Australian cities are uniquely monocentric, with a highly dense core of both residential dwellings and commercial activities, and far-flung low-density suburbs. For the investor, the pattern of growth of the city is important for two reasons.

- It explains the strong relationship between yields and distance from the CBD for all property types, and

- it demonstrates the actual behaviour that leads to higher volatility in values in fringe areas.

An urban economics course at any university will begin by explaining the logic of urban agglomeration. They will start with a spatial model of a single road with two users competing for passing trade. Assuming a uniform distribution of traffic in all forms along the road, most students intuitively believe that the optimal position for the two users, to maximise exposure and accessibility to passing traffic, is at each end of the road.

Unfortunately, this intuition is wrong. Because if they did both locate at either end, each user, say a retailer, could capture more of the market by moving towards the centre. If, for example, one retailer stays at one end and the other shifts to the middle, the retailer in the middle of the street is most accessible to 75% of the street traffic. Thus, the optimal competitive outcome that maximises exposure to passing trade is for each to locate side-by-side in the centre of the road. This is one reason why certain types of businesses cluster together, for example food courts, tailors in Bangkok, and carpet sellers in Moroccan cities.

Once students grasp the logic, the model is expanded to add additional roads to create a network. The optimal location then shifts to intersections of the network that offer maximum exposure to passing traffic, and maximum accessibility, from two or more roads. In real cities, the network typically grows to reinforce this location as the most accessible, since any new development will need access to existing commercial activities, thus market outcome of a mono-centric city is born. Almost every city in the world has an intersection of streets in the network commonly referred to as the cities absolute centre.

Urban areas grow outwards due developments in transport that allows the same accessibility over a larger distance. A century ago most suburbs were walking distance to the inner city, which is also where ports and heavy industry was located. Trams development allowed people to escape the filth of the city, and for a time it was the wealthy living further from the city, having both space and cleanliness, but maintain accessibility to the central commercial hub. The past 25years has seen gentrification of these inner areas and a return to residential densification.

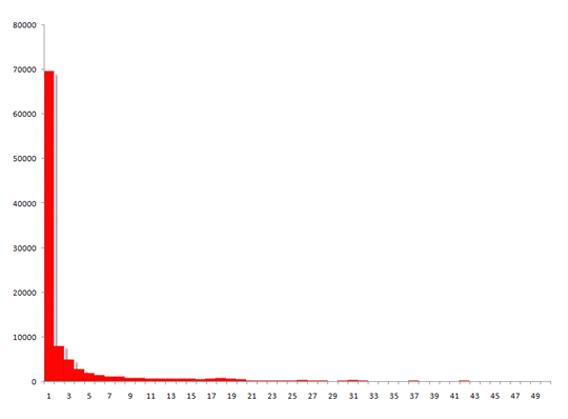

The images below show just how much Australian cities have developed in line with the theoretical expectations. The first shows the employment density of each 1km concentric ring from the Melbourne city centre:

