While the residential property market continues its slow melt, property industry experts are seeing the green shoots of a recovery in commercial property markets, especially in Brisbane, the headquarters of Queensland’s CSG and coal investment boom.

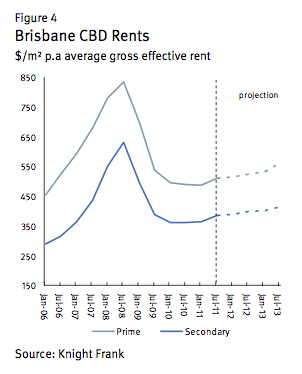

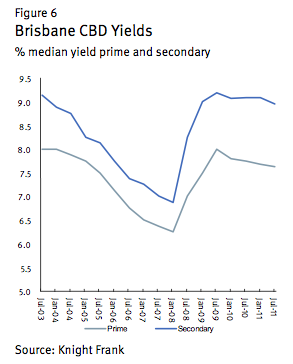

Yields have stabilised (for CBD and near CBD office) at pre-boom levels, and rents appear to have bottomed for now, although sales volumes remain historically low. These two factors combined have seen commercial office prices level off around 40% below their peak. Vacancy rates are now also declining. The charts below show the turbulent boom and bust cycle experienced in this market over the past eight year or so.

I don’t see indications of values rising at escape velocity again in the near future, with plenty of supply coming online, and subdued demand for space. The mining industry has already committed to its space needs, and is unlikely to expand these requirements again in the short term. A growing trend toward CBD fringe locations, and plenty of supply coming online in Fortitude Valley, Spring Hill, Milton and South Brisbane, will keep CBD prices contained even if economic conditions improve substantially in the next year or two.

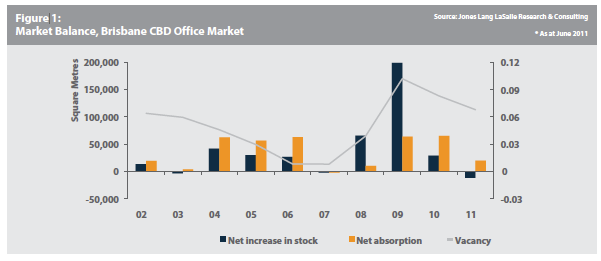

Also important to note is how lumpy investment in commercial space can be. The three major buildings currently under construction in Brisbane comprise 6% of the total CBD stock (or about 130,000sqm) and are 60% pre-committed. The completion of these buildings alone will push the vacancy rate up 2%. In keeping with the trend towards gentrified CBD fringe locations, Suncorp’s recent deal to relocate 3,000 staff a 48,000sqm new office tower at Southbank will open up significant ‘back-fill’ space in the CBD over the coming years.

The impact of a slightly larger supply boom in 2008 and 2009 lifted the vacancy rate from 2% to near 12%, with rents falling around 20% during 2009 (see chart below). With the amount of new supply coming online in the next two to three years, and the likely continuation of subdued absorption rates (the net demand for new space), rents are unlikely to significantly outpaceCPI, or perhaps fall a little, in the near term.

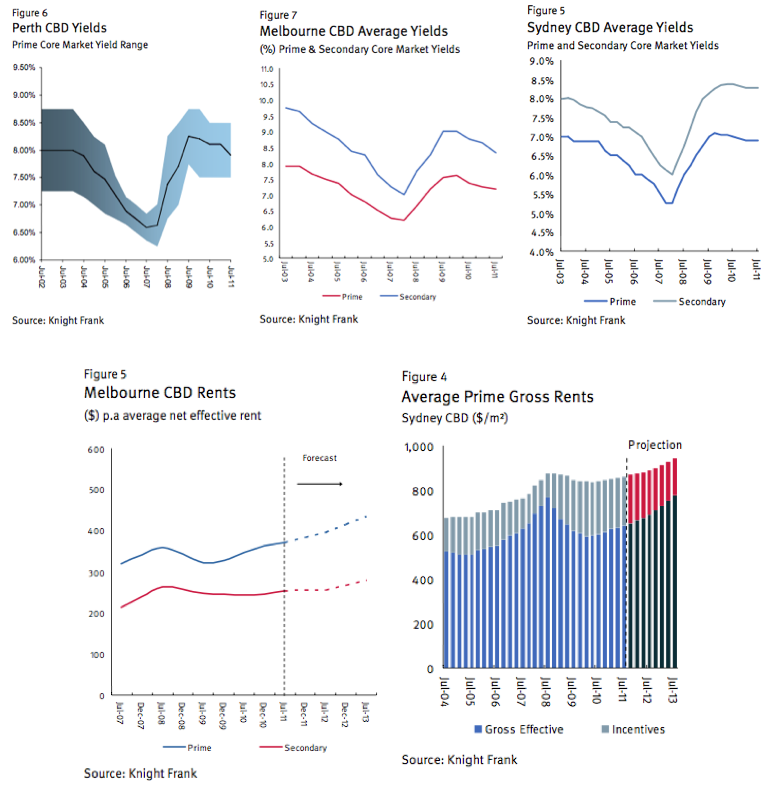

In Sydney, Melbourne and Perth, markets I am less familiar with, indications are that CBD commercial property values have substantially deflated, but are now stabilising. Sales volumes remain low but yields are beginning to tighten a little, and rents have flattened or are rising.

In all capitals, sales activity in the near future will be driven by institutional owners seeking better opportunities for returns elsewhere. Given interest rate expectations, I personally don’t see many such opportunities.

The big question mark is the degree to which some institutions may be under pressure to sell their assets to repair their balance sheets. In this event, potential negative feedbacks from generational lows in household credit, white-collar unemployment, and a stagnant retail sector may have a much stronger price impact.

A likely scenario in Brisbane is for slow grinding improvement in yields, partly driven by the expectation of an interest rate tightening cycle, with rental growth hovering around CPI (but probably below). In effect, the expected behaviour of a rational market. Worst case is for moderately declining prices over the next three years. This could occur if rents take another negative turn, due to substantial supply hitting the market, and some forced selling ensues.

Investing in Brisbane commercial property at this time is only for the very bold, but strongly depends on the attractiveness of this risk profile to other current investment opportunities.

Tips, suggestions, comments and requests to rumplestatskin@gmail.com + follow me on Twitter @rumplestatskin