The CPI data released this morning was a fantasatic number if the RBA wants to act on the two most important words in their vocabulary currently: “if needed”.

Coming in at 0.6% quarter on quarter (qoq) the headline CPI was right on the money as was the year on year (yoy) out turn of 3.5%. But it was the trimmed mean and weighted median numbers that have set the interest rate bulls and Australian dollar bears running. Both these measures printed 0.3% yoy against expectations of 0.6% to sit at 2.3% and 2.6% repsectively.

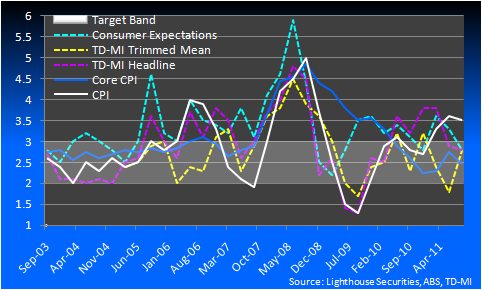

As you can see in the chart above, while the headline level of inlfation might still be stubbornly high the core measure which is the RBA’s favoured measurement is now well and truly back inside the band and actually toward the mid/bottom now. (Please note that due to changes in the way the ABS reports these numbers we need to rebuild our other charts so apologies for only having this one available at this time.)

That being said, the RBA can now confidently and rationally walk away from its recent fear of inflation and thus tightening stance and cut rates in Australia as we have heard recently, and as Ric Battellino reiterated yesterday, “if needed”.

So are cuts needed?

Speaking for myself, my team and the broader MacroBusiness team, I reckon we could comfortably say we have thought that calls for tightenings were way out of the ballpark and that cuts were needed for some time now.

We have written many times about our view on the state of the economy and world and I for one am genuinely concerned about the nascent uptick in unemployment and the still underestimated long term impact of the high Australian dollar and household delevering.

So I answer in the affirmative to the question are cuts needed?

But will they cut on Melbourne cup day?

Given it will be cup day the easy answer is to have a bob each way and say they should, but I dont think they will because they are yet to be convinced of the need. This was writ large in Ric Battellino’s speech yesterday and covered more broadly by Houses and Holes yesterday.

So what do I think?

I’ll come to that in a sec but first lets look at what the early pieces from Westpac, ANZ and NAB have to say.

In its “initial thought” brief publication to clients just now Westpac said:

The RBA has previously stated that “an improved inflation outlook would increase the scope for monetary policy to provide some support to demand, should that prove necessary.” In that context the market has reacted by consolidating near term expectations for an initial rate cut in November and extending the extent of the possible cycle throughout 2012. As at the time of writing there was 125bps factored-in by October 2012, from 100bps prior to the data release.

Westpac has brought forward its long-held RBA policy expectation from a 25bp ease in December to one following the November Board meeting next week, while maintaining a 100bp cycle over the next 12 months.

In a seperate publication Westpac added:

In fact given the Bank’s previous record of moving rates every November for the last five years and given that the case for a rate cut is indisputable the balance of probabilities has now moved to a November cut from our original call of December.

So Westpac is on board for a cut next week. ANZ in their “first impressions” said:

Markedly lower inflation, combined with a still soft employment outlook and uncertain global environment means the RBA has scope to reduce rates by more than 25bps (ie. take rates to an even more ‘neutral’ level) over the next couple of months. Our forecast scenario remains, at this stage, for a 25bps cut in November, followed by another 25bps cut in February.

Tick! ANZ on Board too.

What about my old colleagues at the NAB? They havent mucked around characterising the 0.3% core numbers as “super low” and say that it:

…has tipped the scales in favour of the RBA cutting 25bps on November 1. There is less inflation pressure in the economy than we and the RBA thought only a few months ago and there are downside risks to the medium term forecast. Relevant is that the ABS has revised prior quarters underlying inflation increases to make Q3’s +0.3% not quite as low as it appears – eg the yoy increases of 2.3% for trimmed mean and 2.6% for weighted median average out to near the centre of the RBA’s 2-3% target band. Even so, the Board is likely to conclude they have room to easy policy a little.

So we now have 3 of the big 4 tipping a move next week. But not all! CBA is the hold out:

Clearly the odds on a rate cut next month have gone up a long way. But the policy decision is more complicated than just assessing one number. RBA Deputy Governor Battellino stressed yesterday that the Bank looks at a range of indicators when determining the policy stance. And the key question is whether the economy needs some additional support?

The recent run of domestic data suggests some reasonable economic momentum. There has already been some easing in financial conditions. And the inflation story is unchanged in some important respects:

· The underlying inflation rate has bottomed.

· The headline inflation rate, which is the RBA target variable, is running at 3.5%pa.

· Key upstream price measures have turned up.

· The economy is still close to full employment.

· The economy is still trying to absorb the income boost from a high terms of trade and the stimulus from an unstoppable mining boom.

· Structural inflation pressures are still playing out in areas like rents, utilities, education and insurance services.

· A dismal productivity performance is still pushing up unit labour costs at a rapid rate.

These factors we suspect would make the RBA reluctant to cut rates in normal times. But clearly these are not normal times. The rates call now depends on whether the Europeans can craft a credible rescue package for their financial system. Failure to do so would see the RBA cut rates when it meets next week.

Markets certainly agree with the pricing of cuts over the next 12 months moving from around 100 bps to 120 bps as I write.

Right, so getting back to the question at hand – do I think they are going to cut?

Yes I do. The economy needs a little bit of insurance right now and having tilled the ground its time for the RBA to plant the seed.