Seek (SEK) released its 2011 results recently. At Empire Seek has been one of our favourite stocks – a near-wonderful business with good ROE, great branding, total dominance in the Australian and NZ online employment market with a strategy for diversifying revenues through international acquisitions. Only through lack of a deep competitive moat did it not make the Wonderful grade. Internet businesses are fast moving and their customers fickle, after all.

Seek (SEK) released its 2011 results recently. At Empire Seek has been one of our favourite stocks – a near-wonderful business with good ROE, great branding, total dominance in the Australian and NZ online employment market with a strategy for diversifying revenues through international acquisitions. Only through lack of a deep competitive moat did it not make the Wonderful grade. Internet businesses are fast moving and their customers fickle, after all.

Key Figures

- Net profit after tax (NPAT) of $97.7m – a 9% increase on FY10,

- Increase in operating revenues of 23%

- Online employment EDITDA up 43% to $134m

- Seek Learning division EBITDA dropped 22% to $13.1m

- Think division posted a $7.5m loss

- Five of the 6 international interest posted profits, bringing international NPAT to $16.9m

- Seeks owners equity (i.e. not including non-controlled interests) actually decreased by 12% to $311m as a result of the a $50m put option arrangement entered into with their Hong Kong subsidiary

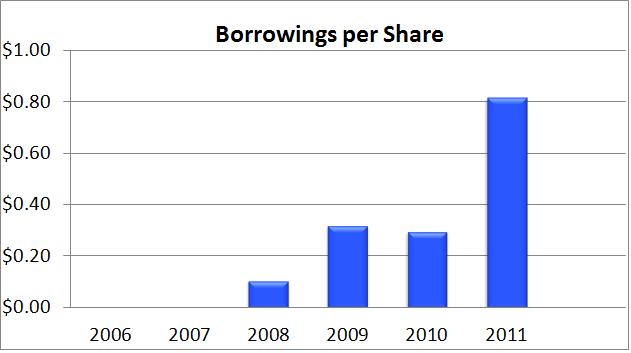

- Debt ballooned from $99m to $275m – an increase of 176%, or more than 2.5 times

Key Calculations

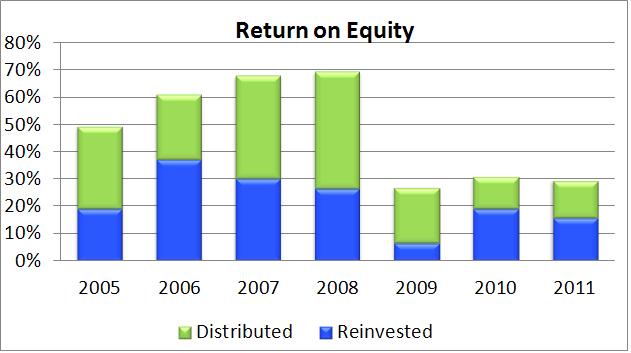

- Return on equity (ROE) was 29.7%,

- Earnings per share $0.29

- Net tangible assets per share -$0.45

- due to debt being taken out in late FY11 for the purchase of another international interest in July 2011, so NTA should now being positive again

- Intangible assets per share $1.38

- Borrowings per share $0.82 – a huge 176% increase on FY10

- Drops to $0.53 per share when $98m in cash and equivalent is subtracted from borrowings

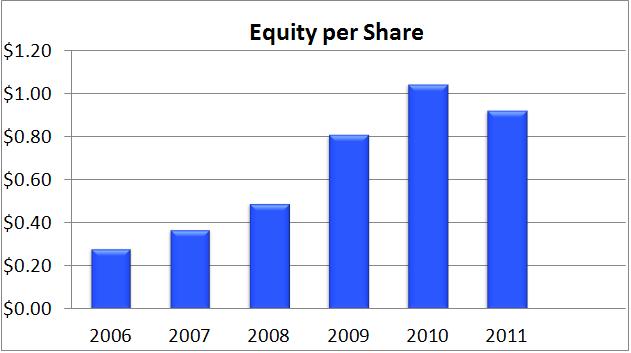

Some of the key calculated metric histories are shown below.

