They say what gets measured gets managed, but a measure as nebulous as GDP needs careful interpretation when used as a guide for economic management. Putting aside the conceptual problems surrounding the use of GDP as a measure of progress, there is still the practical problem of taking estimates of production or expenditure in current prices and deflating these prices to determine a real change in the volume of good and services produced and consumed between time periods.

What good is GDP at all if we can’t separate price changes from volume changes?

We can get a feel for the challenges of separating price changes from volume changes by examining the way prices are deflated when using the expenditure method to calculate GDP.

* It is worth noting that the ABS has used an integrated and balanced accounting method for GDP calculations since 1994-95, which means that the income, expenditure and production methods for determining GDP must give the same result each quarter.

GDP nominal prices estimates are converted into chain volume measures (real terms) using implicit price deflators for each type of expenditure (consumption, investment and government). The data shows that consumption expenditure is approximately 70% of total GDP, while the household component of consumption is 53% of GDP. Having spent quite some time researching the statistical experiment known as the CPI, some odd patterns have appeared in the relationship between the CPI and the GDP deflators.

The ABS explains that its implicit price deflator for household final consumption expenditure (HFCE) should be somewhat similar to the CPI:

Movements in the chain price index for HFCE are generally very close to movements in the CPI due to the fact that most parts of HFCE are deflated by components of the CPI. However, differences do occur between the two price indexes in some quarters

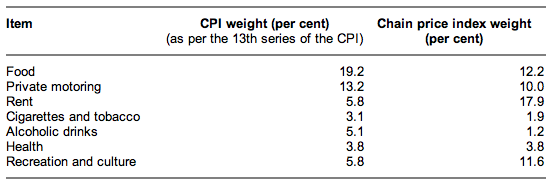

The table below shows the difference in the weights in the CPI and the deflator, which can explain some variation in the short term:

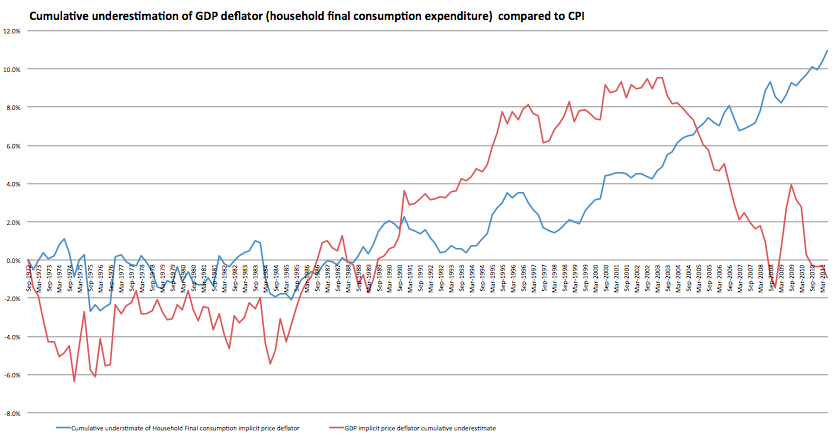

But the data doesn’t seem to support the ABS assertion that the HFCE deflator and CPI will ‘generally be very close’. Below is a chart of the cumulative underestimation of the HFCE implicit price deflator compared to the CPI since 1972. Since about 1993 the GDP deflator has been substantially lower than the CPI and the cumulative difference is now approximately 11%. It is definitely interesting that the variation between these two measures was minimal and corrected quickly prior to the mid 1990s.

The red line is the total GDP deflator (covering all items using the expenditure method), which seems to have recovered its extended discrepancy with CPI since 2003.

This observation leads to questions about the impact on GDP from miscalculation of the deflators. An underestimate of the implicit price deflators for the GDP calculation (treated as positive in the graph) will overestimate real (chain volume) GDP. Since 1997 the household final expenditure component of GDP (around 53%) would have been underestimated by 11%, resulting in a net overestimate of GDP by 5.8%.

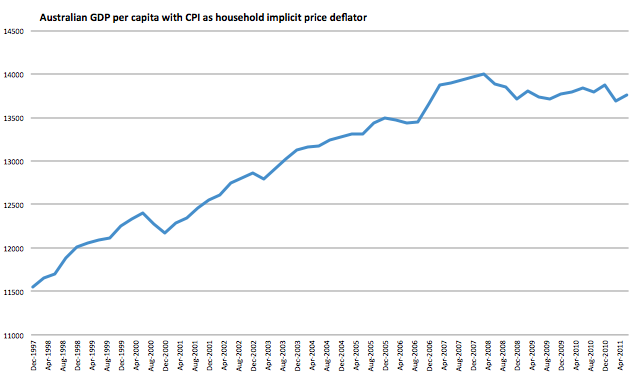

The graph below makes adjustments for the cumulative overestimation of GDP since the late 1990s, and from this new measure is appears that GDP per capita is back at a level first seen in 2006. This gives a slightly different picture to the one in yesterdays Chart of the day showing GDP per capita at 2008 levels.

This analysis does not mean that the ABS has their methods all wrong. Indeed, there may be other biases that more than cancel out this single bias resulting in an underestimated GDP. But it does show that the GDP figure is a product of the assumptions and methods used. It should also raise the question of just how much of the measured economic growth over the past decade was tangible, and how much was simply the result of measurement methods. Historically the CPI and HFCE deflator diverged by small margins for a short periods, so the divergence over the past 15 years appears unique. Whether this pattern will correct and we will see a period of underestimation of GDP I am not sure.

The lesson here is that all economic measurement has bias. Tread carefully.