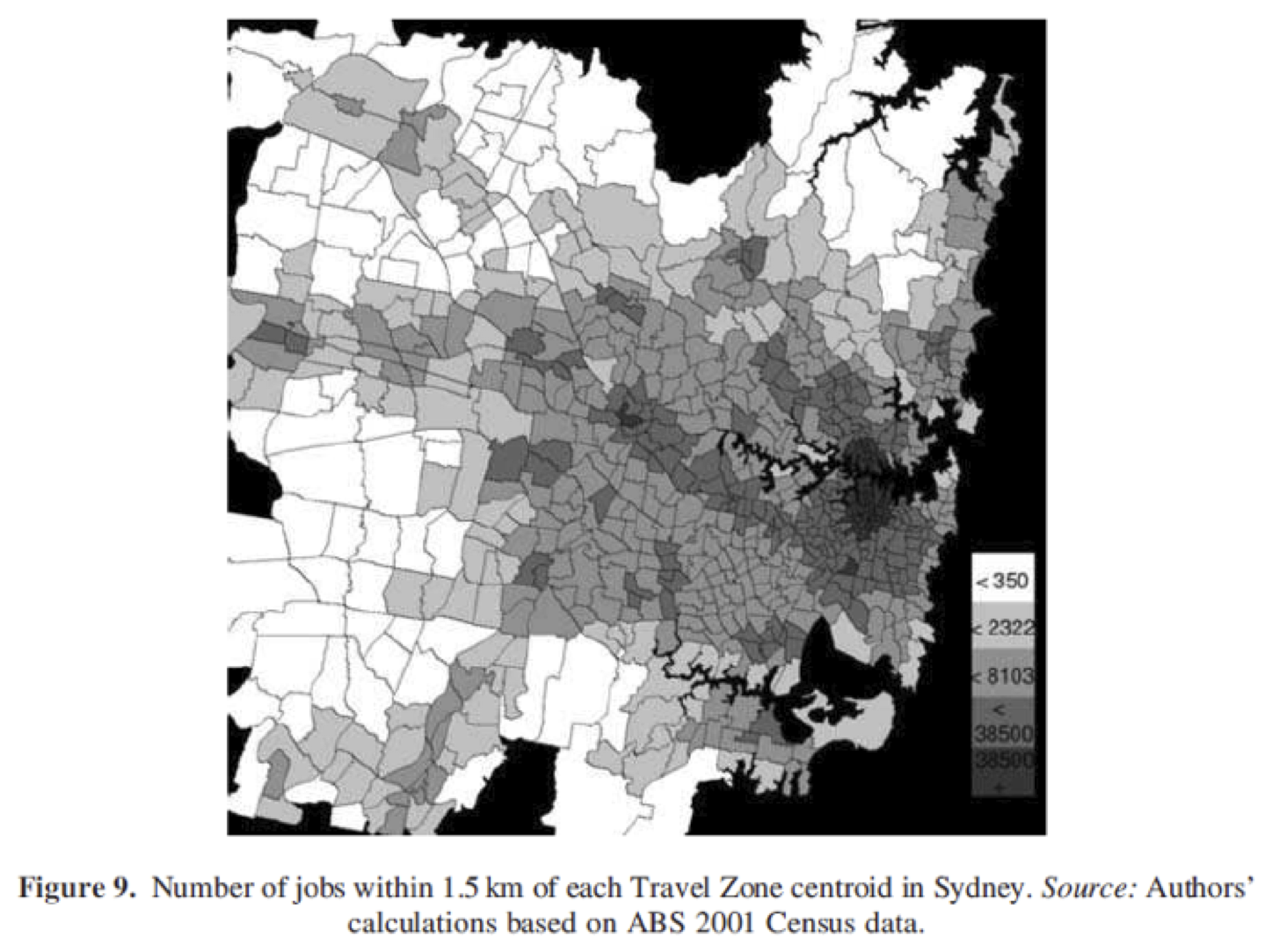

Following a similar pattern, the below map of Sydney with the number of jobs within a 1.5km radius of the centre of each marked zone:

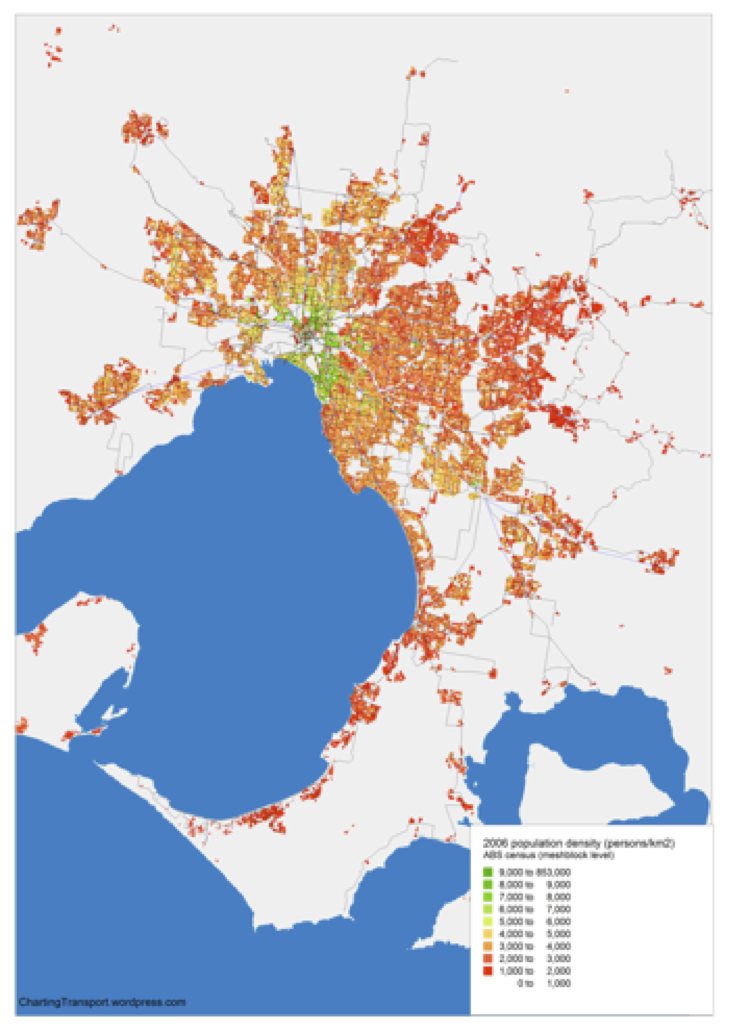

Below is a map of Melbourne residential density:

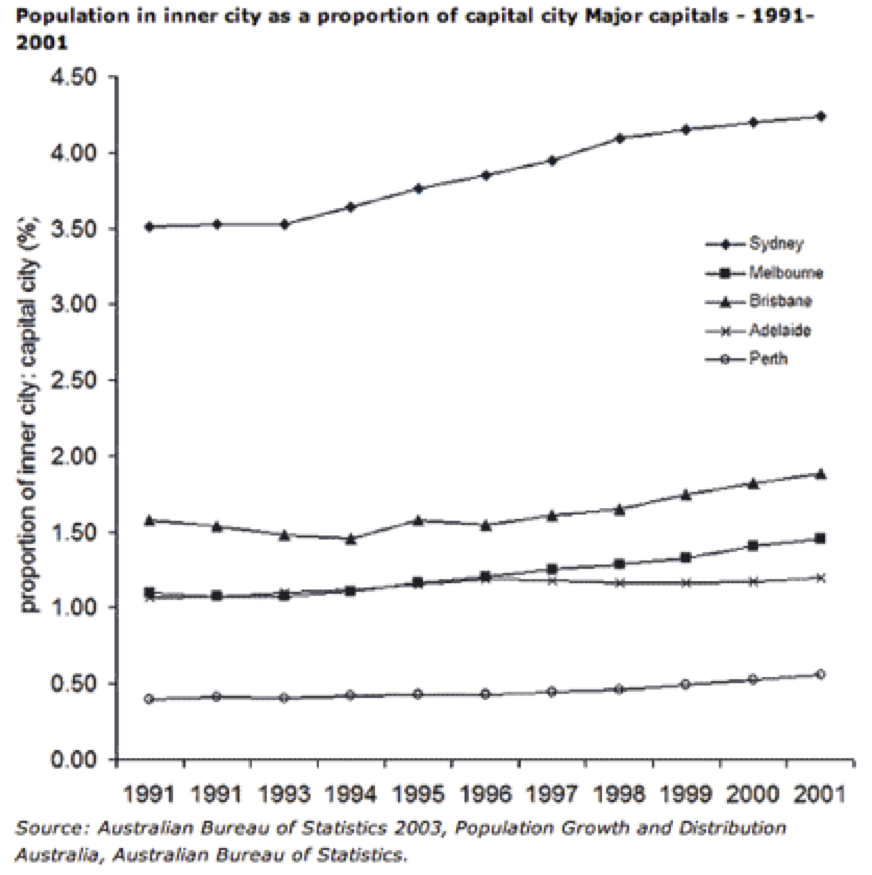

Finally, the below graph shows the increasing dominance of the inner city as a share of total city populations in our capitals since 1990, with recent data confirming this trend has continued:

