Australia’s current terms of trade boom is a media darling. This widely quoted statistic has provided a degree of comfort to those who proclaim the robustness of Australia’s economy due to close trade connections with Asia, and China in particular.

Most readers would not be aware that macroeconomic researchers have built up a solid evidence base demonstrating that terms of trade volatility leads to volatile outcomes for output growth and inflation, a lower average rate of growth, and reduced welfare. A temporary income boost from a terms of trade effect has been shown numerous times to be a double-edged sword as the disruptive impact on production patterns filters through the wider economy.

But what is the terms of trade? How is it calculated? Can we better understand the economic impact of this oft-quoted figure by dissecting it into constituent parts? And what policy options exist to deal with the volitility? This post explores these questions in detail and shows that our terms of trade driven income boom is not an excuse for policy makers to do sit on their hands, but is instead an opportune time to implement policies that improve the durability and diversity of the economy.

Let us begin. The terms of trade is a simple enough calculation. It is the ratio of the price index of exports over the price index of imports. Like all price indexes, these are generated by a weighted average of prices in the basket of export goods and import goods. The weighting for these baskets of traded goods is derived from the input-output tables in the National Accounts and revised quarterly.

An increasing terms of trade means that prices for the basket of export goods are increasing more than the price of import goods. We can therefore import more goods for the same amount of exports and maintain a trade balance.

Australia’s export mix in heavily dominated by coal, iron ore, and other primary resource (including agricultural commodities). The Prebisch-Singer Hypothesis suggests that over the long run the price of primary goods declines in proportion to manufactured, or final consumption, goods. In 1998, Hans Singer reiterated the advice to policy makers than stem from historical observations. He warned that countries with exports dominated by primary resources must:

… be prudent even when export prices are temporarily favourable and to guard against currency overvaluation and Dutch Disease, with all the unfavourable impact on the rest of the economy and all the dangers of macroeconomic instability which a sudden boom in a major export sector could imply. They are warned to remember that the outlook for commodity prices is not favourable and that windfalls will tend to be temporary, with the subsequent relapse likely to be greater than the temporary windfall.

Singer’s advice is usually aimed at resource rich developing countries, but it applies equally to any country with a large resource export base.

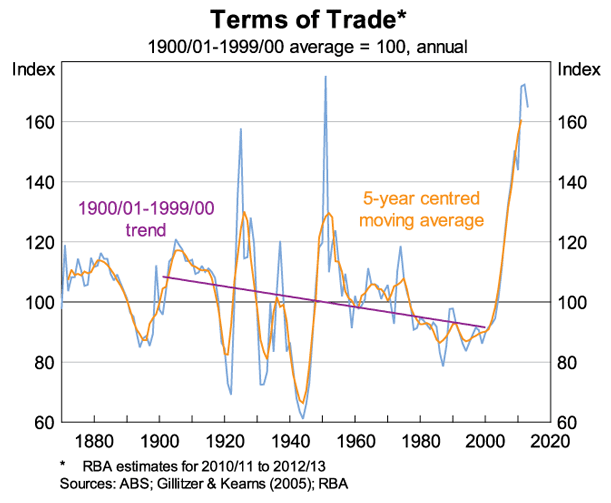

The RBA recently showed this pattern to be true over the 20th century in Australia, with Glenn Stevens himself noting the Prebisch-Singer Hypothesis explains the historical pattern of Australia’s terms of trade:

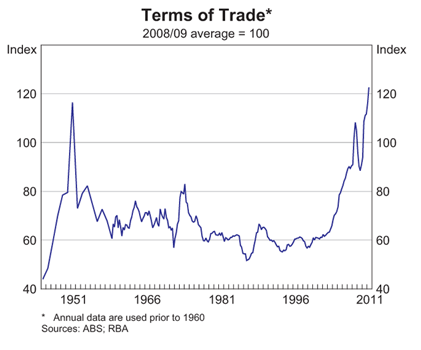

There have been a number of big booms. They all ended. The really high peaks were quite temporary – just one or two observations in this annual time series, such as in the mid 1920s or the early 1950s. Periods of pretty high terms of trade lasted for some years in several instances – as shown by the five-year average – but so far they have all been followed by a return to trend, or even a fall well below trend.

There is also a statistical explanation for the volatility of the terms of trade, particularly when it measure is favourable. Price increases of one commodity lead to increased basket weights for those groups. The basic reason for this problem is that you can’t aggregate tonnes of difference products together – you can only aggregate prices. So if the price goes up its share of exports in terms of price increases. This new share is then used as the weighting of the price change over the next period.

