![]() It’s been raining Macquaire (MQG) blogs at MB this week and last, so I’m going to add my two cents worth in this week’s equities spotlight article. Next week, I’ll be followng up with a Bonds Spotlight article on the Macquarie Note MBLHB.

It’s been raining Macquaire (MQG) blogs at MB this week and last, so I’m going to add my two cents worth in this week’s equities spotlight article. Next week, I’ll be followng up with a Bonds Spotlight article on the Macquarie Note MBLHB.

The Business

Macquarie is a global financial services company with over 15,000 employers, just over half of whom are based outside Australia. It acts primarily as an intermediary for institutional, corporate and retail clients around the world, with a particularly strong presence in the Asia-Pacific region. Macquarie services include (but are not limited to):

- Equities research and stock selection on over 1,200 stocks in the Asia-Pacific region

- Management of infrastructure funds (listed and unlisted), with over $90A billion in assets under management

- Management of agricultural funds, with more than 3 million hectares under the Macquarie Pastoral Fund

- Management of real estate assets and funds

- Arrangement of cross-border financial transactions (e.g. IPOs of Chinese companies in European markets, international debt/bond issuances)

- Trading and risk management services in fixed-income, currencies and commodities (hard, soft and energy)

- Trading of physical energy commodities such as gas, oil and ethanol

- Financial services for debt, equity and price risk management to major commodity producers and consumers

- Retail stock broking, wealth management and full-service banking services, with over 1 million customers internationally

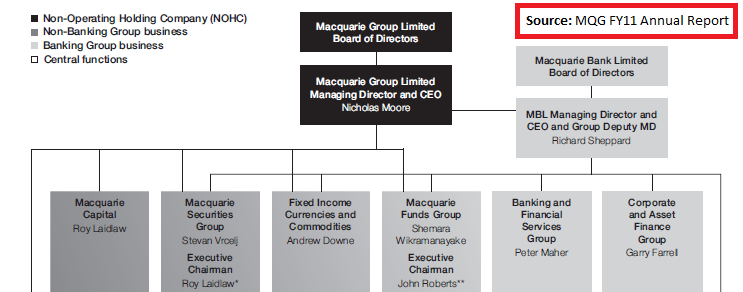

So basically, if there’s a transaction in any major commodity or between any major companies in the world – especially in the Asia-Pacific region – MQG would like to get a piece of it as an intermediary player. They also offer fully-fledged banking and wealth management services for retail clients. A full sectoral breakdown is shown below.

Whilst this sounds reasonable from a macro viewpoint, I still have no idea how MQG makes money. . Their vast reach and the financial products they produce are just too broad and complex for me to understand fully. As an investor, I never invest in companies that I don’t understand. Companies like Woolworths, Onesteel or JB Hi Fi are easily understood – I know how they make money and can use that knowledge to make judgements about future performance. I can’t say the same for Macquarie Group.

