As regular readers would know, the debate continues about the role of planning regulations on housing supply and the resulting price implications. Yesterday our favourite Unconventional Economist elaborated his views in an exploration of town planning and the UK housing market, so I feel it is an opportune time to elaborate the opposing argument – why the supply side has not been factor in determining the price level of Australian housing.

First, I need to outline exactly how I understand the subtle argument about how zoning and approvals processes can lead to unresponsive housing supply due to time lags, consequently increasing price volatility. This is clearly a far different proposition to the ‘chronic undersupply’ arguments of many housing ‘experts’.

I understand the unresponsive supply mechanism could work to create price impacts as follows.

- If planning regimes restricted the ability to develop housing at a rate commensurate with demand in a given period, through zoning or lengthy development approvals, this would effectively act as a short term quota.

- If rational buyers expect this shortfall to be somewhat prolonged (say 3-5 years) they may be willing to bid up prices in expectation of capturing abnormal rental gains during that time.

- Speculative buyers enter the market based on the new price path, creating a feedback of higher demand. This amplifies the house price appreciation justified by the short term planning restrictions.

- Developers overcompensate for these price feedbacks by bringing on too many homes after the price spiral has run its course (by taking on higher risks such as reducing the number of pre-sales).

To me the mechanism appears sound. But remember, it relies on three crucial factors – irrational buyers bidding up home prices beyond what is justified by any short term lag in supply, developers making the same misjudgements about genuine demand, and most critically, planning instruments and approvals processes acting as a short term quota.

While I don’t disagree that buyers and developers can be irrational, I argue that the final critical assumption cannot be demonstrated to be widespread in Australia (although particular locations may see these short term effects from time to time).

Costly and time-consuming development approvals are often argued to be equivalent to delays in the ability to supply new housing (or land supply in the case of residential land subdivisions). But this lead time is no different from the lead time involved in any complex manufacturing task. Just because it may take two years to manufacture a Boeing 747 does not automatically lead to the conclusion that supply will be restricted in the mean time.

The process for approving development applications (where they are required) can be imagined to be much like a simplified Boeing 747 production line. There are planes sitting in the production line at various stages of completion as well as a stock of completed planes (although in reality planes are usually sold before they are produced – in much the same way the developers pre-sell apartments off the plan prior to construction). Only if the stock of completed planes falls to zero does it mean that the supply has not been adequate to respond to demand, effectively creating a short term quota on production until such time as the production line can adapt to increase output levels.

The property industry has a term for this production line of development approvals – the supply pipeline. Large developers usually research the supply pipeline in their markets prior to buying development sites, and prior to beginning the approvals process themselves. It helps give an idea of the type and quantity of developments they are likely to compete with, which helps better position their product in the marketplace.

For the unresponsive supply side argument to hold, we would need evidence that the stock of approved residential land and apartment sites was insufficient to cope with the spikes in demand, particularly over the past decade.

The best data I can find is for Queensland, where the Office of Economic and Statistical Research (OESR) reports regularly on the residential development pipeline. The OESR compiles a selection of reports about the stock of dwellings of different types at various stages of the approvals pipeline.

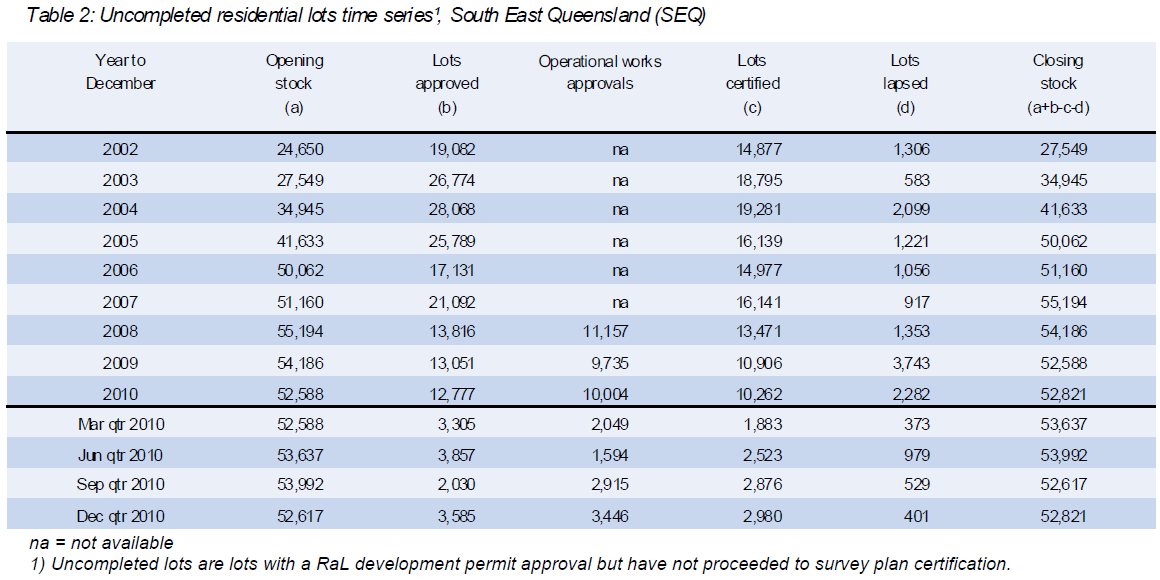

The table below, from this report, shows the completed stock of approved residential land subdivisions at the end of the supply pipeline for South East Queensland. The important thing to note is that this stock has been growing since 2002, with a peak in 2007, meaning that the various councils in SEQ approved far more land subdivisions than the market could absorb. Remember, this is already approved land subdivisions only.

A second important point to note is just how quickly council can ramp up the volume of approvals when necessary, as seen between 2002 and 2005, and again in 2007.

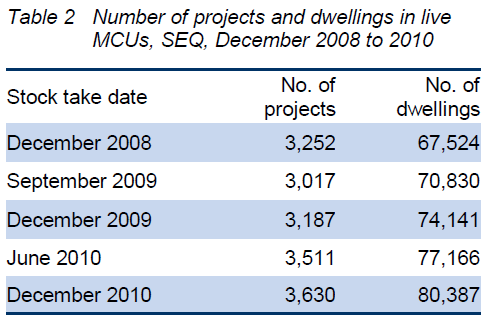

The same pattern holds for the stock of approved infill attached dwellings in the available data since 2008, as shown in the table below (from here).

What are we to make of this evidence?

First, I would argue that town planning controls, in the form of zoning restrictions, urban growth boundaries, have had almost no impact on the price of housing in SEQ over the past decade, and unless there is evidence to the contrary, the same is likely to apply to other capital cities and metropolitan areas.

Second, I would argue that such evidence would not only need to be found in the development approvals data, but in the data for rents in the areas where supply restrictions are suspected. After all, land prices are simply capitalised rents.

Third, I would argue that the benefits from urban growth boundaries, zoning, and other planning rules mostly outweigh the costs. And indeed, these costs are borne by existing owners of developable land, not developers or new home buyers.

Fourth, while planning controls do have benefits, I would be very keen to see more certainty around the planning rules to take away any advantages gained by speculating on future changes to planning rules.

Tips, suggestions, comments and requests to rumplestatskin@gmail.com