After a quick holiday across the pond in NZ (luckily not near Christchurch), your blogger returned to Australia to the news that West Australia Newspaper Holdings (WAN) is going to buy the Seven Media Group from Seven Group Holdings (SVM). So a WA media monopoly is marrying the TV sideshow of a Caterpillar servicing business. I can’t wait to see their kids.

After a quick holiday across the pond in NZ (luckily not near Christchurch), your blogger returned to Australia to the news that West Australia Newspaper Holdings (WAN) is going to buy the Seven Media Group from Seven Group Holdings (SVM). So a WA media monopoly is marrying the TV sideshow of a Caterpillar servicing business. I can’t wait to see their kids.Rather than ploughing into the financial media for summaries and the usual warring opinion pieces, I thought I’d look at the merger based purely on the numbers. No bias from the usual financial commentators – just the shiny prospectus and the raw numbers giving me the answers to:

- Is Seven Group worth buying?

- If so, how much should WAN pay for it?

Would I want to own Seven Group?

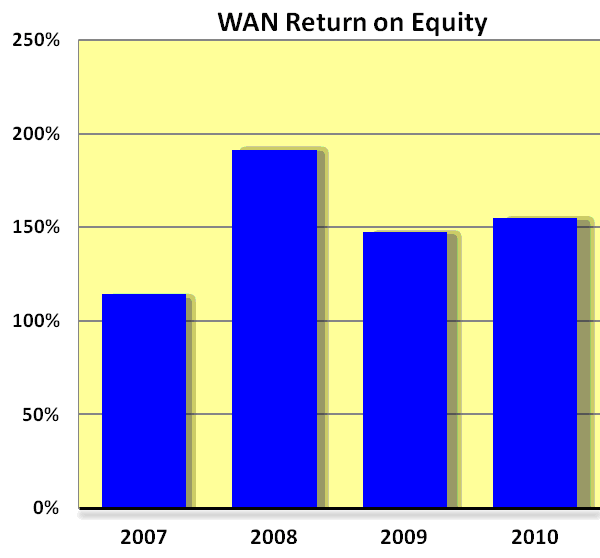

My standard test of any business is to look at how good it is at generating income from its capital. In other words, what is its return on equity (ROE)? The Seven Group forms part of SVM, which consists of the Seven Group and Westrac (a heavy machinery servicing group). Aside from the free-to-air channels 7, 7two and 7mate, the Seven Group also owns Yahoo!7 and Pacific magazines, which accounts for 29% of all Australian magazine sales.

It’s difficult to differentiate the after-tax profit of the Seven Group from the whole of SVM, but the buyout prospectus does provide a forecast EBIT for FY11 of $388M.

Now, WAN is planning to purchase Seven for just over $4 billion in enterprise value. This represents a measly 9.5% EBIT return on that enterprise value. However, WAN is financing some of this purchase debt, so the actual increase in their equity levels will be $2.4B. This equates to an EBIT return of about 16% on the increase in equity. This is an improvement, but remember we haven’t deducted interest (did I mention debt?) and tax.

So, it looks like the Seven Group isn’t very good at turning shareholder capital into decent returns. I know I certainly wouldn’t buy it, even at big discounts to its intrinsic value. Which pretty much answers the first question – WAN shouldn’t buy Seven. It’s a donkey.

Unless of course the Seven Group is a better burro than WAN – which leads us to…

Would I want to own WAN?

