US investors continue to push up stocks, with traders looking to gain exposure to more cyclically-focused areas of the market, and not defensives. You can certainly understand this, with Goldman Sachs suggesting that cyclicals are more undervalued relative to defensives than at any other time in the past fifteen years. Perhaps this will be a theme that develops, with traders shifting first and the investment community someway after.

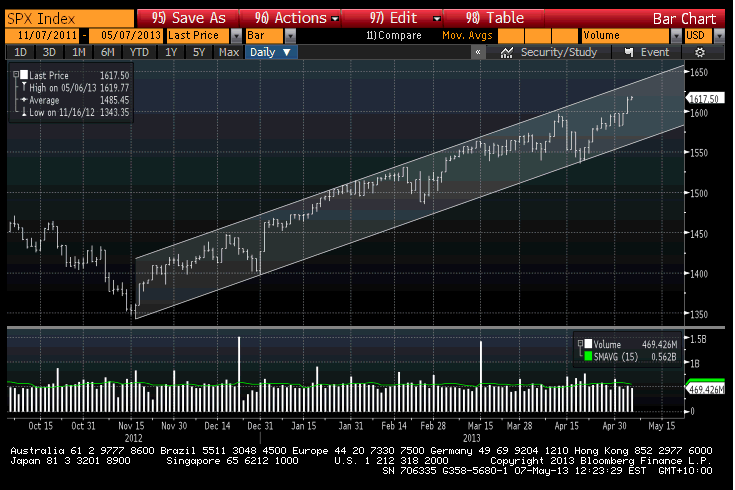

We still feel the US and Japan are the markets to be leveraged to, and in the case of the US, while fundamental traders will point to downside risk to the $109 consensus for 2013 full-year earnings, a 14.8x multiple is not actually overly pricey anyhow. On the other hand, the technicals still look good and you can’t go past the clear ascending channel (as seen below), with 1638 the top and thus near-term resistance. We will keep an eye on the bond market as well given the growing chorus of investment heavyweights who are either calling a bear market in treasuries, or talking about the lack of investment-case right now. Either way, the US ten-year treasury looks very interesting and could signal that a move higher is on the cards, although that would mean we would need to see inflation expectations pick up. Like Warren Buffet said, the time will come for much higher yields, but as with anything in trading markets, it’s a question of timing. Equity bulls will be hoping the great rotation trade will then start in earnest.

Asia has once again seen different paths being taken, and while the ASX 200 has attracted modest sellers, the Nikkei came back on line with a bang. The Japanese equity market printed a new high of 14,157 (+3.4%), taking out the April 26 high of 13,983, and importantly the 61.8% retracement of the 2007 to 2008 sell-off at 13,979. The next clear resistance is not seen now until 14601 (June 2008 high). USD/JPY hasn’t really helped equity investors though, with traders keeping an eye on any signs of activity from the different Japan life insurance players, although in the end, reports of heavy selling from exporters and a mix of stops pushed the pair down to 98.83, although has since rebounded. Comments from finance minister Taro Aso that it will take a few months for BoJ easing to take effect are not helping either. As we said yesterday, we need to see JGB (Japan government bonds) yields pushing back towards 50 basis points to create the real upside in USD/JPY, and subsequently the Nikkei in the short-term.

As mentioned, the ASX 200 was in a holding pattern ahead of the RBA decision, although predictably came alive on the back of the 25 basis-point cut. Prior to that though, we had the March trade balance, and with the ABS already detailing a 1% decline recently, we knew that even modest growth in exports would create a surplus. This ended up coming to fruition, with exports gaining 1%, thus a surplus of $307 million was seen (the first since 2011), although the AUD had its eyes on the RBA meeting.

It’s hard to remember a meeting that has divided a market so intensely. Cutting rates to historic lows was certainly gaining more weight in the market, and the bank decided to use its power to support demand given the inflation outlook could definitely allow it. While some (including ourselves) had expected rates to be on hold, albeit with a clear signal to ease in June, it seems the RBA has looked to get ahead of the curve and not wait for the CAPEX figures on May 30. The key line though is in the last paragraph and the narative ‘at today’s meeting the Board decided to use some of that scope’; the emphasis falls on the word ‘some’, and thus not all. AUD/USD has predictably broken key support at 1.0221 and is eyeing the March 4 low of 1.0115.

European markets won’t have taken too much sentiment from the Nikkei given the Japanese market was playing catch-up. US futures are flat and all eyes now fall on a European corporate space with HSBC, Societe Generale and Commerzbank reporting earnings, and all have big weightings on the corresponding markets; in the case of HSBC, 8%. The market is expecting net operating income of $18.8 billion, while pre-tax earnings should grow around 18% to $8.1 billion. On the data side, again Europe takes centre stage, with French industrial (expected to fall 0.3% in March) and manufacturing production, while German factory orders should also show weakness, with the market anticipating a 0.5% decline.

In our opinion, comments from Mario Draghi yesterday about potentially imposing negative rates were designed to clear up the confusion on Friday after Mr Nowotny’s comments. As things stand, the chance of negative deposit rates anytime soon are low, however upside should be capped, especially as we know the exchange did play a part in the recent cut to the refinancing rate.