Today’s piece is inspired by the comment flow that was associated with yesterday’s piece on the RP Data – Rismark release. Specifically a little bit of apparent angst about a claim we made that,

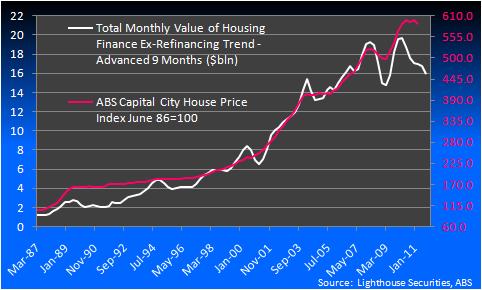

we have modelled the relationship between the quarterly moves in the ABS house price data series and the total monthly value of housing finance ex-refinancing and we see a 0.97 correlation since the mid 1980’s

Now DFM and I have been doing this for a long time and as he said in response to a question the first rule you learn from the Professor in Stats 101 is that others must be able to rely on your work. We hold that near and dear and while no one is infallible we also seek to make statements that underpinned by the data.

Which brings me to the next point I wanted to make. At Lighthouse we say “Information is a commodity. It is the interpretation that counts” and in terms of the reaction to our comment I’d have to say that the level of debate comes from the second part of our strap line. The interpretation of data is what has allowed us, and my fellow bloggers here at MacroBusiness, to be consistently ahead of the MSM Punditariat and the Bank economists on what is really happening in the economy and what is in prospect.

So because something is new to someone does not mean that it is not true. Just they haven’t seen it before or thought about it that way.

While last night’s debate is welcome I’d say the tone was little vitriolic for our liking, on BOTH sides.

But I do wonder how anyone wouldn’t think that there was a strong relationship between the move in house prices and demand for finance. Isn’t that how supply and demand work in a market where leverage is how you finance your position?

Anyway onto the quote and the data/stats that support it.

First thing to note is that we built the house price series by using the weighted average of the 8 capital cities and then building a bridge of the average between the new and old series so we can extend our analysis back into the 1980’s.

The second series is the housing finance numbers (we prefer trend but the raw isn’t much different) and simply use the average of each quarters total housing finance commitment values ex-refinancing.

We used both the correlation function in Excel firstly and the regression available in the analysis toolpack.

Now here is the chart that says it all – at least we think it does (note this is the quarter end not the moving average).

Please note however that this is not to say that myself or DFM necessarily think house prices will crash, even though thats what the stats suggest.

Because unless or until unemployment rises substantially (this could be a reverse causality however – as I think others have pointed out on MacroBusiness previously) and or investors start to liquidate we think the dynamics of the housing market makes prices stickier and more resistant to falls than rises. At least in the short term.

But what this does tell us is that house prices in Australia are under pressure. As are the business models of the Banks who service the demand for credit and ultimately, and unfortunately, the Australian economy is also under pressure.

The RBA is right to be on hold – we think they’ll be there for some time.