We suggested on Friday that EUR/USD may initially spike on a Cypriot agreement, but this reversed course as traders looked at the finer details of the potential bailout. This has worked well with the EUR getting sold heavily across the G10 complex, although EUR/JPY experienced the most aggressive move.

Cyprus is a small country and granted it makes up less than 0.5% of eurozone GDP. However, the confidence that has been shaken is significant and the fact the Cypriots didn’t actually get a chance to vote is key and hence other European banks were smashed. It was then down to Dutch finance minister and head of the Eurogroup Jeroen Dijsselbloem to provide the fuel to the EUR rout. After being quoted as saying the bailout measures represented a ‘template’ for future banking issues, which in turn was the trigger for the moves down in risk assets, we subsequently saw a spokesman saying he didn’t actually make the comments after all. Unfortunately the market took no notice, and the contradictions continued as he later came out and said he had ‘no regrets’. As detailed, the fact that this ‘template’ can be applied to other banks without even a vote on the measures is key. It now appears that Cypriot banks will stay closed until Thursday, which was always going to be the case with the Bank of Cyprus given it will house all the ‘smaller’ deposit holders that have migrated over from wound-down Laiki bank, as well as €9 billion in ECB liquidity. Thursday therefore will be an interesting day (for anyone not holding deposits over €100,000 in one of these institutions); while there will be capital controls, the market will be keen to monitor outflows.

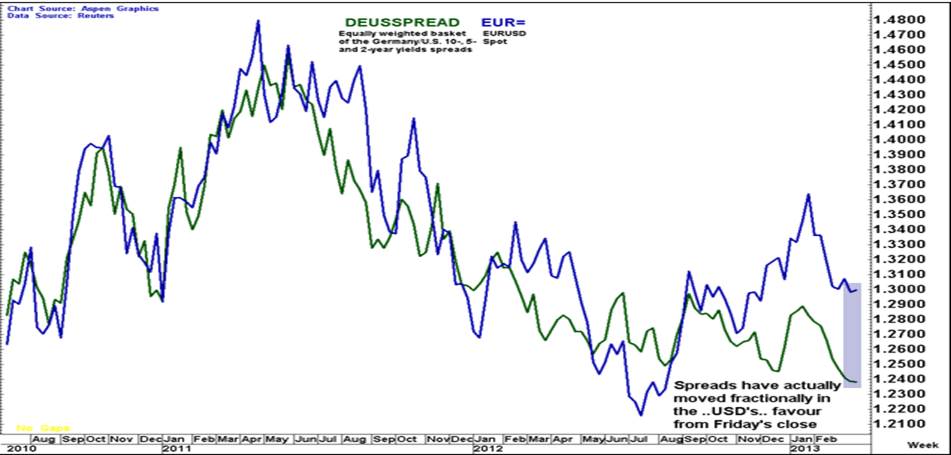

EUR/USD filled the gap from Monday’s open perfectly (as seen on the one hour chart) and printed a bearish outside day in the process. We feel traders could look to move stops down to 1.2950 (just above the 50.0% retracement of yesterday’s sell-off) and a move to the November low of 1.2662 can’t be ruled out over time. Comments from New York Fed President Bill Dudley that the Fed should alter the pace of asset-purchases if the trend in employment continues are very interesting, and have widely been talked about on the trading floors today. The consensus in the market is that November will be the date that the Fed tones down the pace of asset purchases from the current rate of $85 billion a month, and the New York President spoke about slowing the pace of buying – while certainly not a huge surprise, it was the first time the core of the Fed has commented publically about this. All in all it fits in nicely with our stronger USD view over the next couple of years, and with the ever-changing political landscape we feel EUR/USD could trade to 1.10 over time. Interestingly, a German bund/US treasury yield spread suggests current ‘fair value’ is closer to 1.24 at present.

With the S&P 500 closing down 0.3%, Asia has predictably struggled. The ASX 200 is lower by 0.7% with material names taking the brunt of the selling, and in the short term we will be watching last week’s low of 4927 where a break could potentially target 4846 (the 38.2% retracement of the November rally). We’ve heard a raft of bearish calls on iron ore in recent weeks, but now copper is getting a closer focus with hedge funds holding the highest level of short contracts since records began in 2006. The supply/demand equation is not too flash, with stockpiles in Shanghai and London the highest since 2003; add in New York stockpiles and this equates to five months’ worth of US demand. It’s interesting to see swaps traders in China are now holding a view of future policy tightening by the PBOC, the first time they have held this view since 2011. Clearly when USD/CNY is at a 19-year high you know that officials still feel inflation is key. Rio Tinto has now fallen 20% from its March high, thus technically the stock is in bear market territory; BHP is not far off having lost 16% of its value.

China has been the regions underperformer with the index down 1.8%, Japan on the other hand found sellers on the open, although when Haruhiko Kuroda started his lengthy three hour conference USD/JPY moved higher, and of course so did the equity market. As detailed in previous reports, we remain USD/JPY bulls over the medium term and think 100 is achievable, however price action is looking more and more shaky. The base-line of the cloud (now 93.79) was once again breached yesterday, as was the November uptrend at 94.00, although the pair closed above these points and we will continue to watch developments here, with a closing break suggesting a deeper correction could be in the cards. Clearly the market is now primed for next week’s BoJ meeting, and Mr Kuroda has certainly built expectations up ahead of that.

In Europe, again the focus of the market will be on banks and whether yesterday’s sell-off continues. Given the price action in some of the Asian resource stocks, it feels like this sector will struggle as well, although as things stand our opening calls are suggestive of a higher open. There isn’t a lot of data to drive out of Europe, so the market will look at the raft of data points in the US with durable goods, Richmond Fed manufacturing, the Case-Shiller house price index, consumer confidence and new home sales which will keep traders on their toes.

(Source Goldman Sachs research – Yield differential suggesting EUR/USD should be lower)