This post explores a simple question. Why do we need foreign investment? The below quote from Mark Mansfield triggered this line of thought.

We do not need foreign investment to develop Australia. We may need to buy technology and skilled labour from overseas, but we do not need foreign investment. Foreign investors cannot spend their $US, Japanese ¥, German DM or £ Sterling, in Australia, they can only spend $AUD. When foreign investors purchase assets in Australia, they need to buy $AUD. They purchase these dollars from Australian banks, or from banks in their own nation holding reserves of $AUD. In effect the banking system releases counterpart $AUD into the economy, on the signal of the foreigner investor. This is totally unnecessary. Why allow an Australian bank to introduce $100m into the economy to start a mine or factory for a foreign company, when $100m of new money could be created for an Australian company to do so.

The official reason for relaxed foreign investment policy on Australia is “to meet the shortfall of domestic savings against domestic investment needs”. Although there was surely international political pressure to conform to the emerging ideology of deregulation at all costs.

But can there really a shortfall of domestic savings given Mansfield’s description, and the fact that bank lending is essentially unrestricted? If Australian banks could create an extra $900billion in the past decade for Australians to buy homes from each other, surely they could have funded a similar amount for productive investments that were instead taken up by foreigners? Remember, the current account deficit has averaged $48billion pa over the past decade, meaning that foreign capital inflows in the capital account (foreign investment), which balance the current account, has totalled around half a trillion dollars over the past decade, or half the amount banks lent to the housing market.

The reason why foreign investment is a concern is that it allows foreign owners to capture economic rents generated from domestic activity. For example, a foreign company buys a block of land on the city outskirts. A new highway is built alongside the block, increasing its value (economic rent) for commercial uses. When the land is now sold at the higher price, or even rented at a higher price, those unearned profits, generated by the taxpayer investment in the highway, head abroad to be spent in the foreign country.

A more relevant example is the mining industry. With historically high prices, rents are accumulating to foreign owners of mines rather than being ‘shared’ across Australia, as would be the case if ownership were purely domestic.

Australia has a long history of foreign investment stemming from colonial times. The beginning of the modern era of direct investment was the establishment of the Foreign Investment Review Board in 1975. In the early days foreign investment was still tightly controlled and subject to restrictions such as complex net economic benefit tests and a preference that Australians were involved on boards of directors, or through employment. The Government also sought Australian equity participation where foreigners wished to invest in mining, agriculture, pastoral, fishing and forestry industries.

The relaxation of foreign investment was a politically sensitive process, with public fears about loss of sovereignty and jobs. These days there is almost unrestricted indirect foreign investment in debt and equities markets, and even the notification thresholds for direct foreign investment appear particularly lenient – at $50million for investment in existing businesses, and $100million for non-residential real estate (although purchases over $50million will be notified but not scrutinised). For notified foreign investment the Treasurer retains discretionary control, as the recent rejection of SGX’s takeover of the ASX demonstrates. This takeover was rejected on the ground of national interest. Of interest are the following five factors set out in government policy on the matter of national interest –

National security – the extent to which foreign investments affect Australia’s ability to protect its strategic and security interests;

Competition – in addition to examination by the Australian Competition & Consumer Commission (the ACCC), the FIRB will examine the effect that foreign investment will have on the diversity of ownership within Australian industries and sectors to promote healthy competition;

Other Federal Government policies – including the impact on Australian tax revenues and environmental objectives;

Impact on the economy and the community – the impact on the general economy, including the following: plans to restructure the target entity, the nature of acquisition funding arrangements, the level of Australian participation in the target entity following the transaction and obtaining a fair return for the Australian people; and

Character of the foreign investor – the extent to which the foreign investor operates on a transparent commercial basis, and is subject to adequate and transparent regulation and supervision. This also includes special considerations in relation to foreign governments and their related entities.