In 2009-10, the inner-city LGAs of Sydney (C) and Melbourne (C) had population increases among the largest in Australia…

The 2009-10 growth rates in the inner capital city LGAs of Perth (C) (5.1%), Melbourne (C) (3.6%), Sydney (C) (2.5%) and Adelaide (C) (2.2%) were lower than their average annual growth rates over the five years to June 2010.

Why is this relevant? Well, to point out the obvious, it is relevant because non-institutional property investment disproportionally takes place on the city fringes. This occurs across all property types. I believe, however, that this group of investors currently grossly underestimate the locational risk, and hence city fringe property values are likely to be extremely volatile, more so than if such investment decisions were based on cold reflection of real risks.

We know that greater accessibility leads to higher property values:

… for a given point, the shorter the trip to all potential destinations, the higher should be the value of land. A geometrically central location will provide trips of a shorter length to all other location in the city.

And the city centre typically provides this. Which is why, when consolidation of space occurs during economic slumps, across all property classes, any fall in prices will make inner city areas more attractive. The actual behaviour that causes the relative stability of the inner city comprises a number of factors.

- The relatively more financially robust tenants (in all property classes),

- a more diverse market for tenants,

- the lengthy leases possible with larger more established tenants (for commercial property),

- the latent demand for inner city locations when prices fall, and

- the ability for other property owners in the market to avoid forced selling.

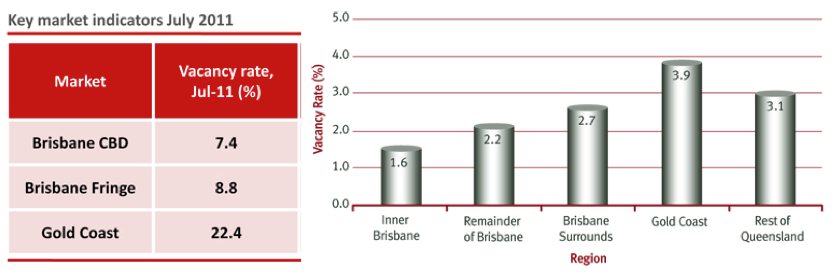

This behaviour results in lower vacancy rates and more stable prices, which is widely recognised by the industry. The below table is a typical example from Brisbane’s commercial and residential markets:

{kind=link}

The reverse is also true during boom times, when a tight inner city market means that outer areas capture the ‘spillover’ of demand, leading to an amplification of property market volatility in fringe areas. A very diverse polycentric city on the other hand with multiple districts of intense commercial activity will have a flatter profile of volatility across the city. There are many examples, especially in Europe and former Soviet states, were such multiple centres exist, often in the form of new and old city centres, with new centres constructed due to planning controls of old parts of the city. Australian planners are definitely looking to emulate multi-nodal networks of activities within the urban footprints of our capitals.

The natural tendency for centralisation, plus planning intentions for urban nodes, means that the prospects for price stability relative to yields in Australia cities appear quite favourable in inner suburbs, say from 3-6km from the CBD. Without being specific, locations in this radius with scope for densification (unlike many established ‘blue chip’ suburbs) could lead to gains on local values (relatively), in addition to their locational value relative to the CBD. Given that residential demand trends are shifting away from the suburban detached dwelling, towards well located attached dwellings, the ingredients are ripe for out-perfromance in these areas, particularly property with potential to value-add or redevelop.

These tangible on-the-ground realities of Australia’s capital city property markets should be properly understood by all market participants, especially, the new private investor in fringe suburbs looking for a long term store of value.

Tips, suggestions, comments and requests to rumplestatskin@gmail.com + follow me on Twitter @rumplestatskin