Last year the EUR got down under 1.20 and I was convinced it was going to its true value, in my opinion anyway of 1:1 with the USD. Nothing against Germany or even France for that matter but the bolted on Eurozone area to these and other “core” nations really does make the sum of the whole worth a lot less than what a Deustchemark or French Franc would fetch in the open market.

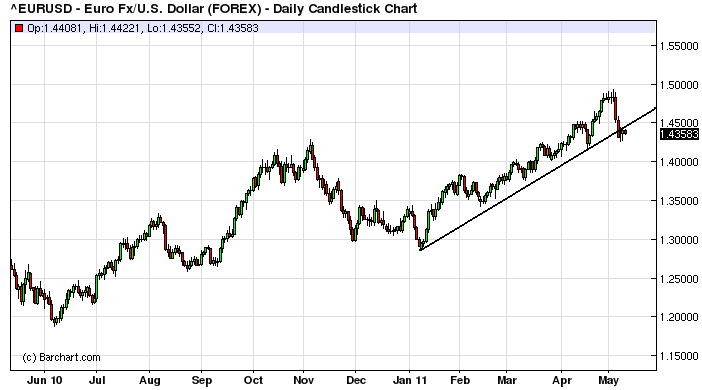

Alas I got too bearish and Chairman Bernanke rode in in his helicopter and started raining US Dollars on the planet and that was the end of that. The USD weakened and EUR rallied all the way back to 1.4938 last week as the chart below shows.

Now it is a true measure of the impact of QE on valuations of the USD that against such a parlous Sovereign European Deficit and Debt position that the EUR was able to rally for such a sustained period and to such an extreme valuation.

Clearly this strength relies in large part on the strength of German resolve to both hold the Eurozone together and maintain the political will to keep stumping up the cash to bail out the Countries of the periphery, the PIIGS (Portugal, Ireland, Italy, Greece and Spain). In the old days we used to call them Club Med and I still think this sums them up better than PIIGS, although with perhaps the exception of Italy, they are certainly on the nose.

So far Germany has been able to hold the Euro together pretty well and has forestalled a Greek or Irish default. But writing in the Financial Times last night (that’s their cartoon up top) Martin Wolf suggests that a day of reckoning is approaching for the Debt laden periphery.

A story is told of a man sentenced by his king to death. The latter tells him that he can keep his life if he teaches the monarch’s horse to talk within a year. The condemned man agrees. Asked why he did so, he answers that anything might happen: the king might die; he might die; and the horse might learn to talk.

This has been the eurozone’s approach to the fiscal crises that have engulfed Greece, Ireland and Portugal, and threaten other member states. Policymakers have decided to play for time in the hope that the countries in difficulty will restore their creditworthiness. So far, this effort has failed: the cost of borrowing has risen, not fallen (see chart). In the case of Greece, the first of the countries to receive help, the chances of renewed access to private lending on terms that the country can afford are negligible. But postponing the day of reckoning will not make the Greek predicament better: on the contrary, it will merely make the debt restructuring more painful when it comes.

Given such a debt burden, what are the chances that a country with Greece’s history would be able to finance its debt in the market on terms consistent with a decline in the debt burden? Extremely small.

This is the key point in all this, as Reinhart and Rogoff have taught us, is that once the debt burden gets too big and the interest rate too high countries get caught in a spiral from which they struggle to drag themselves out of without a default. Look at Greece for example, EUR 110 bln last year and up to another EUR 50 bln in bailouts being propsed now.

Martin Wolf says,

What might persuade investors that this is sufficiently likely to justify funding Greece? Nothing I can imagine. But remember that 6 per cent would be a spread of less than 3 percentage points over German bunds. The default risk does not need to be very high to make this extremely unappealing.

In short, Greece is in a Catch 22: creditors know it lacks the credibility to borrow at rates of interest it can afford. It will remain dependent on ever greater quantities of official financing. However that creates an even deeper trap.

It seems that it is inevitable that Greek debt will be “restructured” thats part of why Standard and Poors down graded the Greek Sovereign rating to B last week and it should not be a shock to investors. But it won’t end there. Martin Wolf again

The saga is most unlikely to end with Greece. Other peripheral countries – Ireland and Portugal, for example – are also likely to find themselves locked out of private markets for a long time. In neither case is a return to fiscal health in any way guaranteed, given the extremely difficult starting points.

Overindebted countries with their own currencies inflate. But countries that borrow in foreign currencies default. By joining the eurozone, members have moved from the former state to the latter. If restructuring is ruled out, members must both finance and police one another. More precisely, the bigger and the stronger will finance and police the smaller and the weaker. Worse, they will have to go on doing so until all these horses can talk. Is that the future they want?

So far the EUR has managed to hold within 6 big figures of the recent high and sits at 1.4340 as I write. this is in no small measure because Europes present appears to be the United States future. But the EUR is not the DEM (Deutschemark) and their may be signs that the USD is turning (at least unless or until we see QE3) so we may be seeing a changing the currency game which has important global ramifications.

The troubles of the Club Med countries aren’t going away but if they are assisting in changing the outlook for the USD then they can actually be a positive. The world is simply too fragile for a USD crash and the forces it would let loose in commodity and currency markets not to mention the inflationary impulse.

If the USD is turning then commodities (denominated in USD’s) should fall in the coming 6 months relieving inflationary pressures and letting central bankers off the hook. This should help temper the ECB’s inflation fighting vigor, reduce similar pressures in the developing world, especially China, and generally give any recovery a chance to gain more traction.

For the Australian dollar, the top is in medium term if the $US is turning, as I think it is. On the crosses – AUD/EUR, AUD/GBP, AUD/JPY – I expect that the positives that have accrued to the Aussie in the past six months will see it appreciate, especially against the euro.