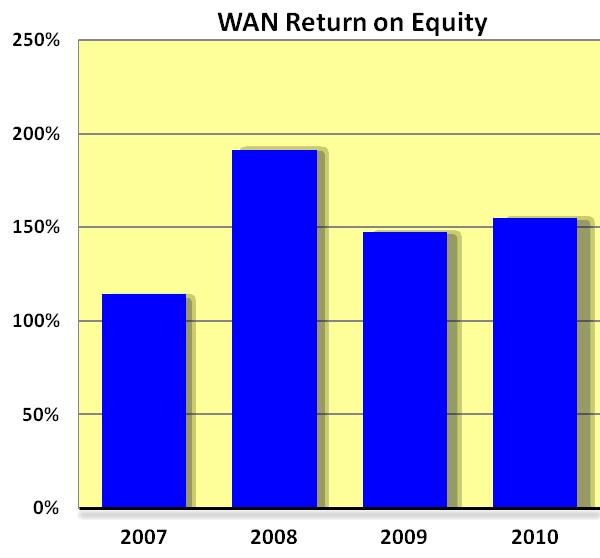

A glance at WAN’s pre-buyout ROE makes for some impressive reading – it averages well over 100% for the last 5 years.

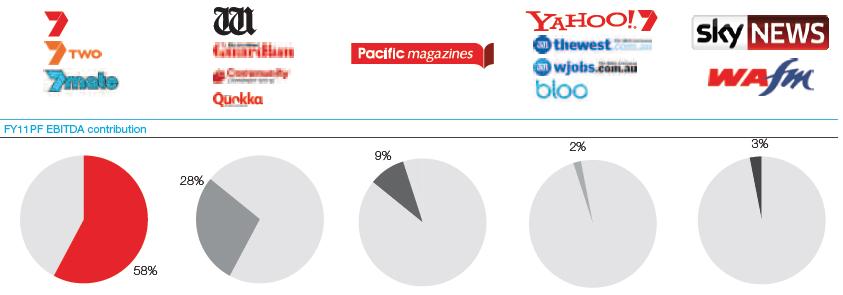

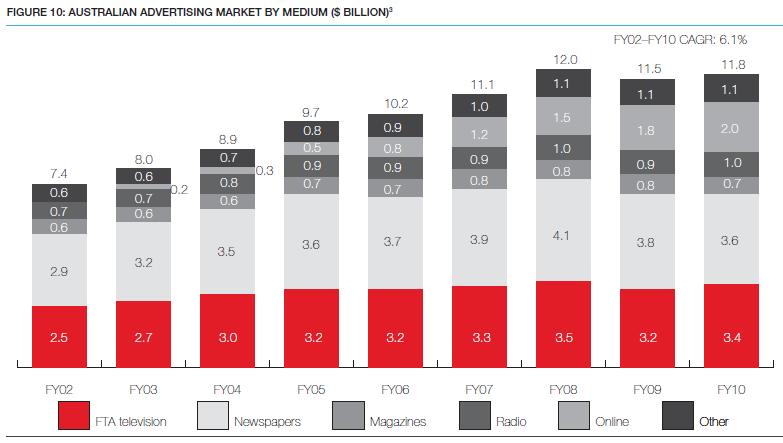

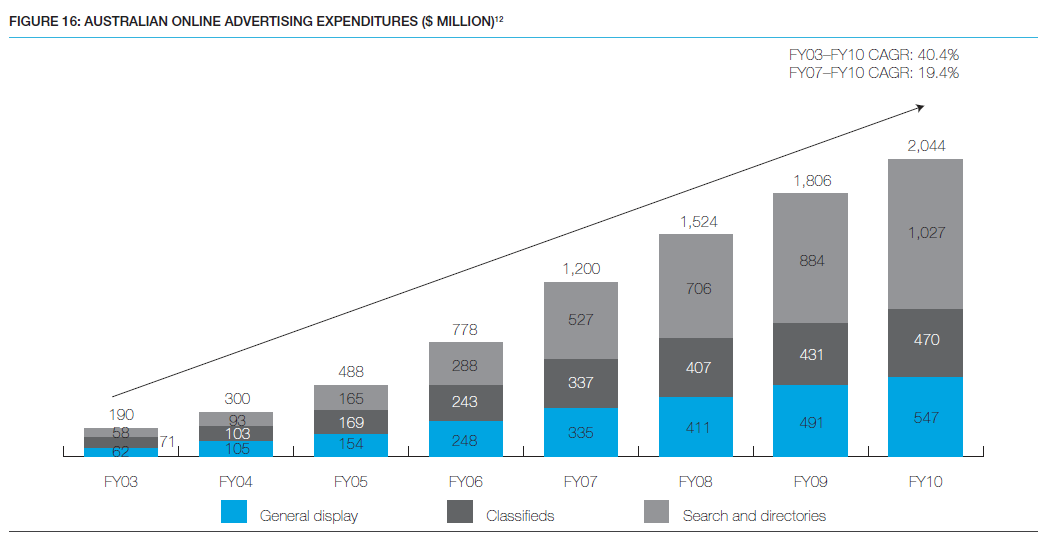

Their debt levels are very modest (about twice after-tax earnings and 10% net debt to equity) and their intangible assets are very low. This may explain the very high ROE – no inflation of equity with goodwill and branding value. WANs market dominance in the Western Australian print and radio media landscape is also a plus. The big flaw is the same flaw held by all traditional media companies – eroding advertising revenues due to the internet. None the less, WAN was a company‘d like to own given it traded at the right price. It’s a thoroughbred. So, I believe WAN investors will be worse off for this buyout. They have a very high ROE company with a dominant market position. Once the buyout is completed, they will have bought a larger, poorer-performing media company that has assets in very competitive market spaces. Taking the analogy to extremes, the new company will be an Ass. The deal would only make sense if WAN was paying a lower price for Seven. Which leads us to… What should WAN pay for Seven Group? The easy answer is to take the expected after-tax earnings of the Seven Group and divide them by a required rate of return (RR). Assuming an optimistic after tax profit of $300M for FY11 and an RR of 15%, the purchase price should be about $2.7B total. That’s a bit different from the $4.0B they are intending to pay, including debt. So it looks like WAN is paying way too much for its donkey sire. Are we missing something? So the numbers tell us it’s a bad deal, but are we missing something that the boring old figures don’t tell us? The synergies are estimated at $15M in the prospectus, which is nothing in the scheme of a $4b sale. Diversifying WANs revenue base is a good idea, but not at the cost of overpaying for Seven. The only non-tangible benefit I could think was acquiring an asset that provides good revenue growth for WAN, which would justify the