![]() Following on from Monday’s post on high-yield dividend stocks, today we take a quick look at Infomedia Ltd (IFM).

Following on from Monday’s post on high-yield dividend stocks, today we take a quick look at Infomedia Ltd (IFM).

Note: I haven’t done my usual job of thoroughly examining the last 5 years of financial data (time constraints of my full-time job), so I’ll be relying on equity, NPAT and assets figures from a proprietary, 3rd-party source.

The Business

According to the IFM website,

Infomedia’s electronic parts selling systems have become the global standard for the automotive industry, used by more than 57,000 users in over 160 countries and 34 languages.

In 2000, Infomedia acquired Datateck Publishing Pty Ltd, a data management company, resulting in an immediate broadening of the Infomedia product and service range. Since then, the Company has worked steadily on both consolidating its position as an electronic parts catalogue provider of choice for the global automotive industry, as well as exploring opportunities in other complex parts and service dependent industries.

IFM’s main product is Microcat Live – a microsot.net-based tool that enables the service staff of vehicle dealers to swiftly and accurately find replacement parts. Major clients of IFM include Kia Europe, Toyota Australia and Mexico, Honda Australia, Jaguar, Land Rover and Ford.

Infomedia is headquartered in Sydney with support centres in Australia, Europe, Japan, Latin America and North America.

The Financials

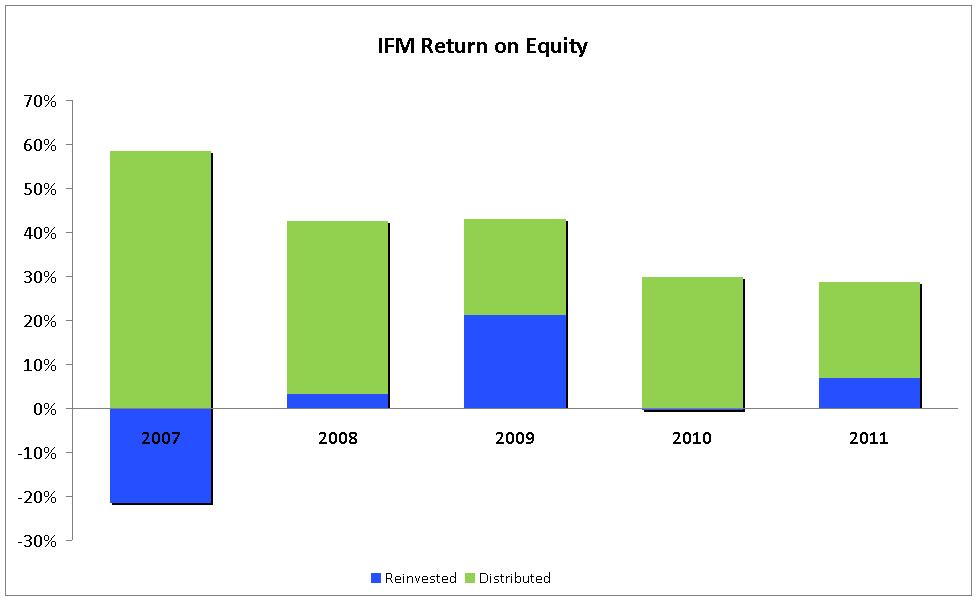

IFM’s return on equity has ranged between 36% and 26% over the last 5 years, with NPAT showing a worrying downtrend over the same period ($15.3m to $9.3m). This has occurred despite share buy backs in FY08, ’09 and ’10, which should act to increase ROE if profits were being maintained. Not a good sign.

IFM is currently debt free. According to Commsec equity has hovered between $0.08 and $0.14 per share for a decade, sitting at $0.11 as of Jun 2010. Intangibles are currently estimated at $0.10 per share compared to tangibles of $0.02, however earnings are only $0.04 per share. Given the decreasing NPAT trend, one should question whether the intangible assets represent fair value.

Management

A quick glance at the 2010 annual report shows little in the way of director histories. Corporate experience outside IFM seems to be concentrated in two directors, who have held executive and non-executive positions in Cash Converters, Itx Group and a few financial companies. Board tenure is quite long, with most members in their roles since the late nineties and early noughties.

Salary makes up the majority of all key personnel remuneration, with bonuses typically making up 15% or less of total packages. Internal management ownership of IFM is negligible.

Management have a history of paying dividends in excess of profits (as seen in the preceding ROE graph in 2007). In our opinion this is a sign of poor capital management.

Opportunities

- Diversified client base

- Widely-accpeted product

Risks

- Foreign exchange movements, particularly the elevated AUD

- Downturn in automotive industry as Western economies enter a period of low demand

- Decreasing NPAT and questionable capital management decisions

Summary

Infomedia is a classic example of a high-yield dividend stock that requires closer scrutiny. Despite its inclusion in my article on Monday, a fundamental value investor should be wary of a stock with volatile ROE, high intangibles and questionable capital management practices. Throw in the macroeconomic factors of exchange rate movements and a possible downturn in Western consumer demand, and IFM suddenly looks less like a safe dividend stock and more like a company facing serious challenges.

At Empire Investing we’d consider Infomedia non-investment grade.

Valuation

Assuming normalised ROE (including franking credits) drops from 30% to 20% over the next 5 years, with 10% reinvested and a current equity per share level of $0.12, Empire would value IFM at $0.20 per share.

As we do not consider IFM investment-worthy, we would not recommend a maximum buy price.

Disclosure: The author is a Director of a private investment company (Empire Investing Pty Ltd), which has no current interest in the businesses mentioned in this article. The article is not to be taken as investment advice and the views expressed are opinions only. Readers should seek advice from someone who claims to be qualified before considering allocating capital in any investment.