Several MacroBusiness bloggers have talked about the possibility of share markets entering a period dubbed the “Great Volatility”. This is essentially a secular bear market where prices rise and fall 20‑50% within a year but give low growth (1-2%) on average over the long term. This would be in contrast to the “Great Moderation” – a period of low inflation and low interest rates that occurred in the developed world over the last 20 years. For more information on the Great Volatility, see The Prince’s excellent article on share market valuation.

Invariably, predictions of increased volatility come with warnings about “traders markets” and that long term value investors should stay on the sidelines due to wild price swings. I couldn’t disagree more because volatility creates opportunity for investors and speculators alike; opportunities to buy when the market is depressed and opportunities to sell when the market is irrationally exuberant.

If you decide that you want to be an investor instead of a trader (check out another great article by the Prince on investor psychology here), then to navigate and profit from the “Great Volatility” I believe you will need four things:

- A method of identifying great companies (grading)

- A method of calculating the value of a security (valuing)

- A method of calculating when a security should be sold (selling)

- Courage (discipline)

Grading

Before any thought is given to quantitative valuation of a company’s share price, the value investor has to ask if it’s worth owning at all. Great companies will enter financial crises and emerge lean and meaner on the other side. Poor companies will fold or undergo major restructuring to weather the crisis, possibly emerging as quite different businesses. Bluescope (BSL) is an example of the latter. Despite trading at very low prices recently, a value investor would never invest in Bluescope because their return on equity (ROE) was marginal even during the good times. BSL now faces large headwinds from the high AUD and has recently axed hundreds of jobs – further confirmation that it is not investment-grade.

The ASX is full of companies that Empire Investing consider non-investment grade. In fact, we would stay clear of most of the ASX200 – there’s far more dogs out there than diamonds, with approximately 60 companies making investment grade (the Empire Index).

Valuing

Once a good company is indentified, the valuation tells the investor when to purchase the share. As the market swings wildly, share prices of good companies will fall below what the investor believes they are worth. At this point, the investor has the opportunity to purchase the shares from a depressed market at a significant discount to value.

One famous historical example of this practice is Warren Buffet’s purchase of American Express securities in 1964 after a fraud scandal. Buffet believed the market over-reacted to the scandal and that earnings would not be as affected as the share price indicated. He turned out to be correct – Amex traded well above its 1964 lows only 12 months later. This is a key message with regard to quality and robustness of the underlying business – a sound valuation technique is effectively an indirect hedging strategy against market and economic volatility.

Selling

The determination of a sell price is as equally important as the buy price – especially during times of high volatility. As the market’s mood becomes manic, the astute value investor will sell him the shares of his securities at prices above their value. Whilst the value investor may think highly of the company they have invested in, it’d be a mistake to hang on to any share when it trades well above value. Firstly, prices will tend to reflect fundamental value in the long run- so the share price may stagnate until value catches up or drop to meet the value. Secondly, it’s better to have $X cash in the hand than hold a share that is worth $Y when Y is a lot less than X.

Courage

To combine the above strategies when the market is volatile requires courage and discipline. Most investors get nervous when their portfolios are splashed with red (this one included). However by grading, valuing and determining a sell price the value investor will go a long way towards mitigating losses and realising profits. They just need to have faith in their valuation skills and ensure they take a conservative approach when forecasting future earnings.

A case study – Reece Australia Ltd

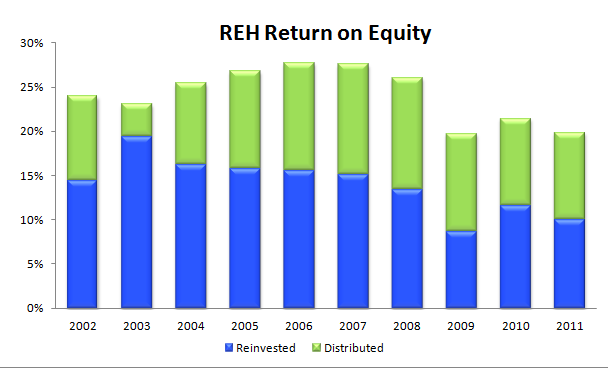

In order to show how this approach could have been applied in the past, I’ve done a little back-testing on one of Empire’s favourite stocks – Reece Australia Ltd (REH). We believe REH is a wonderful company based on its high and stable ROE (see graph), low to no debt, no intangibles assets and dominant market position/brand name.

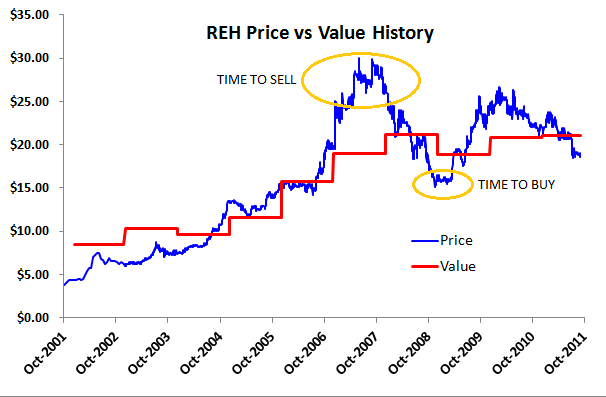

I have calculated the key financial metrics (ROE, equity per share etc) from the last 10 years of annual reports. To determine historical value, I have put myself in the shoes of an investor at the end of each of the year and tried to calculate the value of REH based on only past information. The valuations of Reece versus the historical share price are shown below.

Note: The early 2000’s valuations will be the sketchiest as we often look at 5 years worth of data in an attempt to discern the volatility of earnings. The valuation for years 2001 – 2004 didn’t use data from the mid 90’s onwards, but relied on the figures from 2001 onwards. I also recognise the bias involved in backward-looking valuations, but in lieu of a time machine it’s a valid exercise.

It is clear that the share price of REH shot well ahead of our valuation results in the lead up to the GFC. This confirms the selling strategy – when the market is over exuberant it’s time to offload your shares. At the height of the boom, REH was trading at $30 – which is well any value we would have calculated based on the previous 5 years worth of data. Better to have $30 cash in the hand than own a share you think is worth $20.

Conversely, at the depths of the GFC Reece was trading below our valuation – $15.70 versus a value of about $19. No doubt investing in that climate would have been stressful as share prices plunged, however that’s where courage comes in. It’s easier to sell when you’ve made a fat profit, but very difficult to buy when the rest of the world is selling all shares in sight. A sound investment plan – constructed before having to deal with these real-time events – can assist in developing the required discipline and courage.

Conclusion

The Great Volatility can potentially mean great profits for value investors as long as they have a rigorous approach to grading, valuing and selling shares.

When you hear the phrase “buy and hold is dead”, it’s not a slight on value investors. It’s a slight on blindly buying ASX200 companies with a view to holding them for 10+ years, believing they’ll always go up in the long run. Not everything is worth buying and even the best companies are worth selling if the price is high enough. The value investor needs to understand and implement these principles if they are to make a decent profit – volatility or not.

Disclosure: The author is a Director of a private investment company (Empire Investing Pty Ltd), which has no current interest in the business mentioned in this article. The article is not to be taken as investment advice and the views expressed are opinions only. Readers should seek advice from someone who claims to be qualified before considering allocating capital in any investment.