As the summer of discontent continues for our retailers, so too the woes for JB Hi Fi’s (JBH) share price. Whilst the recent drop has created a lot of unsightly red in share portfolios (yours truly included), big price shifts can also create big opportunities. Given the depressed price of JBH, it’s time to consider a hypothetical takeover, by competitor and diversified retailer Woolworths (WOW).

JBH recently announced a 5% drop in EBIT for the year to November (compared to FY11), which resulted in a massive 25% drop in the share price. Of course JBH wasn’t alone, with Billabong, Kathmandu, Myers, David Jones and Harvey Norman also experiencing share price pain as earnings results disappoint the market.

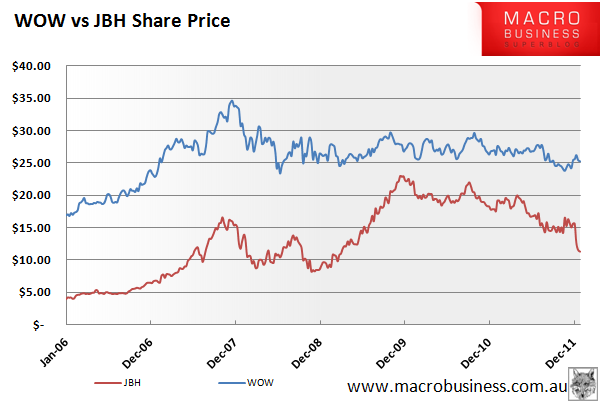

Woolworths (WOW) has been immune from the experiences of its retail peers due to the non-discretionary nature of the majority of its sales. Consumers can decide to forego the latest 3D LED HD TV to save a buck, but they still need the basic necessities of life (like food and alcohol) provided by “our Woolies”. This resilience can be seen in the graph below of WOW and JBH share prices for the last 5 years. Note JBH falling off a cliff in late 2011, whilst WOW bounced from a multi-year low during the same period.

That said, WOW’s own discretionary electronics business – Dick Smith (including Tandy) – has also been doing it tough. In the last market update WOW nominated it as an underperforming segment, largely due to superior competition from JBH as well as the disleveraging consumers and price deflation. whose future was under review.

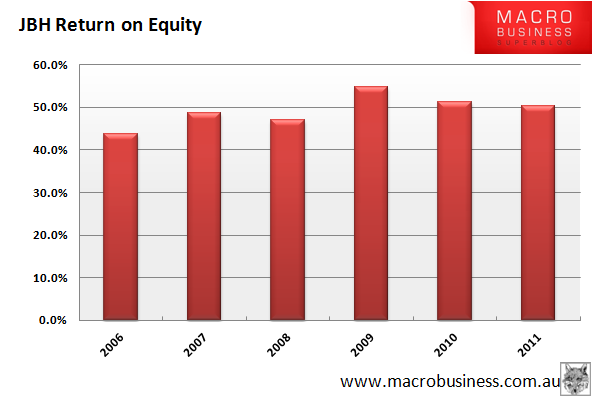

Despite the retail gloom and doom, JBH should still be considered one of the best retailers in the country due to its high return on capital, high-demand products and good capital management. The plummeting share price discounts these facts and it doesn’t help being the most shorted stock in the entire market. We are also in the midst of a 1000 point decline in the ASX200, meaning most shares are being taken out with the market tide. However it still doesn’t change the fact JBH is one of the best in its sector. Return on equity (ROE, shown below) has averaged 50% over the last 5 years and the JB Hi Fi name has become synonymous with cheap music and electronics.

With its relatively low price (dividend yield of 7.1%, grossed up over 10%) and modest price/earnings ratio (PER) just under 9, amidst a struggling sector with inferior competitors, it is probably a bargain stock at the moment – both for retail investors and potential corporate suitors. Which leads us back to Woolies..

Could Woolies buy JBH?

At the current share price of around $11.25, JBH’s market capitalisation is about $1.1 billion – just over 1/30th of WOW’s market capitalisation of $30b. In terms of profit-generated purchasing power, WOW’s net profit after tax (NPAT) for FY11 was about $2.1 billion. Of this, some $400 million was reinvested with the remainder distributed as dividends. WOW could potentially buy JBH with one year’s profit by simply reducing the dividend payout. If it did, however, the share price would surely be hammered by the dividend-loving market.

WOW’s interest bearing debt is about $4.8 billion, with interest expenses of approximately of $400 million for FY11. If WOW were to buy JBH solely using debt, borrowings would increase to about $6 billion (more if a premium were paid on the share price) whilst interest expenses would hit about $500 million per annum. The increase in interest costs would be affordable, however the overall debt increase would see borrowings come to about three times NPAT – not high, but not great either.

Should Woolies buy JBH?

In buying JBH, Woolies would acquire a top-performing electronics retailer – something it has failed to develop in Dick Smith Electronics. It would also pick up a brand-name business with great ROE, relatively low debt and sales margins around 4% as opposed to the 1.5% generated by Dick Smith in FY11. Woolies would also be able to stop the price war between the two chains and could arrest some of the competitive deflation seen in product prices over the last 12 months.

On the flip side, Woolies has sunk a considerable amount of capital into rebandging and renovating Dick Smith stores since 2008. It has also opened up a new retailing front against Bunnings Warehouse (owned by Wesfarmers) with its own Masters hardware stores. In addition, WOW increased its debt load recently to pay for a share buy-back. Given all this capital activity, WOW may be reluctant to plough another lazy billion into their electronics segment.

Aside from the financials, the other risk to a buyout is management change. JBH’s success derives in-part from its culture of low-cost, no frills stores/fixtures and management’s commitment to high return on shareholder capital. JBH is also adapting to the realities of online retail with the “JB Now” service – a paid-for music streaming service. While it’s success is not assured, the rumoured subscription price of $7 to $8 per month should make iTunes look horrendously expensive. At the very least, JBH is trying to make the most of online opportunities while its peers are either ignoring them or building belated web presences. Woolies would be wise to let JBH continue business as usual.

All in all, if WOW hadn’t embarked on a debt-financed share buy back recently, I think a JBH takeover could have been a bold and positive move with minimal stress to the balance sheet. But given their current debt levels I would like to see them deleverage somewhat before getting adventurous. They also have time on their hands – the Euro debt crisis could see retail shares driven down even further as consumers keep saving their discretionary pennies, but the flipside to that is a deteriorating macro environment both in Europe and China, particularly wage inflation in the latter.

As a shareholder of both companies, I wouldn’t mind a happy marriage at some point in the future. Just not now.

Disclosure: The author is a Director of a private investment company (Empire Investing Pty Ltd) and currently has interests in the businesses mentioned in this article. The article is not to be taken as investment advice and the views expressed are opinions only. Readers should seek advice from someone who claims to be qualified before considering allocating capital in any investment.