high purchase price. So is there something inside Seven worth getting a hold of? The forecast EBIT (by segment) of the combined WAN/Seven Group is shown in the graph below, taken from pg 11 of the WAN buyout prospectus. So, the vast majority of the EDITDA for the newly merged company will come from Free To Air television and WAN’s assets. Both of these segments fall under the “traditional” media tag mentioned earlier. They havehigh production costs (cameras, actors, printing presses), are very competitive (channels 7, 9, SBS and ABC) and are being assailed by the cheap and ubiquitous internet. Only 2% of EBITDA comes from online sources. To take a macro view, the table below (WAN buyout prospectus, pg 60) shows the size of each segment of the entire Australian advertising market. FTA television has grown at an average annual rate of 4% – barely above inflation. It’s plain to see that the online section is the standout, growing from 5% to 17% of expenditure in the last 5 years. The rate of growth of the online market is highlighted further the following graph (WAN prospectus, pg 65). However, the new company will only have a 2% EBITDA exposure online. So obviously it isn’t looking to tap into the rapidly growing online market. With the purchase of Seven, they’ll have a very big exposure in TV and an increased exposure to print, but a miniscule exposure to the medium of the future – the internet. Summary So, in summary the buyout is a bad deal. It takes a high-ROE print monopoly and adds a poor-performing media asset that has little exposure to the growth segment of the market. I guess you can chalk this up to another boomer-controlled media company struggling with the challenges of the internet. Or maybe it’s just a run of the mill, over-priced M&A. Over at Empire Investing, we’ve taken a look at the composition of WAN post-buyout and calculated the new intrinsic value. With the increase in equity and forecast earnings for FY11, we wouldn’t buy it for anything more than $4.20. If someone can shed some light on the drivers behind the deal, please do. I just can’t see what the point is. In any event, I bet Kerry Stokes is stoked.

{kind=link}