In this week’s equity spotlight, we take a look at listed investment company Australian Foundation Investment Company (AFIC). Later this week, we’ll also take a look AFIC’s recently-announced convertible note.

The Business

AFIC is a listed investment company that has been investing in Australian equities for over 80 years. They are Australia’s largest listed investment company, with a market capitalisation of approximately $4.5 billion.

According to their website, AFIC aims to “provide shareholders with attractive investment returns through access to a steady stream of fully franked dividends and enhancement of capital invested”. Their goals are:

- to pay dividends which, over time, grow faster than the rate of inflation; and

- to provide attractive total returns over the medium to long term

Judging by their investment list, AFIC looks for dividend-paying, bluechip Aussie shares. Their top 10 investments read like the who’s-who of the ASX: BHP, Woolies, The Big 4 banks, Telstra, Wesfarmers, Rio and Woodside. It appears AFIC really do take a long-term view and are not overly phased by short term market movements. Given their unrealised capital gains tax liability, they also appear to adhere to the buy and hold philosophy.

The Financials

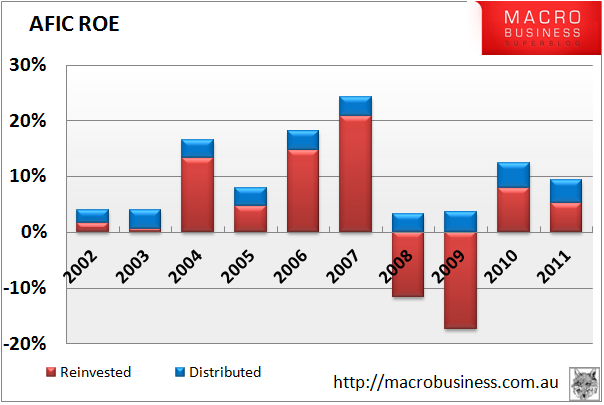

AFICs return on equity (ROE) has ranged between 24% and -13% over the last 10 years. However, those numbers also take into account unrealised changes in their asset base as market prices of their investments fluctuate. This explains the 2008 and 2009 results, when share market prices were depressed following the GFC. Nonetheless, ROE has averaged 7.5% over the last 10 years, rising to 12.1% if 2008 and 2009 are not counted.

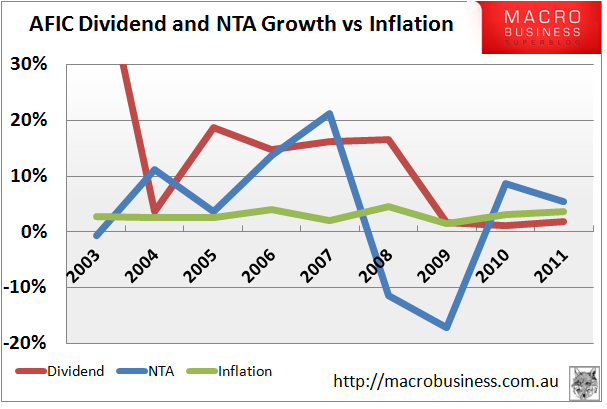

Given their long investing timeframe and propensity to hold onto investments, AFIC’s performance is more accurately reflected in the growth of dividend and net tangible assets (NTA) over time. From the chart below, it appears they have achieved their main goal of growing dividends faster than inflation over the long run. Although the last few years have seen subdued growth.

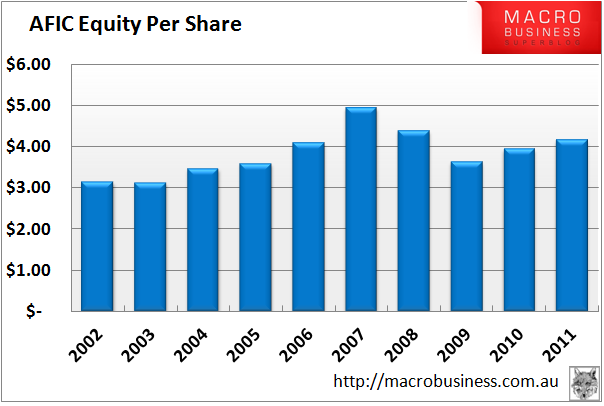

Equity per share has been slowly increasing, with the falls in 2008/2009 matching the drop in NTA growth.

Borrowings have historically been very low – often less than a third of yearly net profit and a miniscule proportion of total assets. On November 15, AFIC announced a convertible note issue that will increase borrowings between $100 and $300 million. Given FY11’s net profit was $233 million, the debt issuance shouldn’t break the bank. In the event things really go pear-shaped for AFIC, they can sell down some of their $4.2 billion dollar asset base to meet the debt obligations.

The notes will be issued to fund general corporate expenses and any investment opportunities that may arise in the future. The coupon rate is a little too close to their average ROE for my liking. If ROE falls below the 6.25% coupon, then the debt raising will be a drag on earnings. I’ll go more into the note issue later this week.

Management

AFIC take the same approach to their management as they do their investing – long term. Company director Bruce Teele has been a director for an astonishing 45 years, with other board members serving +20 years. The board and the executive team have impressive banking and financial backgrounds, with Goldman Sachs and the Big 4 banks showing up constantly in resumes. I wouldn’t expect any scandals or self-implosions from this group.

Given AFICs dividend and NTA growth, as well as a lack of realised capital gains tax, the board appears to have consistently applied a long term approach to their investments. No doubt this is assisted by having the same guy run the place for 45 years. While their returns are not stellar, they have been consistent and grown above inflation on average for at least the last decade – meeting their stated goals.

Risks

- Given their portfolio, AFICs NTA will be closely correlated with the ASX,

- Whilst their long term approach will smooth out income in the short–term, their performance will ultimately be affected by a long-running bear market,

- The recently announced convertible notes will add interest expense to their balance sheet, although small in comparison to current earnings

- The note coupon rate of 6.25% is pretty close to the average return on equity, so the extra debt may be a drag on future earnings.

Opportunities

- AFIC have shown a commitment to long-term investing,

- Dividend income is strong and stable, even during years of poor market performance.

Summary

All-in-all, AFIC meets its mandate of providing dividend income growth over the long term. Although they have average returns, they are consistent and appear to offer a low-risk exposure to the Australian share market. They won’t give you 15% a year, but they should give you something better than inflation without many worries.

Despite their consistency, I still consider AFIC non-investment grade due to their low return on equity. I’m looking for at least 15% ROE (on average) over a 5 year period, and AFIC just won’t provide that sort of return. However, if you’re happy with a 5-10% return, like your franked dividends, don’t mind a slowly growing asset base and are looking for security, then AFIC may just be the ticket.

Valuation

Assuming a normalised (including franking credits) ROE of 9%, an equity per share base of $4.16, a required return of 15% and an assumed reinvestment ratio of 40%, I value AFIC around $3.90.

Disclosure: The author is a Director of a private investment company (Empire Investing Pty Ltd), which has currently has an interest in one of the businesses mentioned in this article. The article is not to be taken as investment advice and the views expressed are opinions only. Readers should seek advice from someone who claims to be qualified before considering allocating capital in any investment.