In my previous post I introduced the idea that the neoclassical market model is built on the shaky foundation of profit maximisation. I introduced the theory of a return-seeking firm, whose aim is to find the highest returns, measured as profits per unit of cost, over the long run.

It is now time to expand the model from one firm in a market to many, to see just why a supply curve can have any slope, is unrelated to a cost curves, and simply arises from the competitive nature of a market.

In the theory of return-seeking firms prices are set as high as possible by every firm. This price is set with consideration of current and future competition, potential to capture market share, and the price-sensitivity of the firm’s customers.

There is no supply curve as such. If we consider the short-run, just like the neoclassical model, firms react to changes in demand based on their expectations about 1) the persistence of a demand shock, 2) their competitiveness.

Under normal conditions where demand increases in line with expectations, mark-up pricing set at a level to discourage competitor entry can continue to be used. This is just one of the many common pricing options available to a firm (a discussion for a later post).

However such a pricing strategy might not make sense during a short-run demand shock.

By definition, a short-run demand shock occurs over a period of time in which no new competitor can enter the market. Nor can your current competitors expand their capital to shift their own cost curves. Essentially then, the short run is defined as period where firms have a quasi-monopoly because there are perfect barriers to entry.

The essential question then becomes, how do the firms in the market compete under temporary monopoly conditions?

Some might maintain their low-markups, or even reduce them in order to gain market share if they expect their competitors to raise prices. Some might raise prices in certain areas where they have a stronger monopoly on their location than others. In fact, anything goes, and the price under a demand shock can move along any slope that is higher than the cheapest firm’s cost curve (meaning that the most it can slope down is depends on the shape of the cost curve, but it can slope up to near vertical).

For example, if demand for oil tankers increased over a short period, ship builders would have years to increase their mark-ups and returns before a competitor could become established. However, they may choose not to set prices that increase their returns substantially in the short-run because lower prices may decrease the attractiveness for a new competitor, or might win market share from an existing competitor. No use making a high return now, but being forced to accept very low returns in the future when new firms enter the market.

The price setting during a short term demand shock is not the result of costs faced by firms, but of market power. This is a critically important difference between this new theory and the neoclassical theory of markets, which is particularly relevant in terms of policy making for regulators looking to encourage competition while constraining monopoly behaviour.

Consider then the weekly petrol price cycle. This is a case of temporary monopoly power of petrol stations. Since people have similar weekly driving patterns, and fuel purchases typically coincide with other activities, each location has a degree of monopoly power. And it is optimal to independently change prices during the weekly demand cycle. Recent Queensland research shows that those petrol stations with closely located competitors have more stable prices. That is what the type of reduced ‘seasonal’ monopoly power the model predicts.

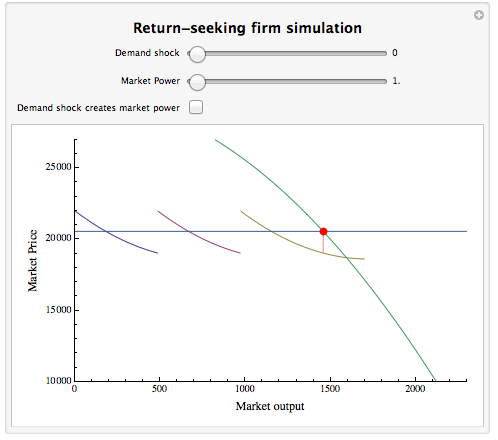

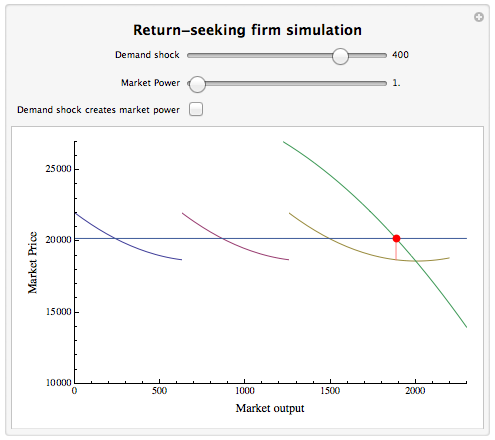

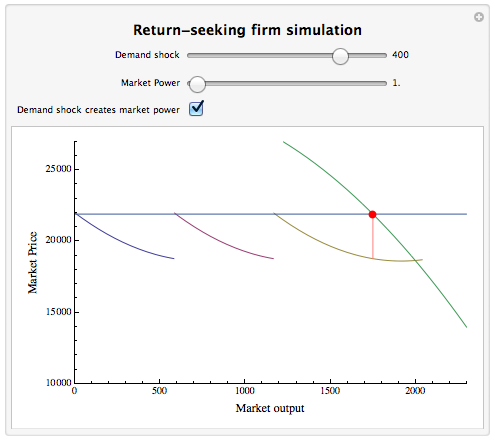

A small interactive model of this effect is shown below for the case of three firms in a market.[1] The rate of return earned at the starting position is proportional to the market power/competitiveness of the industry (which can be adjusted with the slider). The checkbox allows market power to be related to demand shocks to demonstrate the case that even in apparently competitive markets unexpected demand shocks might themselves create temporary market power and generate what looks like an upwards sloping supply curve.

In the Part III of the series I will look at the what the new theory says about the way firms really compete.

fn. [1] The interactive version requires Mathematica CDF and the plugin for your browser and is located here. Alternatively the Mathematica Notebook is available here