As a value investor and climate change agnostic, I have to admit I’ve been watching the carbon tax/ETS debate with a sort of detached interest. Given the Federal government’s unparalleled skill at botching both policy PR and implementation, I had assumed that the ETS would go the way of FuelWatch, Pinkbats and Kevin Rudd’s stiff upper lip. FX movements, commodity prices and legislative risks make the life of a value investor tough enough – calculating carbon pricing and emission intensities just seemed like a hassle I could do without.

As a value investor and climate change agnostic, I have to admit I’ve been watching the carbon tax/ETS debate with a sort of detached interest. Given the Federal government’s unparalleled skill at botching both policy PR and implementation, I had assumed that the ETS would go the way of FuelWatch, Pinkbats and Kevin Rudd’s stiff upper lip. FX movements, commodity prices and legislative risks make the life of a value investor tough enough – calculating carbon pricing and emission intensities just seemed like a hassle I could do without.However after the federal election, Labor rolled over to find themselves in bed with Bob Brown. And to the surprise of many, this minority-government inspired coupling has turned out to be more than a one night stand.

What’s the deal with the Carbon Tax/ETS?

Carbon E. Coyote has done an awesome job of distilling the carbon tax/ETS facts in his series of articles on MB, so I apologise if the following summary doesn’t do them justice (for those who want the good oil, check out his list of blogs here).

Essentially, the ETS is embodied by the government selling permits that give the owners of the permits the right to emit a tonne of carbon. For the first 3-5 years, there will be an unlimited amount of carbon permits sold at a fixed price (price yet to be released). This effectively acts as a tax, hence the outrage about Julia’s “carbon tax” broken promise.

After 3-5 years, the government will move from unlimited release of permits to auctioning a limited number of permits. The permits are sold to the highest bidders, who can then use them to emit carbon or on-sell them to other parties. The price of carbon will vary depending on demand for emissions and how many permits the government auctions each year.

Simple stuff really – they’re just creating a market that turns carbon emissions into a tradeable commodity. The only two big catches (that I can see) are:

- Agriculture is not included (correct me if I am wrong here people). This means stinky-poo cows aren’t penalised for their methane flatulence nor can forestry plantations claim carbon credits to on-sell to emitters;

- Energy intensive export industries (e.g. steel makers) will be given compensation for competing at a disadvantage when exporting to markets without an ETS

What’s that mean on the shop floor?

According to Coyote, Australia emits about 580Mt of CO2 each year. Some 450Mt of these emissions will be covered by the carbon tax/ETS (about 1/6 of our carbon emissions come from livestock and agriculture, which are not covered). The following approximations give you some idea of the emissions intensity of some common products/services:

- 1 tonne of steel – 2.4t CO2e

- 1 tonne of concrete – 0.83t CO2 e

- 1 tonne of aluminium – 1.0t CO2 e

- 1 kWh from Hazelwood power station – 1.6kg CO2 e

- Boeing 737 per hour – 0.09t (90kg) CO2 e

- 1 litre of milk – 0.001t (1kg) CO2 e

- 1 can of coke – 0.00017t (170g) CO2 e

What sectors will be most affected?

Under an Australian ETS, those sectors that use a lot of energy, supply products with elastic demand (i.e. can’t pass on price rises), compete globally (i.e. sell outside of the home market or compete with imports) and operate on thin margins will be the most affected. Fitting this bill will be steel makers, alumina/aluminium processors, concrete users (i.e. builders), airlines and possibly the transport/trucking industry. At this stage, many of of these industries will be compensated for the costs of an ETS, especially those exposed to international competition.

Obviously energy suppliers will be hit hard, but given the rather inelastic demand for electricity they should be able to pass on the most immediate price rises. In the long term, high-emission energy generators will go out of business as the carbon price increases and better technologies are developed – hence the calls for compensation for lost asset value in many coal-fired power stations.

Those businesses that are middle or end users of basic materials will obviously pay higher prices for those materials. This will impact balance sheets as costs go up – whether margins drop will depend on their ability to pass on costs as well energy efficiency efforts. I’d wager Woolies will be fine given its strong return on equity (ROE), pricing power and our basic need to eat.

However, marginal businesses that can’t cope with input-cost increases will be in trouble – especially once the carbon price escalates after the ETS phase starts. Consumer discretionary businesses may also feel the pinch as energy and materials prices increase and consumers see more moolah disappear into their quarter electricity bill. A company like ARB Corporation may find their steel bull bars are both expensive (steel is CO2 intensive) and unwanted (very discretionary item).

There are a few sectors that should float on unscathed by an ETS, feeling only the impact of a slowing economy as the price of energy increases. These include the financials (we still need to do the banking irrespective of a carbon price), agriculture (not part of the scheme), booze/gambling/addictive vices and health care. Exporters of low-energy-intensity goods should also be sweet (think Cochlear) assuming they can survive the rise of our mighty Aussie dollar.