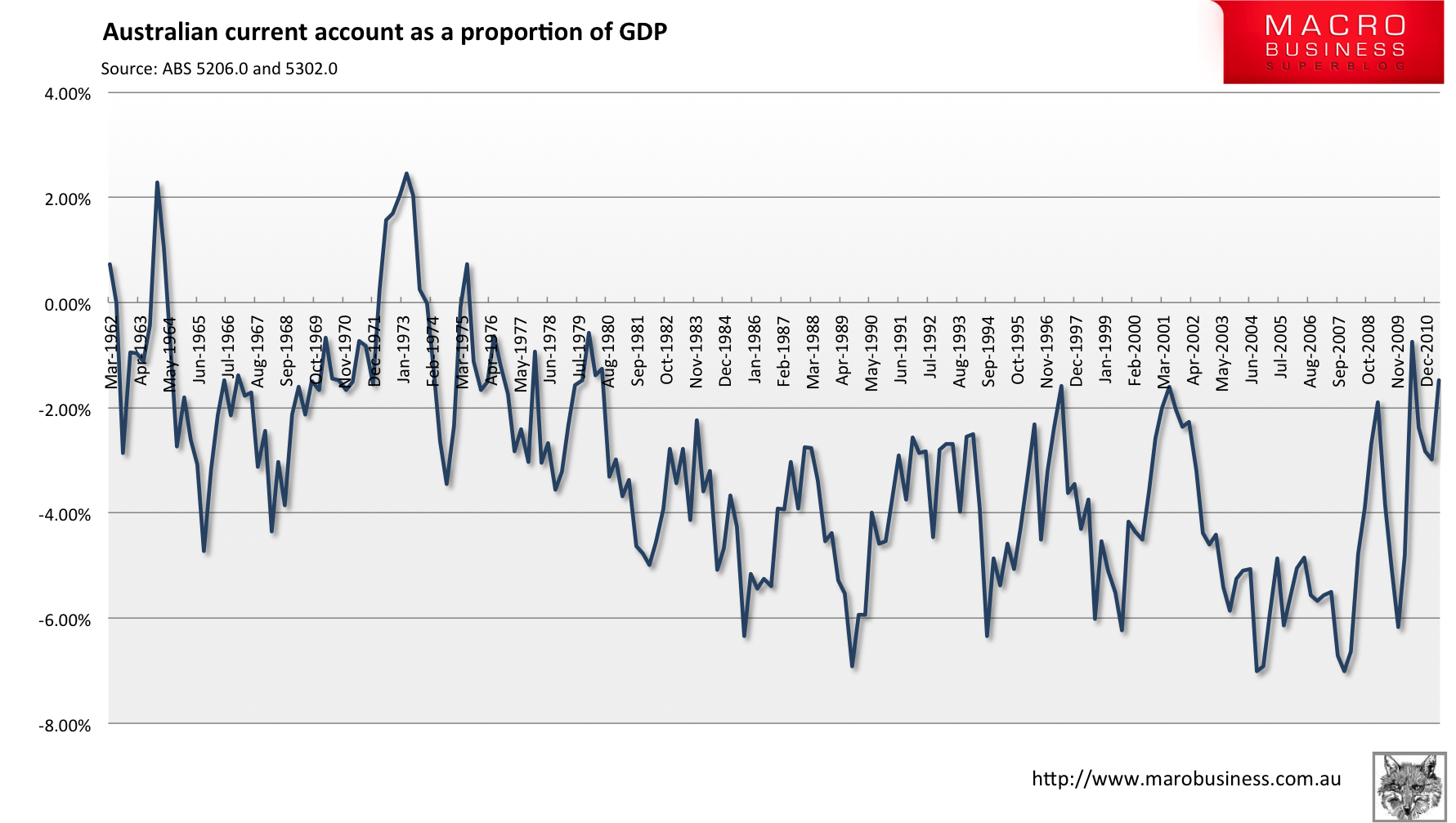

I would be prepared to argue that foreign investment is rarely in the public interest compared to domestic investment. We know our banking system can fund all profitable projects imaginable in the country. And we know that foreign ownership allows the economic rents generated by domestic activity to be taken out of the country. We also know that the current account deficit has become even more entrenched since the deregulation process began. Without foreign investment, either as debt or equity, there can be no current account deficit, and Australia’s current account deficit is not a pretty sight, having grown from an average of 2% of GDP in the two decades prior to 1980, to an average of 5% of GDP in the period since.

So why then do we need foreign investment? My view is that if the government and banking institutions properly understood the functions they perform, we wouldn’t. But I am open to discussions on the matter. Finally I must note that these are long terms issues that typically evolve slowly over time, and as such, any changes to the status quo will also take decades to evolve, unless of course, a crisis allows sudden drastic policy changes.

Tips, suggestions, comments and requests to rumplestatskin@gmail.com + follow me on Twitter@rumplestatskin