In this week’s spotlight, we take a look at the very well-known Australian surf wear company Billabong (Billabong Group, BBG). Gnarly.

The Business

Billabong (BBG) started out as a humble board shorts maker, with founder Gordon Merchant designing and stitching his wares in a Gold Coast kitchen in 1973. From those humble beginnings Billabong has grown into a globally recognised surfing brand, involved not only in clothing and apparel but also sponsorship of major board sports events and athletes. The Billabong Group now owns many surf, ski and skate-related clothing designers including Element, Kustom, Tigerlilly and Von Zipper.

In recent years BBG’s strategy has focused on acquiring retail chains to increase the group’s vertical integration. This decision was driven by third-party retailers squeezing BBG’s wholesale margins and limiting shelf space for BBGs products. In FY11, BBG acquired Surf, Dive in Ski and Rush Surf in Australia as well as RCVA and West49 in North America.

The Financials

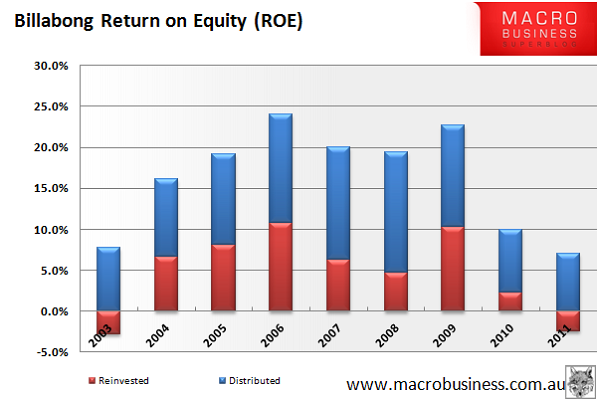

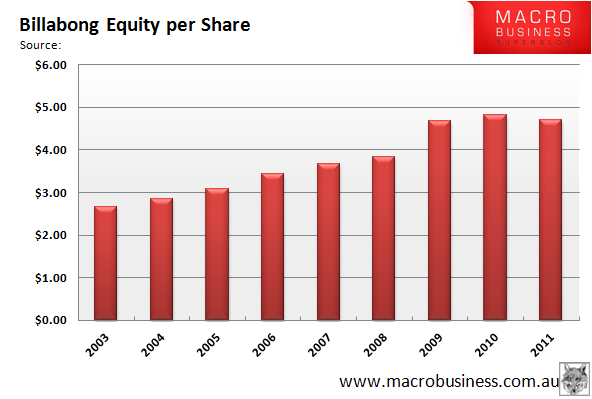

Billabongs return on equity (ROE) was a healthy 20% – 30% between 2005 and 2009. However, it has dropped dramatically after a large capital raising in 2009 combined with decreasing earnings. Equity per share stalled around $4.70 over the last few years.

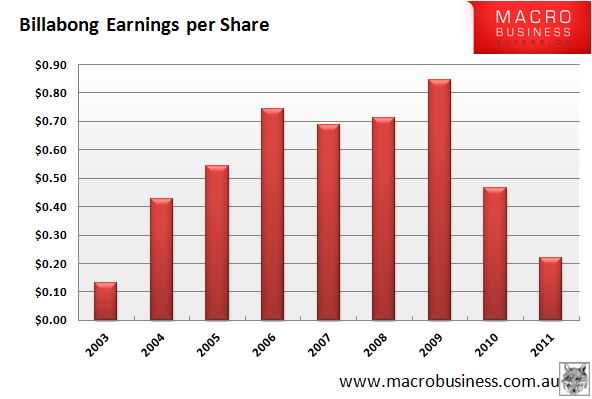

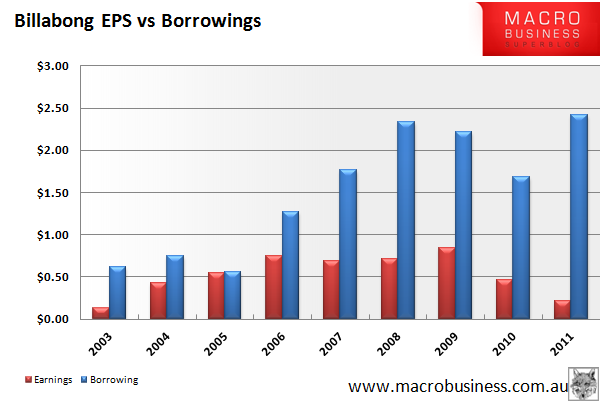

The earnings per share graph follows the ROE trend, with big drops from 2009 onwards.