Emissions earnings impacts and compensation

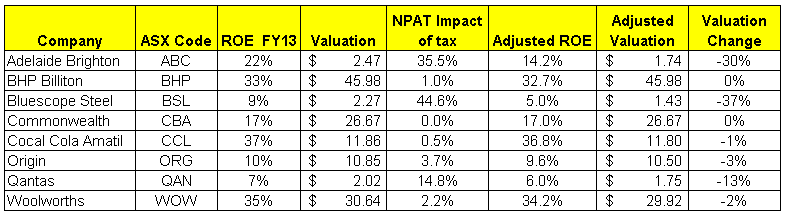

In examining the earnings impacts of a carbon tax – and hence the impact on valuations – I’m going to rely on the good work done by John Abernethy in his article on an Australian carbon tax. Mr Abernethy has estimated the NPAT impact on several ASX companies for FY13 (the starting year of the carbon tax), assuming a carbon tax at $20/tCO2e (but not accounting for any industry compensation). In lieu of a massive research budget and oodles of time, I am going to rely on his calculations and use them to estimate the fundamental valuation impacts on a handful of ASX companies.

The table below shows the companies assumed FY13 ROE (no tax), their pre-carbon tax valuation, their ROE (with tax) and the resulting post-tax valuation. I’ve assumed the NPAT impact starts in Fy13 and is constant there after.

Valuation Impact of Carbon Tax

| Company | ASX Code | ROE FY13 |

Valuation |

NPAT Impact |

Adjusted ROE | Adjusted Valuation | Valuation Change |

| Adelaide Brighton | ABC | 22% | $ 2.47 | 35.5% | 14.2% | $ 1.74 | -30% |

| BHP Billiton | BHP | 33% | $ 45.98 | 1.0% | 32.7% | $ 45.98 | 0% |

| Bluescope Steel* | BSL | 9% | $ 2.27 | 2.2% | 8.6% | $ 2.20* | -3% |

| Commonwealth | CBA | 17% | $ 26.67 | 0.0% | 17.0% | $ 26.67 | 0% |

| Cocal Cola Amatil | CCL | 37% | $ 11.86 | 0.5% | 36.8% | $ 11.80 | -1% |

| Origin | ORG | 10% | $ 10.85 | 3.7% | 9.6% | $ 10.50 | -3% |

| Qantas | QAN | 7% | $ 2.02 | 14.8% | 6.0% | $ 1.75 | -13% |

| Woolworths | WOW | 35% | $ 30.64 | 2.2% | 34.2% | $ 29.92 | -2% |

{kind=link}

* I have shown Bluescope’s valuation assuming that they are compensated for 95% of their emmissions costs. Without this compensation, NPAT impact would have been 44.6% and the valuation would have been around $1.43 (some 37% below our current valuation).

So as you can see, the results are pretty much in line with my earlier summation.

Of course if the doom sayers are correct and the carbon tax/ETS kills the economy, then no share will be safe. However, the relativity of the pain would be the same.

Hot off the Press: Compensation update from Carbon Coyote

There’s been a couple of queries around compensation for certain companies/industries, which is not surprising given the impact a tax would have. The following was emailed to me by the Coyote:

ABC: As a producer of cement they would have got EITE assistance for that activity, and as it is highly emission intensive, it was in the highest bracket of the CPRS compensation scheme, so 90% + Global Recession Buffer = 94.5%. This % is of scope 1 (CO2 produced onsite such as released in the manufacture of lime and the combustion of natural gas in the kiln) and scope 2 (indirect emissions such as use of power) emissions.

QANTAS: (domestic) airtravel not deemed either emission intensive or trade exposed, so no EITE assistance. Qantas will be able to pass on all of its carbon charge to its customers. It already does this; whenever the oil price gets too high, they add a “fuel surcharge” that customers pay. So the interesting thing to watch will be whether they just include the carbon component in the fuel surcharge or whether they introduce a “carbon surcharge” as well as their “fuel surcharge”. The only way they see the carbon price is when the liable entities (ie the oil refineries) pass it through to them as a higher wholesale price of jet fuel; they don’t specifically pay for carbon unless they choose to (for example under the OTN provisions in the CPRS Act). International airtravel coverage is a moving feast globally, but whenever they fill up their A380s in Australia they will be paying an extra 6-7c/l on fuel.

Now that’s based on the old Kevin-Rudd crafted CPRS, which is not necessarily how things will play out in the coming months but it’s a guide. So my ABC valuation will be conservative if they get the full CPRS-level compensation. Should they receive 95% compensation, the value will only drop to about $2.40

So anway, that’s my take on the coming carbon scheme. Given the very dense fog of vagueness surrounding the implementation of the carbon scheme, much of what I assert is debateable – which is just the way I like it. I’m open to your ideas.

Warning: I know this topic can stir passions at the best of time. But for civility’s sake please refrain from debating weather (pun) climate change is happening, whether it’s due to humans, whether we should do anything about it or whether climate scientists are tweed-loving watermelons. That is NOT the point of this piece and I will delete any comment that becomes an off-topic rant.

From an investor’s point of view, it’s a moot point whether humans are messing with the clouds or not – if the guv’ment says you’ll pay for carbon, then we gotta factor it in. When ideology meets reality, reality will kill your portfolio every time.

Disclosure: The author is a Director of a private investment company (Empire Investing Pty Ltd), which has interests in some of the businesses mentioned in this article. The article is not to be taken as investment advice and the views expressed are opinions only. Readers should seek advice from someone who claims to be qualified before considering allocating capital in any investment.