In this week’s equities spotlight, we examine an emerging force in the Australian food retail space – Metcash Ltd.

The Business

The Business

Metcash (MTS) is Australia’s leading wholesale distribution and marketing company specialising in grocery, fresh produce, liquor and hardware. The wholesale distribution networks supplies IGA retailers, various liquor stores and Campbells – a distributor of grocery, general merchandise, confectionery, foodservice and liquor products to small businesses. MTS is emerging as a third major player in the food retail space – shouldering up to the Wooloworths/Coles duopoly.

In March 2010 Metcash acquired a 50.1% stake in the Mitre 10 Group – the second largest Australian hardware retailer. MTS now acts as a wholesale supplier to the independently-owned Mitre 10 retailers. Metcash also acquired the Franklins chain of supermarkets in September 2011 for $215m after overcoming a legal challenge from the ACCC.

Metcash was originally started by Joe David as a family-owned business in 1927. Davids Ltd listed on the ASX in 1994 before being acquired by Metcash Trading Ltd in 2001.

The Finances

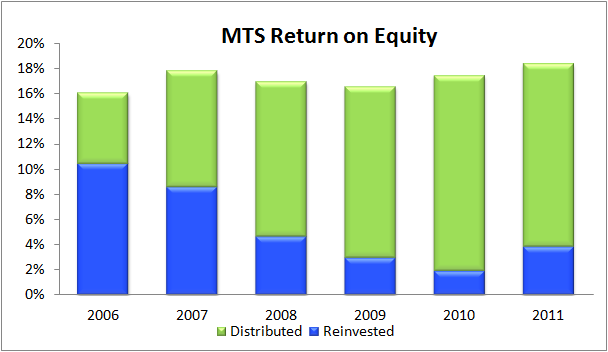

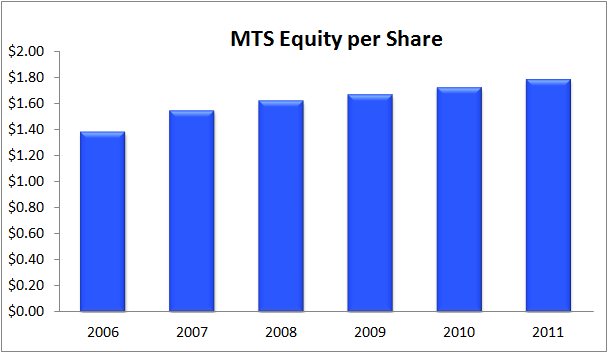

Metcash’s return on equity (ROE) for the last 5 years has averaged 17% and has only varied 1-2% from this average – a welcome trend when trying to judge business value. Equity per share has grown steadily from $1.55 to $1.79, with the only capital injections coming from small share-based payments for employees.

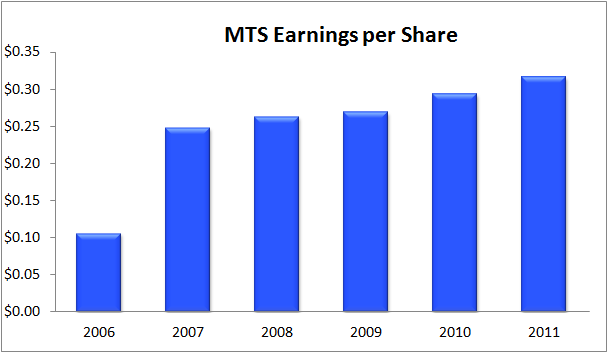

Earnings per share have grown steadily since 2007. The poor 2006 EPS was due to a large capital raising/restructure which added substantially to the equity base.

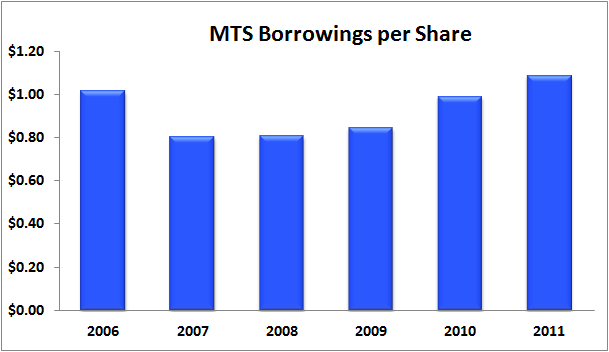

Borrowings are a little high for our liking. Net debt stood at $680m at the end of FY11 versus NPAT of $241. The Franklins acquisition appears to have been funded via debt from US institutional investors, so net debt levels are probably closer to $900m by now. We will be examining the first half FY12 earrings results closely to see if the acquisition has been earnings-accretive enough to justify the increased leverage.

