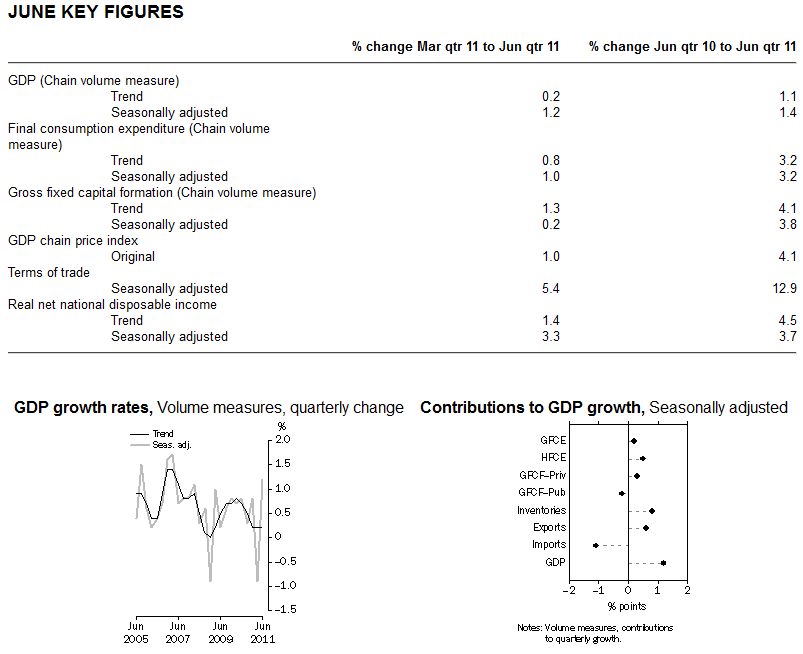

The ABS released their National Accounts aggregates today, with a broad surge in GDP growth since the dismal natural disaster-affected first quarter. The key figures are below.

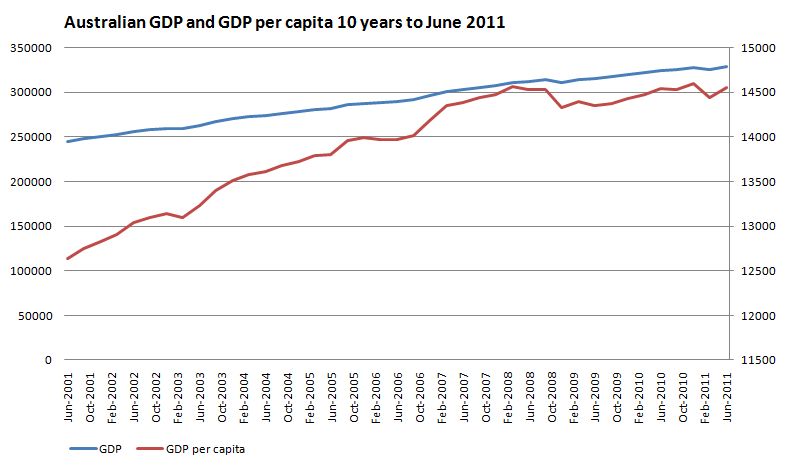

Also important is the revision to the March quarter – up from -1.1% to -0.9%, leaving GDP up 1.38% over the year to June, and per capita GDP flat over the year (up 0.08).

GDP per capita has now recovered to a point first reached in March 2008.

The other interesting notes from the release were the positive contributions of inventories (adding 0.8 percentage points) and consumption expenditure (0.7 percentage points) to GDP growth. While net exports contributed -0.5 percentage points, which is quite a change from the previous quarter.

The household saving ratio declined a little from 11.7% to 10.5%:

Household income was up 2.9% in the quarter and 7.6% over the year. So, roughly 4% in real terms. It’s difficult to know how much of this result is arising from expanding households but stalled GDP per capita suggests we are not shifting to the good times as fast as this figure suggests.

Of course, the question on everyone’s lips is where to from here? Will we, as many suggest, improve on this quarter going into the second half of 2011, or will we continue the relatively flat trend seen over the three years?