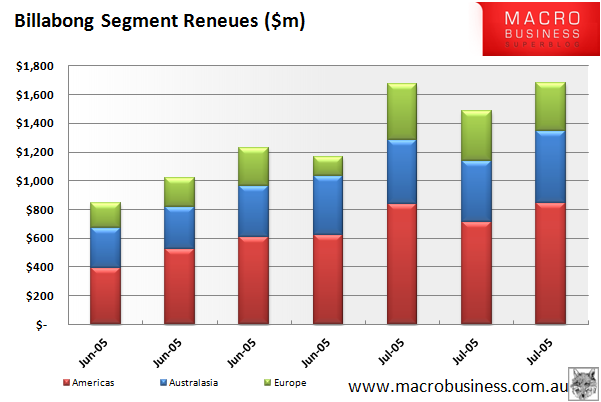

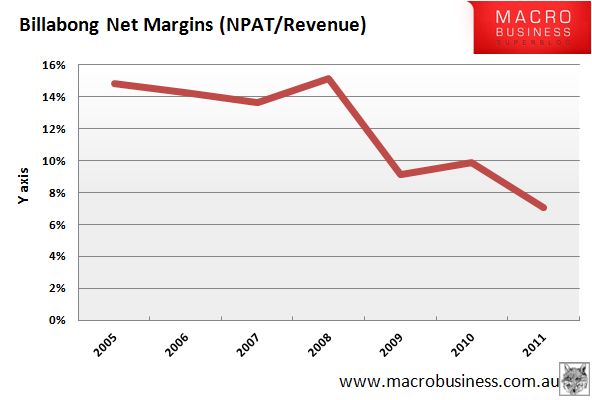

BBG claim the drop is due to a higher AUD and the costs of purchasing low-margin retail stores as part of the vertical integration strategy, which require inventory to be cleared before their own higher-margin products can roll out. There are some truths to these explanations, as the graphs below show BBGs revenue’s by segment and their net margins (NPAT divided by revenue).

About 70% of sales come from outside Australia, meaning the AUD has a big impact on revenues. BBG margins during the good times were also a fantastic 15% (just goes to show the power and financial rewards of branding). However those high margins mean their prices often sell at a large premium to similar clothing from the likes of Kmart or Big W. There is nothing more discretionary than a $90 for a pair of boardies or an $80 t-shirt with a surfing logo on it.

Whilst these issues have had an impact, the real underlying problems for BGG are high debt, poor capital management and a poor retail environment. The graph below, showing EPS vs borrowings per share, paints a grim picture. Debt levels have risen whilst earnings have dropped.

BBG also has very high levels of intangible assets, with their net tangible assets are actually negative. While high margins would indicate some of this is genuine brand value, EPS of only $0.22 against intangibles of $4.99 per share indicates they have paid too much for past acquisitions. To make things worse, a lot of the borrowings used to fund these acquisitions are in US dollars. So a while a drop in the AUD would assist earnings, it would also increase their debt load substantially in AUD.

In October 2007 RBS analysts warned BBG may be close to violating their debt covenants and should issue capital or sell assets to shore up their position. Either option would be disastrous as BBG’s share price is now well below their equity per share level, making any capital raising will be dilutive for existing shareholders. They also have $50 million in unrealised capital losses on the AUD value of their overseas assets – some of which would become very realised if they were forced to sell assets by their creditors.

To add insult to injury, the western consumer is now hibernating after the GFC and whilst the Euro debt debacle rolls on. BBG has overestimated sales recently in the expectation of a retail bounce back that hasn’t materialised. They even stated in their FY11 financial report (my emphasis):

This guidance was predicated upon a global recovery gradually taking hold. With the exception of the USA and some Asian territories, global trading conditions have generally deteriorated significantly…Further information on likely developments in the operations of the Group and the expected results of operations have not been included in this report because the Directors believe it would be likely to result in unreasonable prejudice to the Group.

That says it all – they won’t even talk about their FY12 projections because they think it will scare the pants off the market. Not a good sign.