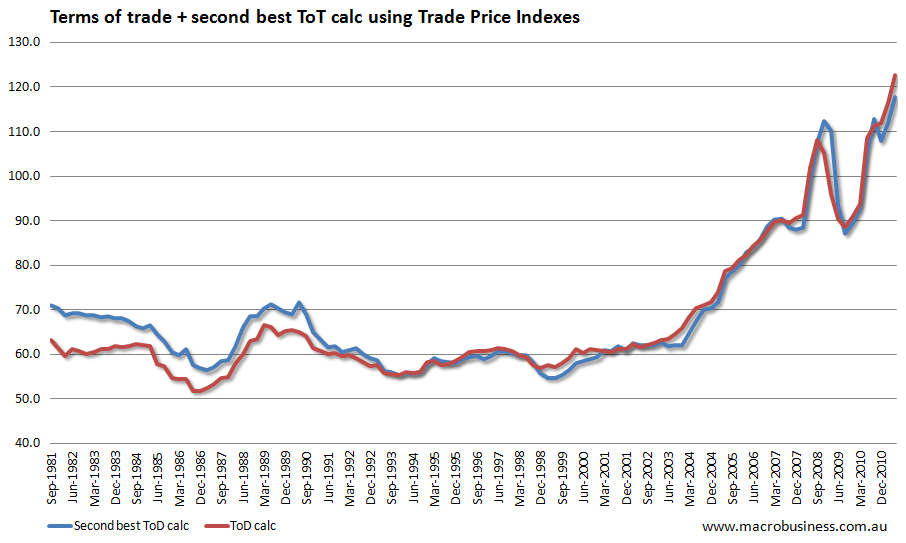

We can see how this has played out in the Australian measure. Unfortunately what we need to do is using a second-best technique that applies the trade price indexes, rather than the indexes derived from the National Accounts. But as the graph below shows, this is a reasonable approximation of the official measure.

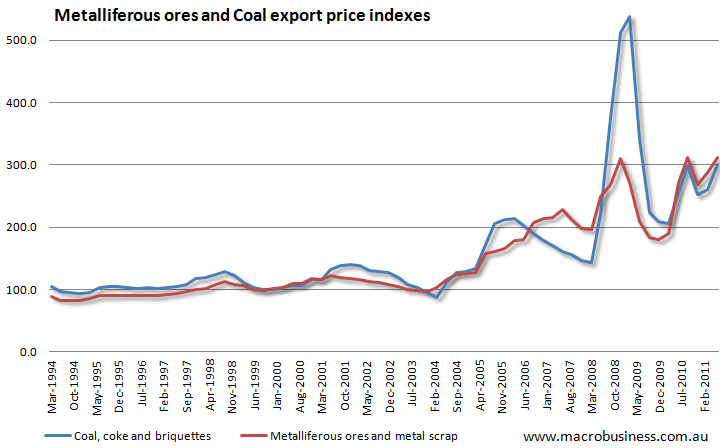

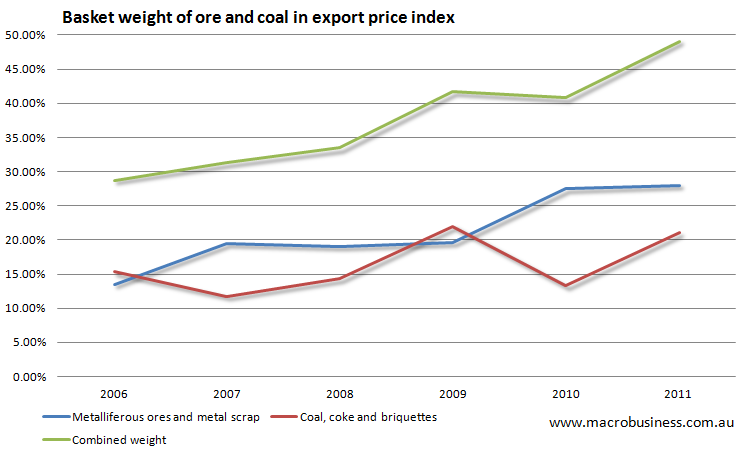

The two graphs below show the pattern of increasing prices and increasing weights to the trade price indexes. The first shows that our two main exports increased in price by 200% since 2004, while the second graph shows that the weighting applied to these two commodities, coal and metal ores, almost doubled to their current 49% share of the export basket weight.

This essentially means is that the higher the terms of trade, the more volatile it will be as the basket of export goods become less diversified. The pattern is easy enough to see when eye-balling the official figures. In the chart below we can see that when the terms of trade is low, say between 1975 and 2000, the volatility is low. When it is a little higher, say between 1960 and 1975, the volatility is a little higher. And when the terms of trade breaks out into the stratosphere, it becomes so taut that relatively small price changes have dramatic effects.

As an example, coal and metal ores price indexes increased 20% between 1996 and 2001 yet the terms of trade was flat (partly due to import prices rising 10%). They also increased in price by 30% between 2006 and now, but the terms of trade almost doubled (while the import price index was flat).

The strong relationship between the value of the Aussie dollar and global commodity prices also results in volatility in the terms of trade. A decline in the dollar will increase the price of imports, while a contemporaneous adjustment in the price of commodities will reduce the price of exports. As a demonstration, a 15% decline in the AUD (in trade weighted terms, which is where the dollar was at in Sept 2009), coupled with a 30% decline in iron ore and coal only, would result in a 30% decline in the terms of trade.

What does this all mean for policy makers looking to promote a stable and prosperous economy? Singer has his view:

Hence the conclusion emphasises the importance of education, development of skills, and of technological capacity. In the light of recent mainstream thinking on growth and trade there is nothing startling about this conclusion

I certainly agree that government should play a role in raising the bar on education and positioning itself as an enabler for new business. I see the NBN as one example of an enabler that is justified on these grounds (despite what you may believe about the opportunities for more cost-effective provision of broadband technology).

Government can also act as an enabler by intervening in the currency market, as the Swiss have done, or even play a role in funding start-up businesses, with favourable lending conditions, especially if they target an export market. Even if the terms of trade soon falls back to historical norms, these are not bad policies to have in place in any case. Remember, volatility itself is a problem.

What the above analysis doesn’t favour is the wait-and-see approach that seems to be the only one on the table at the moment.

Tips, suggestions, comments and requests to rumplestatskin@gmail.com + follow me on Twitter @rumplestatskin