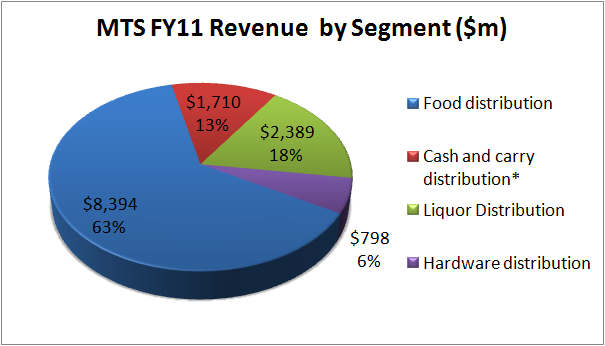

The segment revenue split below shows that food distribution generates the lion’s share of sales.

*The “Cash and Carry” segment relates to the supply of groceries and tobacco via cash and carry warehouses.

Management

The management team appears to have a wealth of retail and wholesale industry. Many members have been with Metcash in one role or another for over 10 years, whilst several bring experience from related outside businesses. The Directors have relatively impressive resumes, with several bringing outside experience from major ASX-listed companies like Telstra and Newscorp.

Management’s goal is to support and promote their independent retail network via MTS’s warehousing and logistics capabilities. They appear to have successfully executed this strategy over the last few years, with steady ROE, increasing market share and manageable debt levels. This is no mean feat given the recent acquisition of Mitre 10 and stiff competition from rivals like Woolworths, Audi and Coles.

Directors and managers can have high proportions of performance-related bonuses – up to 55% of total salary in some cases. However, this proportion seems to vary substantially from year to year, indicating that bonus key performance indicators (KPIs) may actually be set fairly high. The major bonus KPIs are earnings before interest and tax (EBIT) and sales. Unfortunately these two KPIs aren’t overly impacted by debt-fuelled acquisitions, which is a valid concern given the recent leveraged acquisition of Franklins.

Opportunities

- Growing revenues indicate the retailers supplied by Metcash are weathering the downturn in consumer spending,

- The Franklins acquisition increases MTS’s supply chain footprint and provides more retail shopfronts.

Risk

- MTS two main rivals are we part of a large, well-established Australian duopoly,

- The Franklins purchase via debt funding will increase the balance sheet risk if earnings do not increase accordingly,

- The Australian consumer is still paying down debt and being tight-fisted with their discretionary dollars,

- Woolworths has entered the hardware market with its Master stores, which will put pressure on Mitre 10 retailers (who are already facing tough competition from Bunnings).

Summary

Metcash is a solid business with a solid set of numbers. They appear to be growing in an industry that is dominated by two giant established retailers, indicating that MTS is stealing sales from its bigger rivals.

Return on equity is consistent at about 17%, however debt levels will need to be watched after the Franklins acquisition.

Metcash lacks any sort of competitive moat – one could even say that it must combat the duopolistic moats surrounding rivals Woolworths and Coles. As such, we consider MTS a “Good” company with no competitive advantage.

Valuation

Using an equity per share level of $1.79, assuming normalised (including franking credits) ROE of 25% dropping to 21% over 5 years and reinvestment of 15% of NPAT, we value Metcash at $3.45 per share.

Given that we consider Metcash a Good company, we’d be looking for a 40-50% discount to value, giving a buy range of $2.30 to $2.45.

Disclosure: The author is a Director of a private investment company (Empire Investing Pty Ltd), which has no current interest in the business mentioned in this article. The article is not to be taken as investment advice and the views expressed are opinions only. Readers should seek advice from someone who claims to be qualified before considering allocating capital in any investment.