Management

Billabong’s board draws heavily from experience with the surf industry and average tenure is quite high, with the founder Gordon Merchant still active. Outside corporate experience is relatively light on, with non-executive director Margaret Jackson providing the bulkiest resume after stints at BHP, Fairfax, Qantas, ANZ, Southcorp and Pacific Dunlop.

As stated above, there has been a serious decline in return on capital as well as an increase in debt to fund acquisitions at a time when retail sales are soft. This raises serious questions about management ability to weather tough trading conditions.

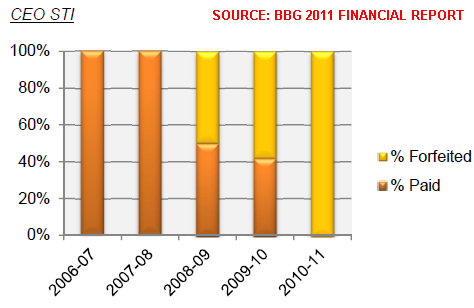

As with many listed companies, BBG has made big changes to its remuneration policies in response to shareholder pressure. Short term incentives (STI) payments now have a larger portion (25 to 30%) deferred into equity, which vests after two years and is forfeited should personnel leave during the vesting period. STI goals are based around NPAT, EBIT and non-financial objectives.

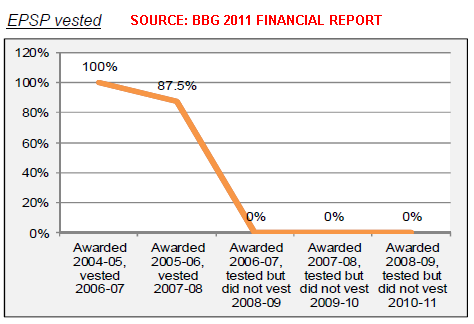

The long term incentive (LTI) payments are made as shares in BBG. LTI was based solely on earnings per share (EPS) and the recipient could still receive dividends on shares which had not vested yet. This cushy arrangement was changed in FY11, with 50% of the LTI measure now based on total shareholder return (TSR, a measure of share price and dividend performance) over a 3 year period, with the remainder based on EPS. Dividends for non-vested shares will also be withheld. Whilst the TSR change is welcome, it is still a relative measure against an Index of ASX listed company – so LTI can be high in a bad year so long as BBG does better than the market average. The measures still don’t guard against excessive debt loads, which can be used to bolster EPS (and hence share price) in the short term.

Despite my concerns on remuneration alignment, BBGs performance has been so woeful over the last few years that STI and LTI payments have fallen to zero since 2006, as shown in the graphs below from the FY11 financial report. Not surprising given the share price has fallen from $17.96 in 2007 to $1.70 today.

Risks

- Poor earnings resulting from continued soft retail sales in all major market segments

- Forex risks from large offshore revenues

- High debt load, much of which is dominated in foreign currency

- The possibility of BBG violating debt covenants and needing to raise capital or sell assets to satisfy creditors

Opportunities

- If BBG turn around their recently-purchase retail store margins and the AUD drops a little, they may climb out of the hole they are in now

- Trading below its equity per share value (but for a good reason)

Summary

In summary, Billabong had a great brand name, high ROE , high margins and moderate gearing during the good times. Unfortunately those advantages have been lost after debt-and-capital-fuelled acquisitions, just as the global consumer retreated and the AUD skyrocketed.

Three years ago I would have called Billabong Group a good company and thought it to be relatively well placed to weather a downturn. Today I see a discretionary retailer with too much debt and far more downside risk than upside.

I do not consider Billabong Group an investment-grade company.

Valuation

Assuming an equity per share value of $4,70, ROE increasing from 5% to 10% over a 5 year period and a reinvestment ratio of 10%, I would value BBG around $2.50.

However, given BBG’s debt problems the equity per share level may be far lower in the future, either as a result of asset sales or a capital raising. As such, I wouldn’t buy BBG shares even if they traded at a significant discount to this value.

It’s just too risky, dude.

Disclosure: The author is a Director of a private investment company (Empire Investing Pty Ltd), which has currently has no interest in the business mentioned in this article. The article is not to be taken as investment advice and the views expressed are opinions only. Readers should seek advice from someone who claims to be qualified before considering allocating capital in any investment.