Equities have just finished their worst quarter, in terms of returns, since the dark days of Act 1 of the GFC and the impact of this has been to severly dent Australian dollar sentiment. But even as the dollar teeters on the edge of another cascading fall you’d have to say that the currency is doing much better and holding in well relative to historic context.

We know this statement is correct because we consistently use a my process for evalutaing currencies and in particular the 5 drivers framework for the Australian dollar. We also know it true because the majors are telling me so based on their estimates of “fair value”. Now fair value is a nebulous concept in many ways because by necessity you build a model based on what the key drivers you think are important and see if it fits the history. By definition you are solving for an known outcome which is a bit dangerous when it comes to the future predicitive power of the model. But their are statistical methods to account for this and keep your model updating an evolving.

But even as your model learns, there are often periods of extreme deviation from the implied fair value as markets over shoot. By some estimations the AUS/USD rate over shot to the top side by around 4-5 cents when it rallied to 1.10 twice earlier this year. Presently, the Australian dollar looks like it could still be 5-10 cents over valued.

Writing last week Westpac FX Strategists Richard Franulovich and Jonathan Cavanagh said that their:

Advertisement

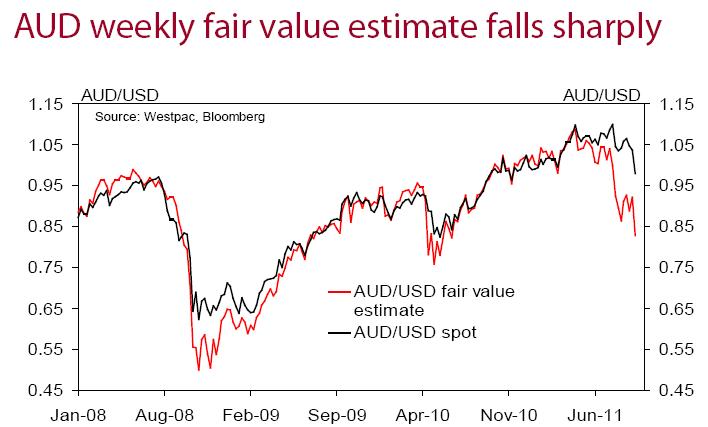

…short term AUD/USD fair value has collapsed to just below 0.85¢ in recent weeks:

Now they note, and you can see in the chart above, that the AUD has been above their fair value estimate since late July and that:

The AUD’s recent sharp fall has unwound some of its overvaluation but the gap between spot and our cross market weekly equilibrium still remains historically large.

Advertisement

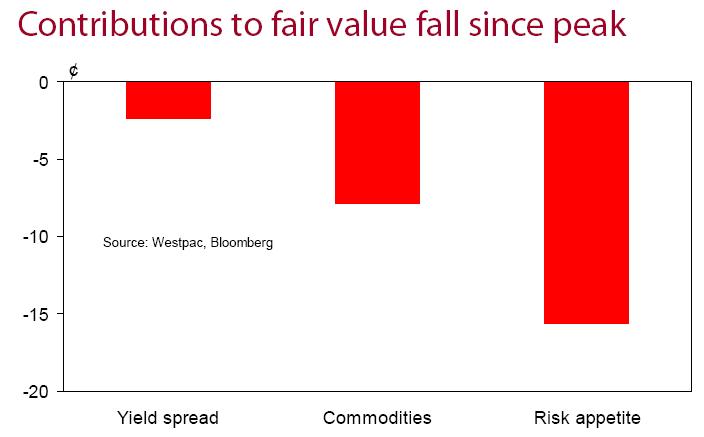

Richard and Jonathan are curious about what has driven the big fall in fair value of 25¢ from the peak in April to now. As such they have performed some attribution analysis of the drivers of the big drop noting that:

3 main drivers of this fall. Lower global risk appetite, as proxied by the VIX, has contributed around 15¢ of this fall, while falling commodities just under 8¢ and declining yield differentials around 2.5¢.

Readers will be familiar with these 3 drivers as key inputs into our 5 drivers model but it is really interesting to me that the Australian dollar is resisting the weak investor sentiment in a manner that is uncommon in recent history. Indeed, I was talking to NAB’s Currency Strategist John Kyriakopoulos last week and he also suggested that the fair value estimate was well below current spot. So why is the Australian Dollar holding up so well?

Advertisement

My guess is that there is some truth in the re-rating discussion that we have had many times. Not safe haven as many call it because that implies the Australian dollar goes up when things in markets go awry and that theory has been comprehensively shown to be bunkum by the recent price action. But certainly in the past I have discussed the possibility that the type of “new’ buyers who have been attracted to the Australian dollar over the past year or so, Central Banks, Sovereign Funds, Family Offices etc. are not short term players who will get spooked by a fall or who have to manage to public benchmarks.