The Financials

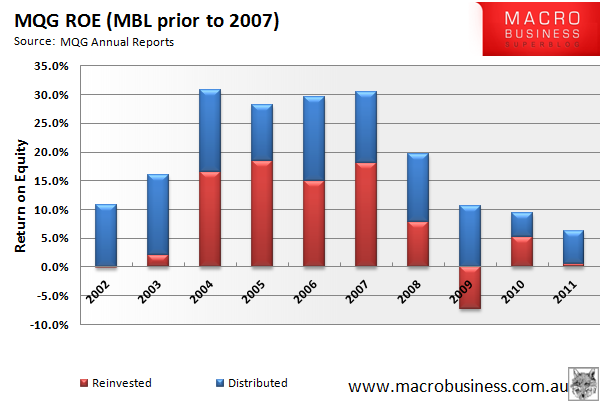

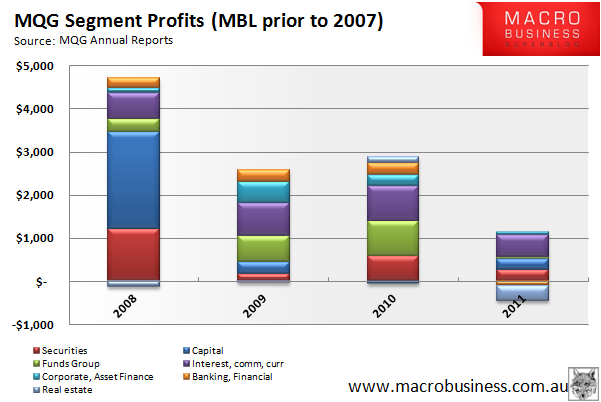

Macquarie’s return on equity had a great run during Mining Boom mk I – averaging around 30%. However, since then ROE has trended down and came in just over 6% for FY11. MQG claim part of this is due to the increased capital on their balance sheet. Another reason would be the big drop in earnings from their Capital segment, which manages M&A, IPOs and other capital market services for corporate and government clients.

Net profit after tax for FY11 was $956 million in 2011. This compares to a high of $1.8 billion in 2008.

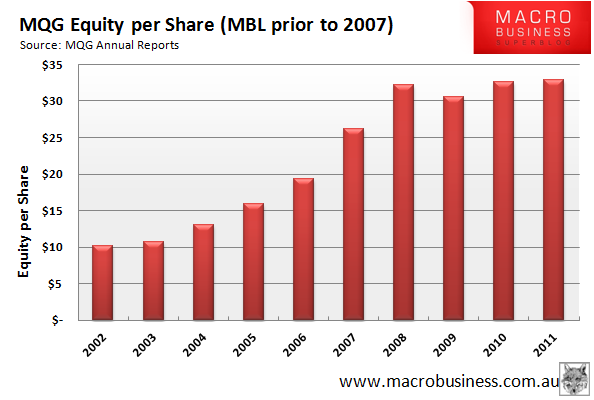

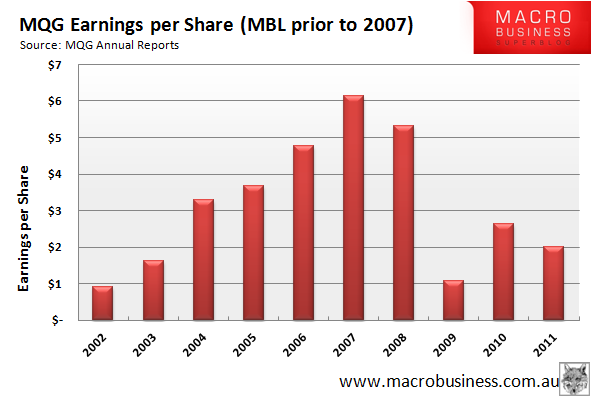

Equity per share plateaued after a big increase running into the GFC. In the face of dropping NPAT, a large capital raising in 2010 and dropping market values of MQG-held securities, earnings per share has fallen significantly to maintain equity per share levels.

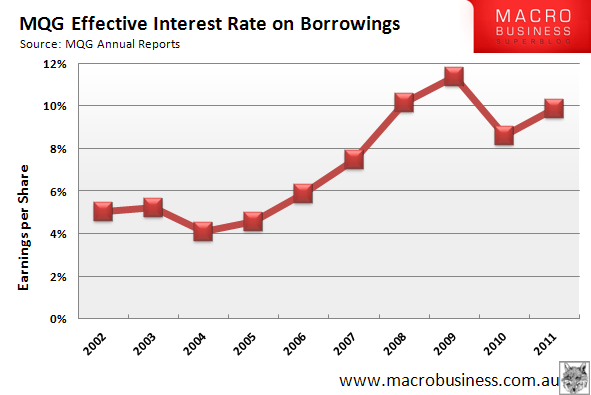

Whilst debt levels have decreased since the GFC, the relative interest costs have remained elevated compared to the pre-GFC era. The graph below shows the effective yearly interest, calculated by dividing interest expense cashflows by MQG’s interest-bearing debt. It’s a crude measurement, but it shows a definitive shift in funding costs. It’s another possible explanation for the lacklustre ROE of late.

