Australian economist Steve Keen has released a second edition of his book Debunking Economics. It should be compulsory reading in any economics course, and certainly contains many lessons for policy makers.

I will state up front that I have been a follower of Keen’s work for some time, having read some of his academic publications , his top quality blog, and the first edition of Debunking Economics some years back

As the title suggests, this book is a step by step debunking of the mythological assumptions at the heart of neoclassical economic theory; the theory that is almost exclusively taught in undergraduate economics courses and subsequently drives much of the mainstream economic thinking in markets and public policy. Keen rails against the indoctrination of economics students through the teaching of completely debunked theories that even their originators have disowned (for example, Robert Solow has criticised the widespread misapplication of his growth model in the economics profession).

I would go so far as to say that the primary purpose of the book appears to be to shine a light on the ridiculously poor condition of economics as a discipline, and the perpetuation of falsified theories through poor, or narrow, teaching at universities. Keen was certainly impressed when Havard’s first year economic students walked out on Greg Mankiw’s economics class last month, citing the narrow agenda presented in economics teaching as less than satisfactory. But this was also one of my main concerns with the book. I felt I was part of an alternative economic indoctrination from the repetitive emphasis on the poor state of the discipline. My message to Steve – if someone is reading your book, they are highly intelligent and already critical of the discipline of economics. They will get your point the first time.

Overall the book contains high quality accessible analysis. Here is a short selection of some ideas from Keen’s book that really stuck with me.

Demand curves are any shape at all and supply curves don’t exist!

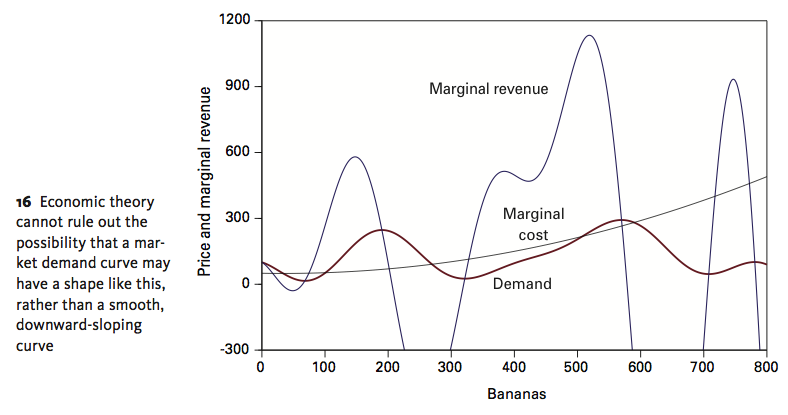

One of Keen’s core ideas from the first edition of the book, which has since been the subject of intense debate, is that demand curves can be any shape at all, and the Law of Demand, which suggest that demand curves are always downward sloping, is just a single special case all possible demand curves. Given that the literature finds upward sloping demand curves for individual goods (either Giffen goods or Veblen goods) such as rice in China, or luxury branded items, as well as asset markets (through bandwagon effects and others) this seems quite plausible.

Indeed, the heart of Keen’s criticism of demand curve analysis is the fundamental aggregation flaw requiring that for a downward sloping market demand curve to exist, the whole market needs to me considered as a single individual at the mean income level with perfectly fixed preferences (which is a huge simplification of the few dozen pages of Keen’s analysis). This is nonsense of course, since markets require different individuals with different tastes and preferences to actually function. Keen cites numerous originators of microeconomic theory who have demonstrated that demand curves can have any shape at all (so long as they can be fitted by a polynomial equation).

The figure below, from the online supplement to Debunking Economics, demonstrates that uselessness of traditional microeconomic theories of demand once aggregation fallacies are rectified.

Regarding supply curves, Keen shows that marginal cost pricing almost never occurs in reality. He builds on Piero Sraffra’s 1926 critique of theories of the firm, contending that production and price setting decisions are not the result of internal firm cost patterns, but solely from external market demand limitations (the share of the market able to be captured). Although I would suggest again that the neoclassical ideal is a special case of the more general model Keen presents, and is particularly relevant in markets for natural resources, which do often face rising marginal costs.