Summary

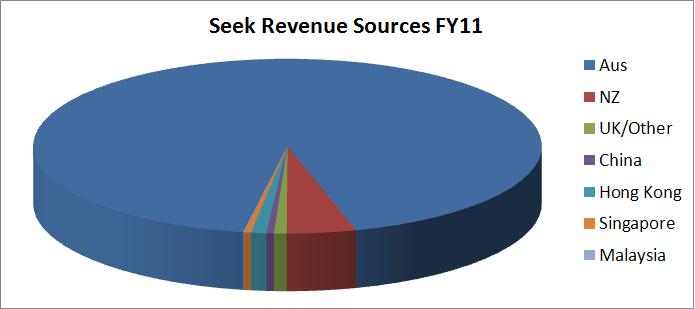

Seek continues to perform well with its bread-and-butter online employment business. It is still by far the most dominant online jobs advertiser in Australia and New Zealand. As the chart below shows, this is also Seeks most dominant revenue source by a wide margin.

The education divisions (Think and Learning, both providers of vocational training services) have struggled this year, however Seeks international purchases in Asia and the Americas are starting to bear fruit, albeit small bananas compared to Australian and NZ employment revenues.

Of greatest concern is the very large increase in Seek’s debt levels in FY11. As of the end of FY11, Seek was carrying $290m in debt, with interest rates ranging between 6.2% and 7.6%. That means Seek is paying some $40m in interest per annum. Whilst this is by no means excessive in corporate Australia, it has elevated the balance sheet risk substantially compared to FY10. Net debt currently stands at $177m, which can be covered by approximately two years’ worth of NPAT at FY11 levels.

Future headwinds

Despite its overseas interests, the majority of Seeks revenue comes from Australia. So the Aussie jobs market will determine the fate of Seeks profits. There has been a lot of coverage here at MB on the outlook for the Australian economy, which most bloggers believe is not rosy outside the mine pit (I concur).

High private debt loads and an uncertain global economic environment have lead to a tight-fisted consumer. This has hurt the feelings of Gerry Harvey and the rest of our retail and services sectors, which employ a large proportion of our population. Any rise in Australian unemployment is likely to impact both Seek’s profits and share price negatively.

Valuation

Unfortunately Seek is no longer our golden-boy internet stock. A heavier debt load has tarnished its image whilst a negative outlook on employment has made us more conservative.

Subsequently, we have downgraded Seek from “Very Good” to “Good”. This also means an increase in our margin of safety at purchase due to the reduced robustness of earnings potentials. It’ll take a reduction in debt levels, better Aussie employment indicators and some sort of improvement in the US/EU saga before we look at reinstating its prior status.

Assuming an updated (after adding the $49.7m in equity for the post-FY11 acquisition of JobsDB) equity per share level of $1.10, normalised ROE of 35% (falling to 25% over 5 years) and a reinvestment ratio of 40%, we now value Seek at $5.00.

Give our rating of “Good”, we would only consider buying below a share price of $3.50.

In my previous equities spotlight article I valued Seek at $7.70, which is a far cry from the $5 bucks stated above. The big drop is due to a lower ROE assumption and our more pessimistic market outlook. Basically, we were too optimistic several months ago. Since that time Seek’s debt has increased substantially and the global outlook has soured.

Nothing is certain in investing, no valuation is perfect, and when the facts change so do our valuations. It is for these reasons we attach generous margins of safety to our valuations. As should all value investors.

Disclosure: The author is a Director of a private investment company (Empire Investing Pty Ltd), which has no current interest in the businesses mentioned in this article. The article is not to be taken as investment advice and the views expressed are opinions only. Readers should seek advice from someone who claims to be qualified before considering allocating capital in any investment.