The Aussie’s price action once again speaks of underlying demand and overall strength even if it wasn’t able to eclipse or close above last week’s highs.

Opening the week near the highs, the AUD traded down to a low a little below 1.04 on the back of what was widely reported to be a bit of “risk off” but as I wrote here at the time it seemed to me more akin to punters taking a few dollars of the table after Goldman Sachs advised clients to lock in profits which either means buy a put option or in most cases “sell” out of your position.

‘Risk on’ and ‘Risk off’ are becoming overused phrases to explain market action in the very short term. To me it seems like lazy reporting and or strategising. Traders trade and that means buying AND selling. Indeed the beautiful thing about currencies and futures based commodity markets is that it is easy to both buy and sell for pretty much everyone in a way that it is not for direct equities or bonds. It’s one of the reasons I like these markets so much, you can be long, square or short quite easily. And to reiterate traders trade so some days there are just more sellers than buyers. It’s got little to do with ‘risk on or off’ and more to do with technicals in the short term trading goals.

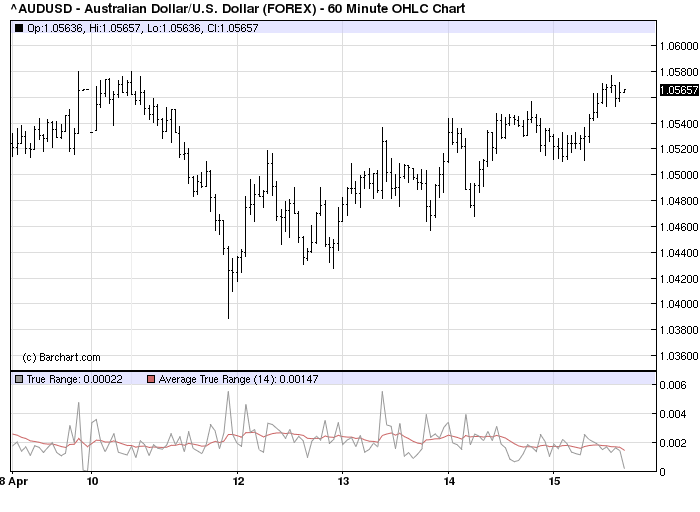

Below is a chart of the AUD’s moves during the week. What we see is a pretty good hourly uptrend (could be a pennant for the technically minded) from the low. Last week we said we’d expect a technical pullback which is what we got but I confess I was looking for a move back to 1.0249 which is a Fibonacci retracement level of the big move higher recently so I would have missed this bounce back if I had had only one shot at it. Although my stops would have made a little money as they flipped me out of my short on the way back up.

The price action was pretty solid insofar as the buyers came back quick, very quickly. However, fundamentally the Chinese and Indian inflation situation (not to mention German, European and UK inflation outlooks) do potentially pose a “real” risk to investors and traders perceptions of where the global economy is going to go over the next year or so as central bankers grapple with tighter rates and the real strength of the economy. For better, or most likely worse, inflation fighting is likely to be the main focus in my opinion.

Chinese inflation in particular continues to accelerate with yesterday’s data showing an increase to 5.4% from the 4.9% the market expected. It seems to me that the Chinese government, if they are serious about restraining the price pressures in their economy, will need to tighten further both reserve requirements and official rates. They need to get a sharply positive real rate.

The consequence of this is going to raise the stakes on a misstep as the further they are forced to go the greater the chance that they find the tipping point which is the difference between a soft landing and an economy that pulls back hard. A crash in the Chinese economy isn’t forecast yet but the chances, or probability, must be rising the further interests need to go to restrain prices.

Back home if we look at our 5 drivers we see a continued underpinning of the AUD against the USD and it held its own against the big crosses this week although AUD/NZD did fall. This is more about the Kiwi than the AUD at the moment.

In terms of the outlook, the longer term backdrop in all of the key drivers remains supportive but for the short term the AUD needs to trade and hold above last weeks highs to get the upside momentum going again and head toward 1.07. There are two types of consolidation/pullbacks, time and price. An inability to get through last week’s highs in the next week doesn’t derail the AUD completely but when I look at correlated markets like equities I think their momentum is waning which may ultimately see a “real” risk off event. Global markets are due for one.

Disclosure: This post is not advice or a recommendation to buy or sell. Do your own research and consult an adviser before allocating capital.