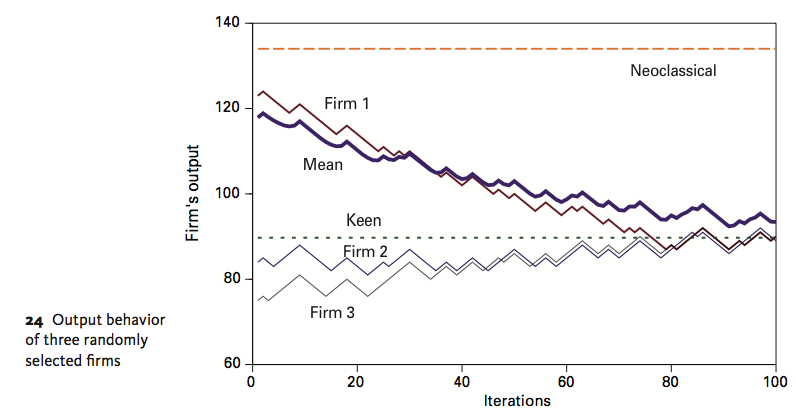

Keen also demonstrates the aggregation fallacy that leads most economists to believe that monopolies will restrict output to increase prices relative to a competitive market. In fact monopolists are likely to produce just as much as competitive firms, at the same market price. Neoclassical assumptions of perfect competition do not maximise profits, and therefore overestimate market output (as shown in the graph below). The real problem with monopolists is their market bargaining power in specialist labour markets, which is why unions have a role to play.

Going further, Keen asserts that macroeconomics cannot have micro economic foundations due to its emergent properties, and should be studied at a separate level of understanding in the same way that chemists and biologists usually ignore subatomic physics to understand the properties of chemical systems. Macroeconomics with micro foundations is the same as biology with foundations in subatomic physics – no meaningful information will come from the pursuit.

Equilibrium ideology

If there is one key theme that will become etched in your mind after reading Debunking Economics II, it is the idea that equilibrium is not a possible economic condition in reality. Therefore, equilibrium economic models are useless in modelling real life economic systems.

While I agree with Keen, I believe he takes this idea a little too far for my liking. There is value from static comparative analysis for the policy maker interested in the impact of new policies. Treating the economy as a dynamic system provides no way of knowing which changes are policy related, and which are simply products of the system dynamics themselves.

As an exercise in understanding the macro economy, dynamic modelling is highly valuable, and I hope that Keen’s work in this area continues to provide new insights, particularly with respect to developing policy in enhance system stability.

Overlooking the role of money

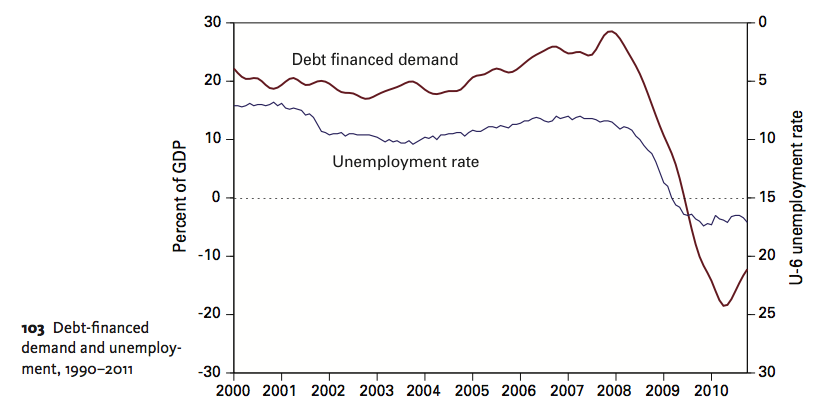

The economics profession in general has a very basic assumption about money. They ignore it. Keen is one of a small group of economists actually examining how the monetary system links with the physical production systems in the economy. Keen explains why the rate of change of new debt (the credit accelerator) is an important macroeconomic indicator, due to the way debt brings forward future demand, creating a current total demand greater than the current productive capacity of the economy. The reverse is true when deleveraging begins, with subsequent impact on employment (as shown below).

Keen’s monetary model also demonstrates that bailing out borrows rather than lenders during credit crunch will be much more effective tool for containing unemployment than bailing out lenders.

One area of Keen’s work I found most intriguing was his analysis of the writings of Karl Marx. Keen takes a pragmatic approach to the classicists, highlighting their constructive contributions to economics, which have stood the test of time and are supported with empirical evidence, and even debunking the often erroneous ideals symptomatic of the era that they are often remembered by. Some ideas really do stand the test of time, as insightful MB reader Lori pointed out recently Marx also wrote that science and knowledge are the most important productive forces in the economy; a principle complexity theorists are now pursuing empirically.

The book left me thinking, if current neoclassical economic theories are so obviously flawed, what will spring up in its place? If I recall, it was Thomas Kuhn, musing over the battle of scientific paradigms, who suggested that evidence does not destroy theories -new theories destroy old theories. With current global economic events as a backdrop, I can’t help feel that a scientific revolution is coming to economics. And if Steve Keen has his way, it will happen sooner rather than later in the form of dynamic systems analysis.

Tips, suggestions, comments and requests to rumplestatskin@gmail.com + follow me on Twitter @rumplestatskin