is nothing to look forward to in global tradables and it’s obvious from recent data that the two big EZ economies outside of German, France and Italy, are in trouble. In fact the French data remains poor (although again, this should come as no surprise ):

The downturn in French private sector output continued in May. Unmoved from April’s reading, the Markit Flash France Composite Output Index, based on around 85% of normal monthly survey replies, posted 44.3. Although remaining above the levels registered in Q1, the latest reading was indicative of a marked rate of contraction in overall activity.

The decline was broad-based across the manufacturing and service sectors, with equally sharp falls signalled in each case. The latest drop in manufacturing production was fractionally weaker than in April, and the slowest in nine months, whereas service providers noted an unchanged rate of contraction in activity.

The northern European recession and the southern depression continue apace and, from this data at least, still have quite a while to run.

Markit Economics EZ PMI May 2013