With the recent News of the World scandal and the Australian media inquiry it has prompted, today we’ll take a look at the media empire at the centre of it all – Newscorp.

The Business

Newscorp is a global, diversified media company which operates in the following areas:

- Cable Network Programming,

- Filmed Entertainment

- Television

- Direct Broadcast Satellite Television (distribution of basic and premium programming services via satellite)

- Publishing

- Other assorted digital media properties and advertising businesses

Newscorp is best known as the owner of the FOX broadcasting company in the USA and publisher of the Wall Street Journal, whilst closer to home NWS owns approximately 146 Australian newspapers including the national masthead “The Australian”. Newscorp was recently embroiled in the News of the World scandal – a now-defunct UK newspaper which allegedly used unethical and illegal investigative practices, such as phone hacking, to obtain information for stories.

The Financials

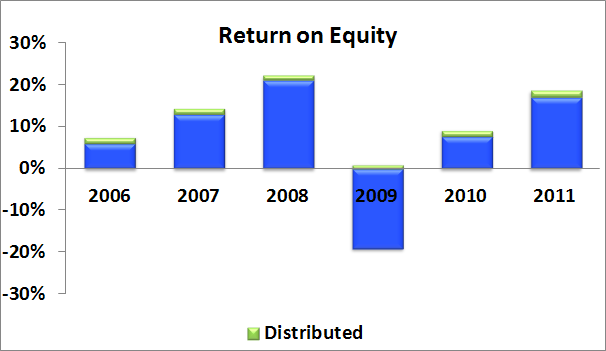

Newscorp’s return on equity (ROE) over the last 5 years have been volatile, ranging from -20% to +20%. The 20% loss was made during FY2009, when some $8b of impairment charges were recognised as a result of decreased intangible values and a loss of goodwill. These losses were driven by decreased earnings and the high prices of past acquisitions. The recent sale of MySpace for a fraction its purchase price is a more recent example of over-exuberant purchases.

Total interest bearing debt of $14.5b is very high compared to FY11 NPAT of $2.8b, however total

cash and equivalents of $12.7b makes net debt relatively low. Intangible assets are very high – $8.86 per share compared to tangible assets of $2.37 and earnings per share of $1.79. Although an argument can be made for high intangibles in media companies (especially publishing brand names), the low earnings return indicates some of NWS’ s goodwill and intangible assets may be overvalued.

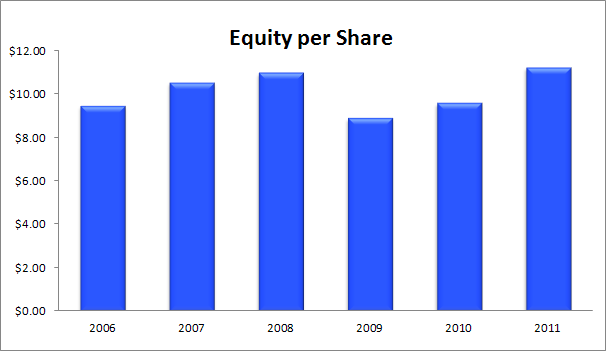

Equity per share has fluctuated between $8.80 and $11.23, taking a hit in FY09 due to the -20$ ROE.

The current dividend yield is around 1.1% – which is even less inspiring when you lok at the equity per share growth and realise NWS does not frank its dividends.

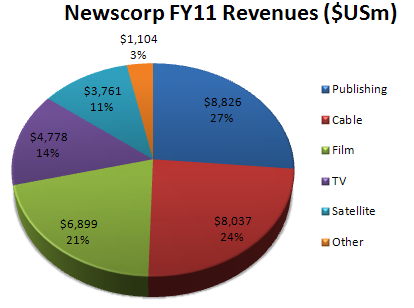

The revenue contributions for each business segment are shown below.

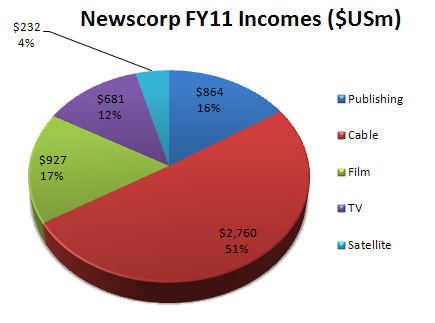

However, the segment incomes paint a very different story:

Cable appears to be the the most profitable business segment – contributing 51% of income in FY11 at a margin of 34% despite only making up 24% of revenues. Television and film are next most profitable, wth margins of 14% and 13% respectively. Publishing appears to be the least-profitable segment, with a margin of about 10% even though it is the largest revenue generator. These margin trends have been consistent over the last few years.