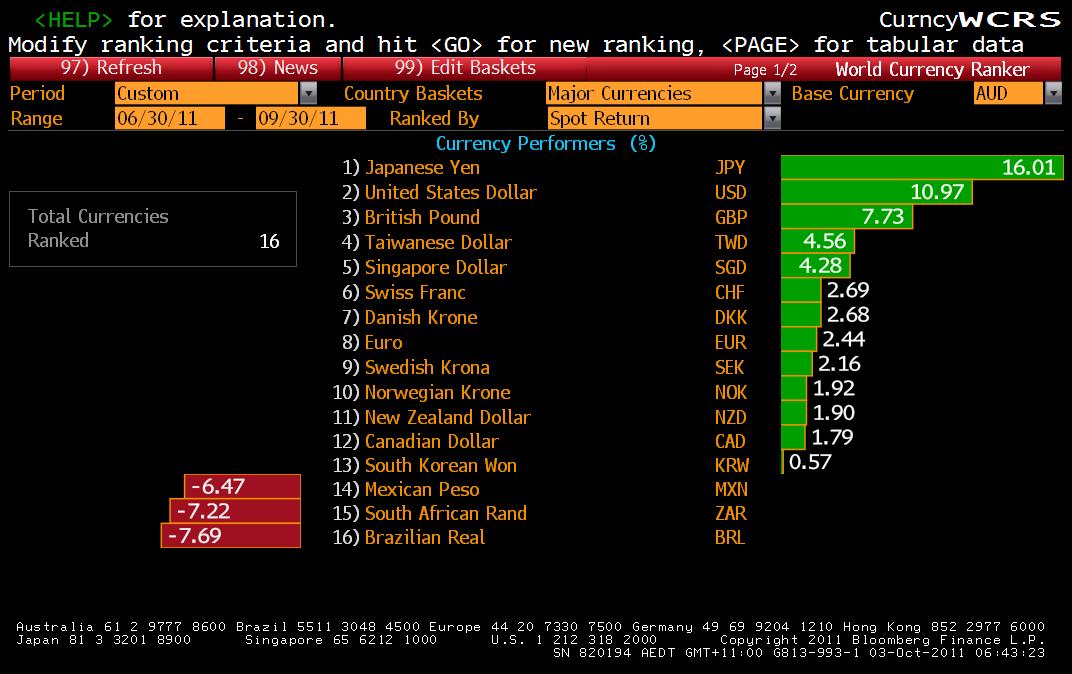

Perhaps there is something in that? But lest we get carried away with the strength of the Australian Dollar and start to give too much credence to the safe haven/rerating thesis, I offer the following table of Q3 2011 relative currency performance of the major traded currencies versus the USD.

Advertisement

As you can see the Australian dollar is the 13th worst performer of 16 currencies with only the “emerging” currencies of Brazil, South Africa and Mexico behind it. Relative returns in Australian dollar terms are below.

So clearly the Australian Dollar is holding in better than expected based on history but still underperforming against most of its peers.

Advertisement

What does this tell me – fairly easy I reckon. The USD has started to rally over the last quarter but safe haven flows into it are not as strong as they once were because it too has problems in this global recessionary environment. So the Australian dollar sits way above fair value because the USD just isn’t performing its usual role with its historic strength.

Looking forward to the week we have some important data in Australia,lead by the RBA Board meeting tomorrow and accompanying statement. I personally think it’s time to drop rates a bit but there is nothing we’ve heard from the RBA recently that suggests to me that they will do it this month. My sense is the statement will be on the dovish side, particulalry after the downgrading of the inflation outlook and the further deterioration in markets and economies world wide recently. Also out are the TD-MI inflation guage today for the month of September and retail sales on the 5th.

In terms of levels, I ink the 0.9600 region is key short term support as I highlighted last week:

Advertisement

Friday’s close was ugly on many levels but unless and until I see a daily break and close below 0.96 I can’t get too beared up,although my overriding medium term view is that the Australian dollar is going to head and test 0.9200/50 eventually. While above 0.9600, however, there is a chance of a rally back toward 0.9790/0.9800 initially, and if through, 0.9960/90.

Please remember these are not recommendations for you to trade these are my views and I have my risk management tools and risk parameters that you do not have access to. Thus, this blog is for information only and does not constitute advice. Neither Greg McKenna nor Lighthouse Securities has taken your personal circumstances, objectives or financial situation into account. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation or needs.