In a slap in the face to all the dividend huggers, MQG stopped issuing franking credits with its dividends in FY11. Management claim this will continue into the foreseeable future, although I couldn’t find a decent reason as to why they were doing it.

Management

Seven of MQGs eight board members are independent directors and most have been associated with either Macquarie Group or Macquarie bank for at least 5 years. The CEO and Chairman have been long-term MQG employees, with over 35 years experience between them. In a similar vein, the average tenure of the 12 executive committee members is 18 years.

The resumes of the board members include names like Origin, ASX, Westpac, Telstra and Bluescope whilst philanthropic endeavours are common. Sadly long-serving Chairman David Clarke passed away in April 2011, taking with him 40 years of experience as one Macquarie’s founding fathers.

The remuneration report is mammoth – it takes up 51 of the 270 pages in the FY11 annual report. Macquarie wholly embraces the use of performance-based pay, believing a high proportion of at-risk pay for its executives is the best way to align employee and shareholders’ interests. In fact, despite the recent push for increasing fixed-income remuneration amongst Australian listed companies, MQG prides itself on retaining relatively low levels of fixed pay compared to their peers. The primary remuneration performance hurdles for MQG appear to be return on equity and net profit – which is music to my ears as most other ASX-listed companies use easily-gamed metrics like “total shareholder returns” or earnings before interest and tax. In a nod to recent remuneration trends, more performance pay (50-70%) is being granted as deferred MQG equity (or allocated to MQG managed funds) than in previous years. This is a big change to previous years, where up to 80% of performance based pay was paid as cash.

Macquarie certainly lives up to its moniker as “the millionaires factory”, with remuneration for the top 12 executives totalling $58.9 million in FY11 – or about $4.9 million per person per annum. This is equivalent to about 6% of the NPAT for FY11. The total employment costs for FY11 were $3.7 billion.

Risk Management

MCQ dedicate some 16 pages of their FY11 annual report to risk management. They have set up a number of processes to manage risks – from an independent risk management group to various methods of calculating losses and equity requirements in the event of large market correction. I thought I’d take a deeper look to see if their risk management practices would allay my fears on the mysteriousness of their earnings methods. The following processes caught my eye:

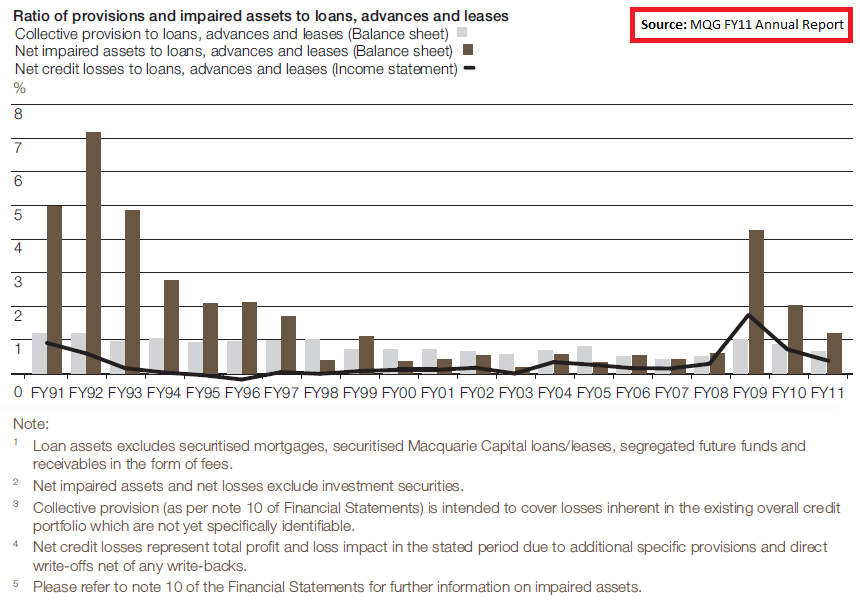

Loan and Asset Impairments: The ratio of provisions and impaired assets to loans, advances and leases are shown below. Note the big uptick after the GFC and the even larger impairments experienced during the “recession we had to have” in the early 90s.

