US markets continue to push higher and today could be the day the S&P 500 prints a new closing high, which given it’s a mere point away, is very much a rounding issue. The fact that the Cypriot dramas have been widely overlooked for domestic data shows US investors are in a positive place, and a move through the intra-day high of 1576 can’t be too far away either.

If the market is going to close above 1565 today, then US pending home sales will need to be strong, while Cleveland Fed President Sandra Pianalto can’t say anything that could be construed as overall hawkish. Recall in February she talked about tapering back on asset purchases before year-end if the economy continued to gather momentum. The Cleveland President also spoke out about the risks both on a credit and interest-rate basis if the Fed gets its timing wrong. Currently she is not a voting member, although will be in 2014, but Sandra Pianalto’s comments will still be of interest, as will Boston Fed President Eric Rosengren (who is a voting member this year and speaks earlier) who will probably give a more dovish bias and maintain the status-quo.

Europe remains transfixed on Cyprus, and while the market has moved on from the country itself, the focus is now more firmly on broader implications, especially in wake of recent comments and headlines in the last 36 hours. First we had the Dutch finance minister and Eurogroup chair Jeroen Dijsselbloem providing insight, and last night we heard an EU lawmaker suggesting the European parliament could push for depositors with €100,000 or above to face a bail-in under new bank resolution law. Either way you look at it, the banking industry in Europe is going to have to change; any bank with a heavy reliance on public sector support will have to downsize and restructure. The EU has spoken out that it may help out sovereigns that have issues raising funds through the debt markets (Greece for example). However, banks will not be funded by sovereigns indirectly through the Troika any longer and depositors will be the first line of offence. Say goodbye to the ESM (European Stability Mechanism) and potentially even a banking union. The other key issue is the use of the ECB in the whole process. As the dust settles, it is clear that the ECB has played, and will continue to play an ever more political role in negotiations. In this case, while the EU maintained a mantra of ‘we will give you €10 billion as long as you can provide €5 billion in commitments – however you want to do it’, it was the ECB who ultimately put the gun to the Cypriots’ head and said ‘get it done now’!

EUR/AUD looks a good way to play the concerns and continues to make lower lows with the pair hitting 1.2235 before finding modest short-covering to close at 1.2264. Importantly this was below the December low of 1.2272, and a move now to 1.2160 can’t be ruled out. AUD/USD continues its grind north, reaching a high of 1.0497 in US trade. The pair looks strong and while there isn’t a huge amount of volatility seen here, this will benefit traders, especially if the VIX continues to move lower. Traders are buying AUD given it has the highest ‘real’ yield in the G10 complex when the interest rate is adjusted for inflation, and when volatility is low this will find buyers. Remember hedge funds and other large leveraged plays hate shorting AUD/USD, as it’s very expensive to do so, and in the current environment they will play AUD from the long side. We feel a move to the January 10 high of 1.0599 can’t be ruled out given the current momentum, although we also believe long AUD/JPY also looks good. The latter seems like it wants to break the recent high of 99.97, where there is subsequently little resistance seen until the 2008 high of 104.50.

In the equity space, the ASX 200 has found good buying activity with the broader market putting on 0.9%. telco’s, healthcare and material names are putting in the points, while utilities lagged. We are pretty neutral on the Australian market at present both from a valuation and technical perceptive, and unless we see the S&P 500 and Nikkei move convincingly higher, we feel the market looks pretty comfortable around the 5000 mark. A move above the March 25 high of 5023 is needed to see the recent high of 5163 come into play.

Japan and China are both firmer, although it has to be said that the Nikkei would be even more so if it wasn’t for the fact that 88 points coming out of the index as 87% of the index went ex-dividend today. The talk in the Chinese market was around a descent decline in banks’ bad-loan ratios. There has been a reasonable rally in bank shares as you’d imagine, and renewed confidence that the asset quality has gotten through the worst. The fact that the Shanghai Composite is trading on 9.4 times 12 month earnings puts the index on a 40% discount to its seven-year average.

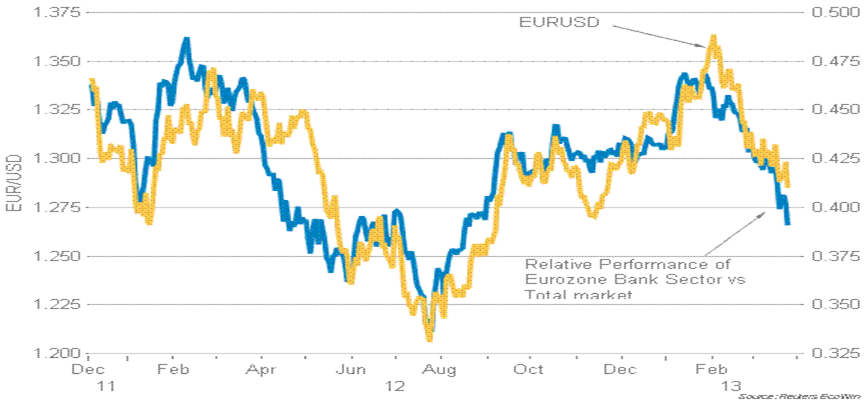

FTSE and EuroStoxx futures are basically unchanged from the close of the European/UK cash session, although S&P futures are up 0.4%, thus given the tepid moves in Asia our opening calls are modestly higher. Of course the banks are fully in focus and another day of weakness could have implications on other asset classes like EUR/USD, for example (given the correlation – see chart below). On the billing we have Q4 GDP in the UK, although it’s a revision and not expected to change. We also get consumer confidence for the eurozone and Germany, with retail sales in Italy and Spain. The Italian treasury will also try and tap the bond market for up to €4 billion in five-year bonds (previous average yield of 3.59%, bid/cover of 1.61x) and €3 billion in ten-year bonds (average yield of 4.83%, bid/cover 1.65x). With underlying yields currently softer, we will probably hear about lower borrowing costs, however it’s all about demand and any upside in the bid could help European assets.