There is no denying that the AUD, when it wants to, is a volatile beast, when the buyers clear out it simply crashes. Yesterday was a case in point and while the AUD was clearly crashing with other risk assets there was definately a buyers strike after whoever was defending 1.00 (potentially the RBA) stepped away.

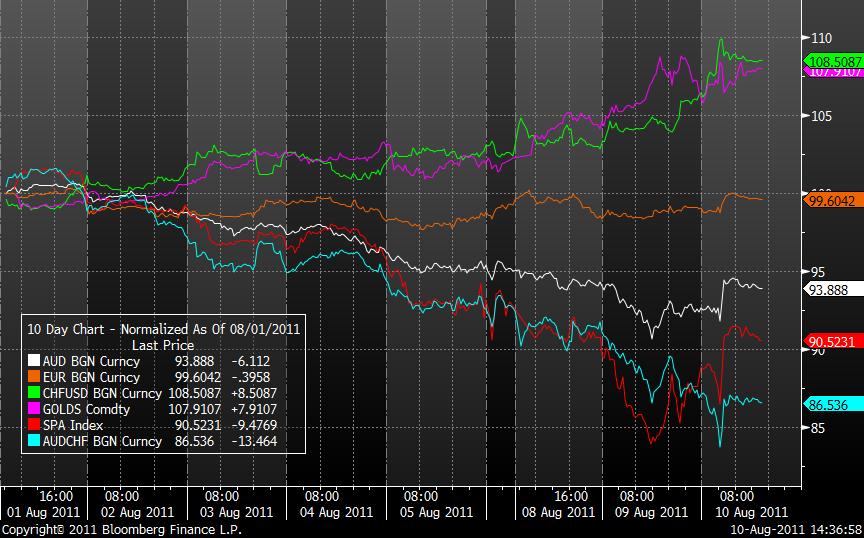

Indeed the low of 0.9928 was synchronus, almost to the minute, with the bounce in S&P futures in night trade as you can see in the chart above. The AUD/USD is the white line, S&P 500 futures the red line and AUD/CHF the light blue line at the bottom.

So it’s all about risk aversion and investor sentiment at the moment – and we know this is an ephemeral force.

Yesterday we had a quick run through the 5 Drivers in our AUD model to assess the outlook – which on balance is bearish. But given the magnitude of both the selloff and bounce this week it is worth posing the question of how sustainable is this current Australian dollar bounce.

Now, obviously on the back of the chart above and recent market price action and correlations you’d probably argue, and be right, that at the moment the AUD’s life and future is not its own.

But is it a bull trap?

The first thing to do is recognise what is driving the AUD at the moment. I can walk you through the 5 Drivers all I want and I can hold that on this model the outlook should remain that the AUD needs to test trendline support at 0.9700 to see just how strong it really is. That remains my view, particulalry given the global growth outlook flagged by the Fed overnight in its announcement that rates are effectively zero forever – at least in market timeframes.

But you have to ask the question of what a long term commitment to zero interest rates is going to do to asset markets around the world.

For mine what the Fed is doing is what it has done since the dim dark days of the initial period of the GFC – it is punting (not too strong a word I think) that if it leaves rates low enough for long enough and markets can contain themselves then they are buying the real economy time to heal.

This is a grand experiment in my view but one that I believe they have little choice in making. The best case scenario given all of the headwinds that face the US and global economy is in many ways a Japanese style period of low rates and low growth but with slightly elevated prices or inflation. Something akin to what they are doing in the UK with 4% inflation and low growth. In that way stability and certainty can return to the economy, inflation can eat away at the “real” value of the debt pile and the economy can heal itself.

The Fed is trying to skirt the mire by buying time for the economy, but as you can see from the FOMC statement last night, it is hardly enthusiasatic about the prospects for jobs and growth in the short term.

But three Fed presidents on the voting panel at the FOMC dissented from the decision and are not even sure that this fresh commitment to low rates is appropriate. This level of dissent is a sharp example of the ongoing debate between the Left and the Right in the US about many things economic and makes it problematic for the Fed to wriggle between the factions to get the outcome, let alone consensus it needs.

So, ultimately, I think the grand experiment will fail to ignite growth.

In the short term the impact of last night’s statement is important because in biasing US and probably global rates lower, in implicitly (I think) undermining the USD it is in many ways seeking to put markets back where we were before the April/May European ructions started and people worried about the end of QE2.

So it’s possible we could be in for a period where traders borrowing at zero can and do chase risk assets. This means that we could get some perverse outcomes where the usual reaction of commodities to weak global growth – falls – is more than offset by money manager capitalists chasing returns on their funds and bidding prices higher.

Equally, the AUD which should go lower in a weak global economic environment may surprise us all because of USD weakness and its place as the world’s favourite punt. This will take away the opportunity for it to act as Australia’s great economic stabiliser.

Do I think the Fed’s action is going to ignite a sustainable move higher where the markets can ignore economic weakness long term in such a way as to take equities and the AUD back toward recent highs?

No, I do not.

After the massive bounce in the AUD and markets, being short here (1.0366) is not for the fainthearted. But I would be looking to get short again while it is below 1.0640. Because in the longer run, as the Fed told us last night, we are going to have a low growth future for many years. This is not an environment that normally suits a strong AUD.

This blog is for information only and does not constitute advice. Neither Greg McKenna nor Lighthouse Securities has taken your personal circumstances, objectives or financial situation into account. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation or needs.