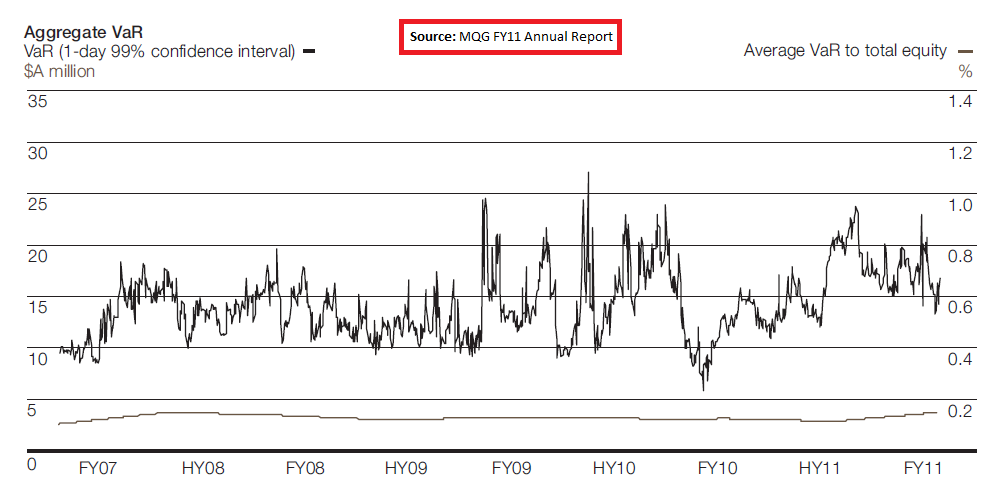

Value at Risk: According to the FY11 report, MQG calculates Value at Risk by using (my emphasis):

“a Monte Carlo simulation to generate normally distributed price and volatility paths for approximately 1,400 benchmarks, using volatilities and correlations based on three years of historical data. Emphasis is placed on more recent market movements to more accurately reflect current conditions. Each benchmark represents an asset at a specific maturity, for example one year crude oil futures or spot gold.”

According to the chart below, MCQ has very low exposure to benchmark/asset volatility when compared to total equity.

While I think a little statistical analysis is a good thing for risk management, I believe the emphasis on short term/more recent movements is a weakness in MQGs approach. In fairness, MQG use this as a “99% confidence level” tool for price volatility, with scenario analysis used for extreme situations/back swan events. However, I’d argue more than 3 years of data is required to get this sort of confidence level given the historical frequencies of “extreme” market events like the GFC. If you were to take a Ben Graham approach, you’d be looking over a +40 year timeframe.

Risk Appetite Test: MQG uses the “Risk Appetite Test” to quantify losses and earnings expected under a severe economic downturn. Namely:

- a drop in earnings more severe than what was experienced during the global financial crisis,

- potential losses more severe than what was experienced during the global financial crisis.

Once again I think this reference is a little too short term. The GFC was a scarring event but there’s no guarantee it was a worst-case scenario. Obviously you can’t plan for everything and operate with zero risk – impossible in a business setting – but maybe a little conservatism on top of what has already happened would be prudent.