Management

Newscorp’s CEO and chariman is as famous as the company itself. The 80 year old, Australian-born Rupert Murdoch has been at the helm since inheriting News Limited from his father in 1953. Over several decades he expanded News Limited from an Australian publishing company into the second largest media conglomerate in the world. It is rumoured his successor will be Chase Carey – current COO of Newscorp who has had a long association with FOX and NWS. Two of Murdoch’s sons serve on the NWS board (James and Lachlan). The remainder of the board appear to service specialist roles for each segment, with well-known Aussie Rod Eddington also filling a board seat.

Recent ROE volatility and impairment writedowns indicate management is struggling with the digital revolution (see below).

In terms of salary benefits, equity-based remuneration for executive management typically has 4 years vesting and is dependent upon segment profit goals. At the executive director level, equity compensation is based on a 3-year performance timeframes.

The Digital Revolution

Over the last few years NWS management have struggled to come to terms with the online digital revolution; but so have most traditional media companies. The purchase of Myspace in 2005 for $850m shows management are trying to adjust to the new online environment. However, that turned out to be the wrong horse to back as Facebook overtook Myspace as the most popular social network site. Newscorp subsequently sold Myspace in 2011 for a paltry $35m. In all fairness, at the time of purchase Myspace appeared to be the more popular site and it would have been a brave call to say FaceBook would be the ultimate social media winner. Nonetheless, the episode was a lesson in the fast-moving and fickle environment of online media.

All print media companies are facing the challenge of dwindling ad revenues whilst still trying to maintain (i.e. pay for) a decent journalistic standard. NWS is currently erecting paywalls around some of their premium online news sites (e.g. The Wall Street Journal) in an attempt to extract revenue for what they deem excellent journalistic services. NWS claims that the journal subscriptions are increasing, however the success of paywalls on news sites is yet to be determined – especially given the emergence of independent bloggers that typically provides news and analysis for free.

The more successful film and TV segments are also facing challenges as peer-to-peer file sharing increases and pirated films and TV series proliferate. Whilst the margins of these segments appear healthy, they too will face long-term challenges as the world goes online and bandwidths increase to allow fast and easy streaming of all media content.

Risks

- High intangible assets compared to earnings increase the likelihood of future impairment charges during challenging years

- Internal disputes amongst the Murdoch family may sour succession planning

- Further brand name damage via the News of the World scandal

- Possible legislative or regulatory impositions arising from the News of the World scandal or the impending Australian media inquiry

- The inexorable trend of advertising revenue moving form print to online media and the risks associated with online paywalls

Opportunities

- NWS is a diversified, global media company that has significant political clout via it’s market dominance and the reputation of its chairman (also a risk in terms of making it a target for politicians and activists)

- Proliferation of Ipads and tablet devices may assist in the paywall concept for online news sites

- Recent strength in film and TV divisions (Avatar, X-men movie) shows hope for non-print divisions

Summary

Newscorp is a global media behemoth with a long serving CEO who wields considerable influence in the global media landscape. Nonetheless, NWS is facing serious challenges as the world embraces the online future – a future of low overheads, scattered consumer interest, free flowing information and numerous niche content providers.

NWS is attempting to this adapt to this evolving and fluid environment, however recent impairment write downs do not bode well for the current high levels of intangible assets on the books. NWS also has the legacy of a large print division that is now the worst-performing segment (by margin) but generates the largest revenue share – not good for ROE.

At Empire Investing we consider NWS non-investment grade due to the ROE volatility, the high level of intangible assets and the regulatory and macro challenges mentioned above.

Valuation

Assuming an equity per share level of $11.23, an average ROE of 12.5% and a reinvestment ratio of 80%, we value NWS at $12.10 per share. We do not consider NWS investment grade, so we do not calculate a maximum buy price.

Disclosure: The author is a Director of a private investment company (Empire Investing Pty Ltd), which has no current interest in the business mentioned in this article. The article is not to be taken as investment advice and the views expressed are opinions only. Readers should seek advice from someone who claims to be qualified before considering allocating capital in any investment