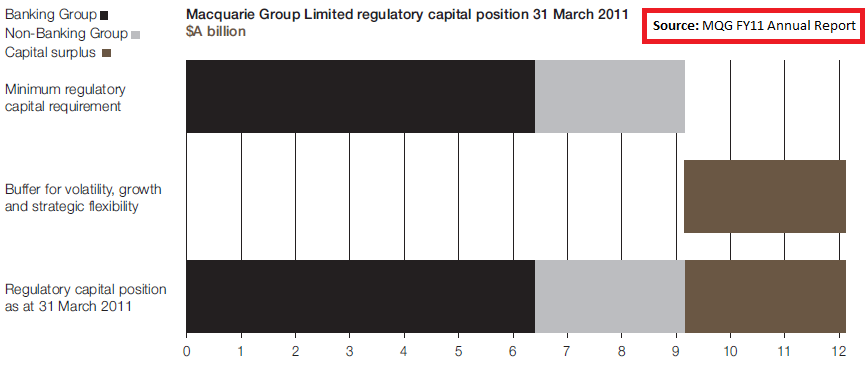

Capital Adequacy: Macquarie claims to follow a policy of being well capitalised – meaning well in excess of minimum regulatory requirements. This is done to provide support to growth opportunities as well as act as a buffer against volatility. MQG assess their capital requirements against equity, credit and operational risks as well as the risks inherent in their trading activities. They also claim to use only a fraction of future earnings as a buffer against losses – which is prudent given their earnings should the general market direction.

As Deep T has written numerous times on MB, banking capital adequacy calculations are obscure at the best of times. I also don’t have access to how MQG calculate their asset values, so I won’t bother trying to assess MQG’s methods. However, below is a graph from the FY11 report showing MQG’s capital holdings compared to regulatory requirements.

If MQG is correct in its capital calculations, it has a buffer of about 30% above the minimum regulatory requirements. This appears prudent, but as always the devil is in the detail of how their capital levels are calculated. Could a dramatic writedown in one of their infrastructure funds impact this seemingly large buffer?

Liquidity Policy: For both the banking (MBL) and non-banking (MQL) arms of MQG, the liquidity policies state:

- MBL/MGL is able to meet all of its liquidity obligations on a daily basis and during a period of liquidity stress: a 12 month period of constrained access to funding markets and with only a limited impact on franchise businesses.

So in other words, there must be enough cash and liquid assets to cover 12 months of stressed liquidity. In addition, MGL has no short-term wholesale funding. Both good policies.

Whilst all these risk management approaches appear sensible, I still have no grasp on how effective or how rigorous they are. Some of the historical timeframes are a little short for my liking too, so I am still uneasy about MQGs business model as a whole.

Risks

- Fully understanding MQG is difficult and hence determining the soundness of equity levels and future earnings is also difficult

- The performance of MQG seems tied to the share market, particularly M&A activity

- Future legislative/regulatory changes may impact capital requirements and further depress ROE

Opportunities

- The share price is trading below the current equity per share levels

- MQG may prosper if the European crisis is solved and share markets turn bullish

Summary

Despite pouring through their FY11 annual report (and a fair chunk of past reports), I still find MQG a bit of mystery. Exactly how it generates earnings and productively employs over 15,000 people is beyond my scope of knowledge. It was the share market darling prior to the GFC – hitting a high of $98.64 in May 2007. However, both share price and earnings have tumbled since the GFC, as has ROE. The once super-profitable capital segment is a shadow of its former self whilst interest costs have stayed relatively high post-GFC.

MQG is an unknown entity to me, as such I consider it non-investment grade. This is not to say MQG is a bad company – it’s just one that I don’t understand.

Valuation

Using an estimated equity per share of $33.90, ROE of 7.5% (increasing to 10% over 5 years) and a reinvestment ratio of 30%, I value MQG around $24.98.

This is well below their current equity per share levels, but even if the value was higher I still wouldn’t buy MQG shares because I just don’t know enough about their business. Their risk management approaches may look good on paper, but I am not confident in how their equity levels are calculated or how they are going to make the big bucks in a future full of soveriegn credit woes and potentially high credit costs. And I wager most other investors don’t either.

Disclosure: The author is a Director of a private investment company (Empire Investing Pty Ltd), which has currently has an interest in one of the businesses mentioned in this article. The article is not to be taken as investment advice and the views expressed are opinions only. Readers should seek advice from someone who claims to be qualified before considering allocating capital in any investment.